Table of Contents

- What Is the Present Value of an Annuity?

- Why Calculate Present Value?

- Calculating Present Value for Ordinary Annuities vs. Annuities Due

- Formula to Find the Present Value of an Ordinary Annuity

- Formula to Find the Present Value of an Annuity Due

- Find Out What Your Future Annuity Payments Are Worth Now

Updated: February 27, 2026

How to Find the Present Value of an Annuity

The present value of an annuity is a calculation that shows you the cash value of future payments from an annuity given in today's dollars. To calculate the present value of an annuity, you will need the value of each payment, the interest rate (or "discount rate"), and the number of payments that will occur.

If you already know what a present value calculation is used for and just need the formula, you can find it here:

Present Value = PMT x ((1 - (1 + r) ^ -n ) / r)

- Where PMT is the value of each payment,

- r is the interest rate,

- and n is the number of payments.

If you're looking for an interactive present value of annuity calculator that you can use in your web browser, here's a good resource.

Retirement planning can be complicated.

It's tricky because there are so many uncertainties: What will my health be like? What government support will be available? How much money will I really need?

Adding to the uncertainty is the changing value of money. A dollar today is worth more than that same dollar in the future.

To make sound financial decisions, you have to be able to estimate the value of future money in today's dollars. This is true when it comes to annuities, too.

With an annuity, you put money in now and receive guaranteed income in retirement.

To make a well-informed decision about your annuity, it’s helpful to know the value of those future payments today. That's where the present value of an annuity comes in.

The present value of an annuity is the value of future annuity payments right now. In this article, we give you everything you need to calculate the current value of future annuity payments.

What Is the Present Value of an Annuity?

The present value of an annuity is the value of a series of future payments in today’s dollars.

Calculating the value of a series of future payments is complex because money is worth more today than the same amount of money will be worth in the future. We call this the “time value of money”—the future value of a given amount is less than its current value.

One reason for this is inflation—the price of goods tends to rise. During periods of inflation, a currency’s purchasing power decreases.

That means a dollar today buys more than it will in the future.

Another reason money is more valuable now is that it can grow with compounding interest.

Imagine you took $300,000 today and put it in a deferred annuity for 5 years at a 3% rate of return. The value of the annuity would grow over the 5 years. At the end of the term, you would have over $347,000.

Because you can turn $300,000 today into $347,000 in 5 years, it’s worth more than getting $300,000 in 5 years—in this case, $47,000 more!

The takeaway is this: we can’t directly compare the value of money we have today with money we get in the future.

To properly compare them, we have to factor in the lower value that future money has.

So, how do we do that? How much are future payments worth in today’s currency? We can find out by calculating their present value.

Why Calculate Present Value?

There are lots of reasons you might want to know about the value of future annuity payments.

Here's a common situation: Imagine that you bought one of Canvas Annuity's deferred annuity products in the past. You chose the Future Fund with a 7-year term. Now, the 7-year term is up, let’s assume that your account value is worth about $300,000. You have the option to take that out as a single lump sum, or you can annuitize it and turn it into a series of periodic payments.

What would you do? To decide, it’s best to know what the present value of those future payments will be. Once you calculate the present value of the series of payments, you can compare it to the value of the lump sum payment.

Knowing the present value of your annuity payments will help you make a more informed decision.

Calculating Present Value for Ordinary Annuities vs. Annuities Due

Remember that an “annuity” in a general sense can refer to any series of periodic payments.

(At Canvas Annuity, we sell retirement annuities. These are special kinds of insurance products designed to provide a guaranteed retirement income. Insurance companies tend to use "annuity" to mean the insurance product that provides income in retirement. But technically, it can refer to any series of regular, periodic payments.)

An income annuity for retirement could be either an ordinary annuity or an annuity due. It just depends on whether it pays you at the end of a given period of time or at the beginning.

An ordinary annuity is a series of equal payments paid at the end of each period.

An example could be monthly mortgage payments where the first payment and future payments occur at the end of the month.

An annuity due is a series of equal payments where payment occurs at the beginning of each period.

An example could be a property rental agreement where renters make monthly payments at the beginning of the month. You don’t need an annuity calculator or an excel sheet to calculate the present value of an annuity.

All you need is the right formula. The present value of the annuity formula varies depending on what kind of annuity you’d like to calculate.

We present both here.

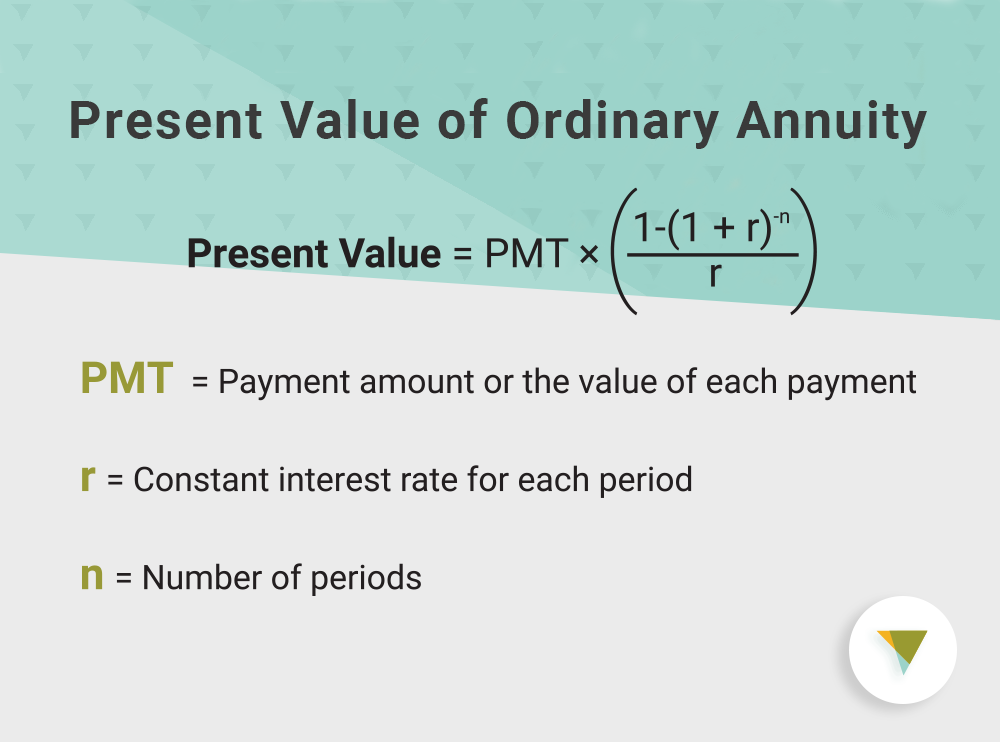

Formula to Find the Present Value of an Ordinary Annuity

The formula for finding the present value of an ordinary annuity is:

Present Value = PMT x ((1 - (1 + r) ^ -n ) / r)

Where,

- PMT is the payment amount or the value of each payment

- r is the constant interest rate for each period (also known as the “discount rate”)

- n is the number of periods (the number of payments that will occur)

For example, imagine an annuity that pays out $30,000 at the end of each year for 10 years, and the annual interest rate is 3%.

Present Value = $30,000 x ((1 - (1 + 0.03) ^ -10) / 0.03) = $255,906.09

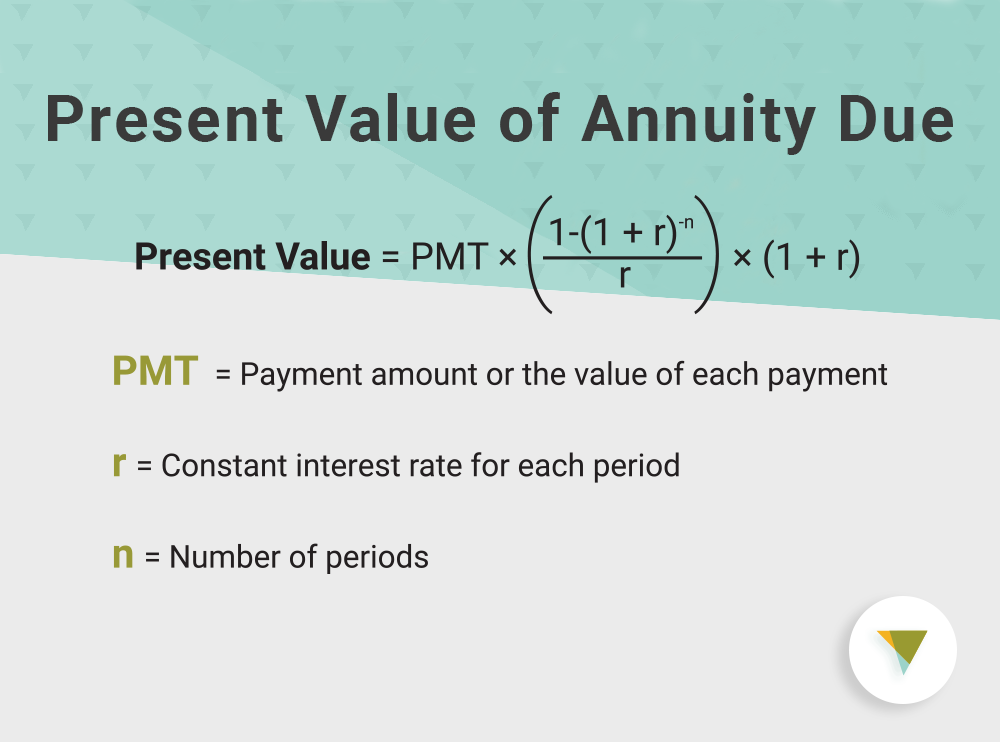

Formula to Find the Present Value of an Annuity Due

Here is the present value of an annuity formula for annuities due:

Present Value = PMT x ((1 - (1 + r) ^ -n ) / r) x (1 + r)

Where,

- PMT is the value of the cash flows

- r is the constant interest rate for each period (also known as the “discount rate”)

- n is the number of payment periods

For example, imagine an annuity pays out $30,000 at the beginning of each year for 10 years, and the interest rate is 3%.

Present Value = $30,000 x ((1 - (1 + 0.03) ^ -10) / 0.03) x (1 + 0.03) = $263,583.27

Find Out What Your Future Annuity Payments Are Worth Now

Annuities give you lots of options—and that's a good thing! But with more options come more decisions.

The present value calculation is a tool that can help you make decisions about your annuity.

For example, this annuity formula can help you decide whether you should annuitize or whether you should withdraw your annuity as a lump sum of money.

Remember that the present value of the annuity isn't the only consideration that matters in your decision.

You may want to consider the tax implications of taking your annuity out in a lump sum versus periodic payments.

Also, consider the intangible benefits that can come with regular annuity income payments.

Receiving periodic payments over a number of years may help you feel more financially secure and certain about the future.

And, there’s another option when you come to the end of your annuity term: You can always purchase a new annuity.

Having a growing annuity ensures your money continues to earn. If you're feeling uncertain, consult with a financial advisor. They can help you make the best decisions for your particular situation. And if you want to know more about how annuities can help secure your financial future, get in touch with our licensed representatives.

They can show you how a deferred annuity from Canvas Annuity can grow your money, ensuring you have a guaranteed income when you need it most.

Resource Hub