Updated: January 6, 2026

What is a Life Annuity with Period Certain? How Does It Work?

When you are ready to retire, a life annuity with period certain is one of several payout options insurers offer. You select a specific guaranteed period (the “certain” period) during which payments are guaranteed. If you die during that period, payments continue to your beneficiary for the remainder of the term; if you outlive the term, payments continue for as long as you live.

Annuities can help you save before retirement and convert savings into predictable income once you retire. What makes annuities unique among retirement products is their ability to provide income you cannot outlive.

In this article, you’ll learn a little more about the life annuity with period certain option, including the features that make it different from other payout choices. Then you’ll be able to determine if a life annuity with period certain is right for you.

How They Work

A life‑with‑period‑certain payout has two parts: the life income guarantee and the certain period.

Life Payout Option

A life annuity refers to a payout option that guarantees annuity payments for life or until the death of the annuitant.

A straight life payout guarantees income for life, stopping at death. If funds remain when the annuitant dies, they do not pass to a beneficiary under a straight‑life option.

For example, imagine you buy an annuity at age 55 and choose a straight life payout option. Then you annuitize and turn it into periodic payments. If you live to be 95, you will receive income payments for 40 years. But if you only live to 58, you’ll only receive income payments for three years.

So straight life payouts can be a bit of a gamble. The advantage is that you have guaranteed income for the rest of your life. If you live a long time, you can be paid a significant amount of money. You may even get paid back more than you put in your annuity. But the disadvantage is that if you live for only a short time, you may not earn back all the money you put in the annuity.

Period Certain Payout Option

A period‑certain payout guarantees payments for a set term (e.g., 5, 10, 15 or 20 years). If the annuitant dies during that term, remaining payments go to the named beneficiary; if the annuitant outlives the term, payments cease.

Many shoppers specifically compare a ten-year certain and life annuity against other payout options—10 years is a common length that balances protection for heirs with lifetime income.

Life Income with Period Certain Blends Both

Life income with period certain combines both guarantees. You receive a monthly payment for the term you choose; if you die before the term ends, your beneficiary receives the remaining payments. If you outlive the term, payments continue for life.

Joint Life vs. Single Life with Period Certain

A single life annuity provides lifetime income based on one life and typically pays more than a comparable joint life option.

A joint and survivor option covers two lives (often spouses), continuing income as long as either person is living. Joint options generally pay less per month than single‑life options because income is expected to last longer.

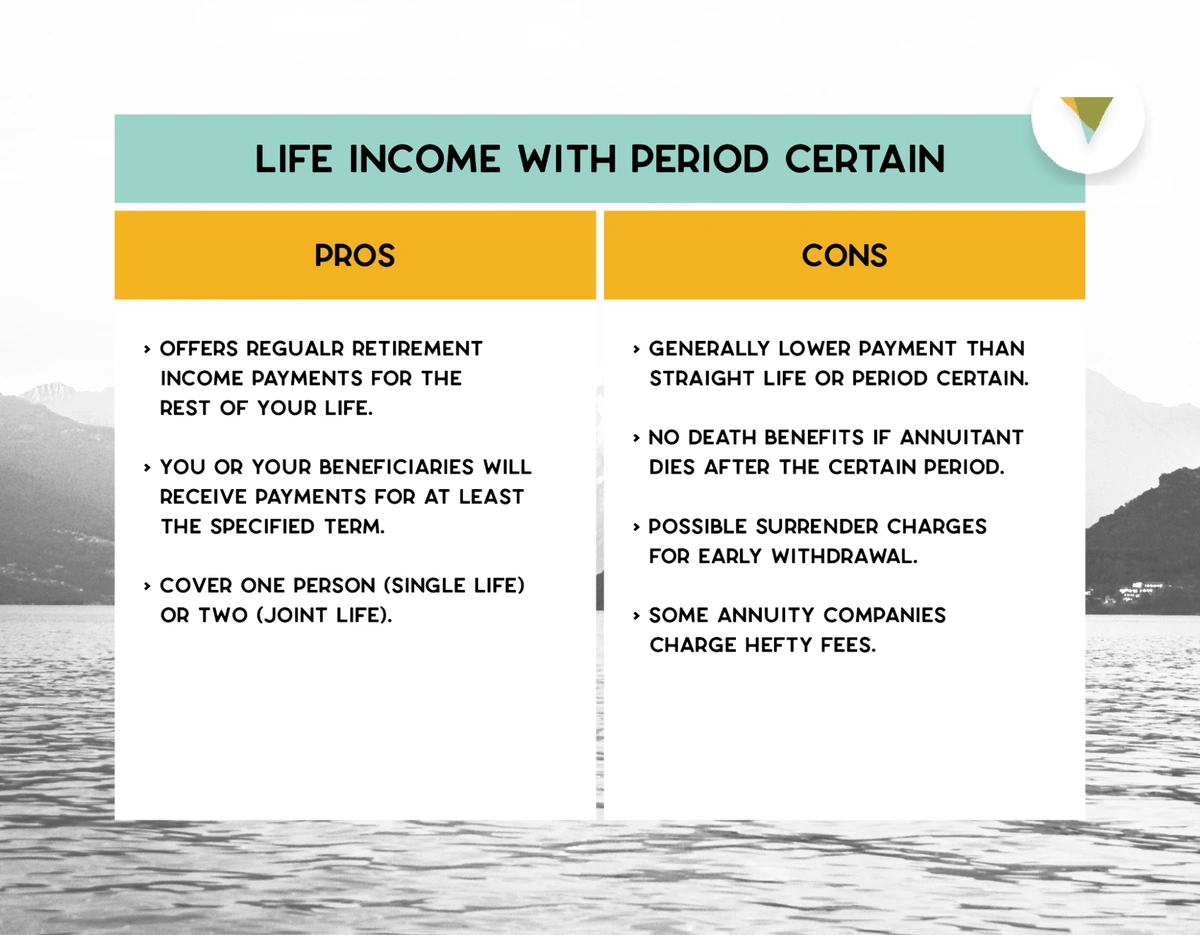

Pros and Cons of an Annuity with Life Income and Period Certain Payouts

The life income with period certain payout choice can be a great option for ensuring lifetime income while also guarding against the risk of losing your money if you die too early. But, like any product, it has advantages and disadvantages that may or may not make it appropriate for you. Here are the pros and cons.

Pros

Some of the advantages include:

- Potential lifetime income.

- Heirs receive payments for at least the certain term.

- Available on single or joint life.

Cons

There can be some downsides, including:

- Payments are usually lower than straight life.

- No death benefit if death occurs after the certain term.

- Illiquidity and possible surrender charges during the early years.

- Some contracts have additional fees.

What Types of Annuities Offer This Option?

Most immediate annuities and deferred annuities that are annuitized can be set to life with period certain. If you are still accumulating, consider a deferred annuity (fixed, fixed‑indexed, or variable) and choose your payout option later. If you are ready to turn savings into income now, an immediate annuity lets you pick the same life‑with‑period‑certain structure at purchase.

10‑Year MYGA Comparisons Shoppers Often Research

Consumers sometimes compare life‑with‑period‑certain payouts to 10‑year multi‑year guaranteed annuities (MYGAs) they see in the market—for example, asking about the benefits of products like an “American National Palladium MYG 10-year annuity.” A MYGA is an accumulation product with a guaranteed rate for a set term, while a life‑with‑10‑years‑certain payout is an income structure. They solve different needs: MYGAs grow principal at a fixed rate; income annuities convert assets to lifetime payments with an optional guaranteed period.

Who Is It Right For?

Life income with period certain can fit retirees who want lifetime income but also want to ensure a minimum stream goes to a beneficiary if death occurs early. Those confident they will live well beyond the certain term may prefer straight life for higher income; those prioritizing higher payments for a defined window may consider period‑certain‑only payouts.

Canvas offers simple and safe fixed annuity products to help you plan for retirement. Zero commissions, account charges, or fees make Canvas stand out from our competitors. And our annuities can be structured to pay out as a life annuity with period certain.

To learn more about these annuities, contact one of our knowledgeable licensed representatives today.

Resource Hub