Updated: June 27, 2025

Baby Boomer Retirement Strategies: Income Planning for the Boomer Boom

The baby boom has become the retirement boom. As thousands of people reach retirement age every day, the average age of the U.S. population is changing, which is having a profound impact on the retirement experience. To navigate the coming years, effective baby boomer retirement strategies are critical.

How Many Baby Boomers Are There?

It’s called the baby boom generation for good reason: this generation represented a surge in the population. According to the Population Reference Bureau, 76 million baby boomers were born in the U.S. in the 19-year period between 1946 and 1964. These baby boomers are now reaching retirement age. The U.S. Census Bureau says all baby boomers will be aged 65 or above by 2030. Every day, approximately 10,000 baby boomers turn 65.

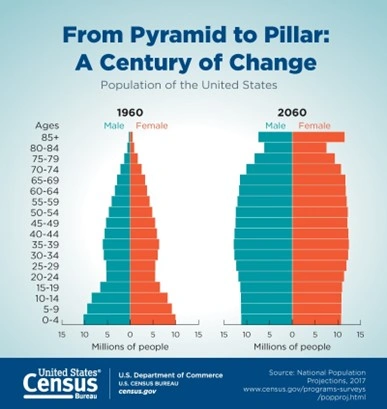

The Graying of Society The entire U.S. population is aging. The U.S. Census Bureau says older adults are projected to outnumber children in 2034 for the first time in U.S. history. By 2060, approximately one out of every four Americans will be aged 65 or above.

Source: https://www.census.gov/library/stories/2018/03/graying-america.html

The Impact of the Retirement Boom

As baby boomers age, they’ll need more health and retirement services. This will put strain on many industries, including healthcare and senior living. At the same time, many industries are experiencing skilled labor shortages as their most experienced workers retire in droves. Investopedia warns that these trends could have economic consequences. For example, increased demand for healthcare services could cause the cost of healthcare services to increase. Furthermore, skilled worker shortages could fuel higher wages, which could trigger higher inflation rates.

The aging population will also put pressure on government programs designed to help the elderly, notably Medicare and Social Security retirement benefits. The Social Security Administration says it will face challenges in the near future due to demographic changes. As the worker-to-beneficiary ratio falls, the Social Security trust fund is at risk of depletion.

To address this issue, some people have proposed raising the minimum retirement age, while others have proposed reducing retirement benefits.

At the moment, it’s unclear what will happen in the future, but many who currently rely on Social Security or Medicare or who plan to rely on these programs in the future are concerned. A 2024 Gallup poll found that 73% of adults are worried about Medicare and 80% are worried about Social Security.

Finding Retirement Income Solutions for the Graying Population

Amid the threats to Social Security and Medicare, the risk of high inflation, and the surging demand for healthcare and senior services, baby boomers need retirement income solutions they can count on.

Few employers offer defined benefit pension plans anymore, and the 401(k) plans that have largely replaced them are subject to market volatility. As a result, many retirees have been looking for new retirement income sources – and annuities have emerged as a popular solution. In an American Council of Life Insurers survey of 1,003 retirement savers, 26% already owned annuities and, of those, 86% were interested in buying more.

Annuities for Retirees

To understand why retirees are increasingly drawn to annuities, it’s important to understand what annuities are and how they work.

An annuity is a contract between the insurance company that sells the annuity and the individual who buys it. Retirees frequently choose this option because annuities can:

- Create a steady income stream. The individual pays an upfront premium to purchase the annuity. In return, the insurance company provides a stream of payments that may start immediately or at a predetermined future date.

- Grow in value. Exactly how this works depends on the type of annuity in question. Variable annuities grow at a variable crediting rate tied to the underlying investments, meaning market volatility impacts growth. Fixed annuities offer a predetermined minimum crediting rate to protect the annuity from market volatility.

- Provide tax advantages. When you’re saving for retirement, an unexpected tax bill may derail your plans. Annuities enjoy tax-deferred growth, meaning you don’t have to pay taxes on growth until you make a withdrawal. In addition to simply not having to worry about taxes for a while, this is beneficial because you might be in a lower tax bracket once you retire and because it lets you maximize compounded interest growth.

Should You Embrace an Annuity Retirement Strategy?

The retirement boom is fueling increased demand for practical and innovative retirement income solutions. Annuities are emerging as a preferred choice for many retirees. However, there are both pros and cons of annuities to consider – they may not be the right fit for everyone. Ask yourself:

- Are you looking for a retirement income stream? As an annuity can help you achieve this goal, it may be worth pursuing one.

- Do you know what type of annuity you want? Whether you buy a variable annuity or a fixed annuity will make a big difference to your return. Although variable annuities produce high return rates if the market performs well, they are also riskier and tend to have pricier fees. A fixed annuity is a better option for retirees with a lower risk tolerance. Also consider whether you want a deferred annuity (which begins paying out at a future date) or an immediate annuity (which begins paying out immediately).

- Do you understand the early surrender and distribution penalties? If you change your mind and surrender your annuity early, you may face a surrender fee. The IRS also levies tax penalties for early distributions if you are younger than 59 ½. To avoid fees and penalties, it’s important to have realistic plans regarding when you will need your funds. It’s also smart to have some emergency savings or liquid funds available.

- Will you receive a good return? For the best return possible, it’s important to understand the details of your contract. An annuity with a higher-than-average interest rate may seem ideal, but it might not be as good a deal as you think if it comes with excessive fees or uses a simple interest rate instead of a compound interest rate. Before you buy an annuity, make sure you understand exactly how much you can expect to receive back.

Are you interested in annuities for retirees? Canvas offers straightforward fixed annuities. Our licensed, non-commissioned agents can help you navigate your retirement income options.

Resource Hub