Updated: August 14, 2025

What Is a 401(k)?

Planning for Retirement with a 401(k)

There are a variety of plans people use to save for retirement. From annuities to IRAs to 401(k) plans each have their own advantages and disadvantages when strategizing retirement savings.

In this article, we’re taking a closer look at one of the most widely used retirement plans in the U.S.—the 401(k). Learn more about what a 401(k) is, how it works, and how to take advantage of its benefits for healthy retirement savings down the road.

What is a 401(k)?

A 401(k) is a company-sponsored retirement savings plan where workers can contribute a portion of their paycheck toward long-term retirement savings. Contributions are usually made before taxes, so the money you invest can grow tax-deferred until it is withdrawn. The plan is named after Section 401(k) of the Internal Revenue Code, which was added when Congress passed the Revenue Act of 1978.

401(k)s took off in the 1980s as companies began shifting away from traditional pension plans. Today, they’re the most common retirement savings plan for private-sector workers. However, not all jobs offer a 401(k). Public-sector employees and nonprofit workers may instead have access to a 403(b) or 401(a) employer-sponsored plan that have their own set of rules and benefits.

How Does a 401(k) Work?

As the owner of a 401(k), you make elective deferrals to fund your plan. This means you get to choose how much of your paycheck you want to contribute throughout the year and up to IRS limits. Designated contributions are automatically deducted and invested in options like mutual funds, exchange-traded funds (ETFs), stocks, bonds and money market funds.

Here's how that money you invest really gets to work. With a 401(k) your contributions grow tax-deferred and compound over time, which can help you build savings faster. Then when you reach retirement age, you can tap into your account as an important stream for steady retirement income.

What Are the Current 401(k) Limits in 2025?

Each year, the IRS adjusts 401(k) contribution limits to keep pace with factors like inflation and cost of living. The 401(k) limits in 2025 are as follows:

- Employee contribution limit: $23,500

Who is it for? This is the standard contribution limit for anyone with a 401(k).

- Catch-up contribution: Additional $7,500

Who is it for? This is for people 50 and over with a 401(k). Catch-up contributions allow individuals to make higher contributions to help boost their 401(k) as they get closer to retirement age.

- Higher catch-up (age 60–63): Additional $11,250

Who is it for? This is for people ages 60 through 63 with a 401(k). High catch-up contributions are an upgrade from regular catch-up contributions and can only be taken advantage of for a limited time—so don’t miss out!

What Types of 401(k)s Are There?

There’s not just one way to save, there are two main types of 401(k)s you may find in your company’s benefit package. Then the main difference between the two types of 401(k)s is how and when you pay taxes.

Traditional 401(k)

With a traditional 401(k), contributions are made with pre-tax dollars. This lowers your taxable income now, but you’ll pay taxes on withdrawals in retirement. A traditional 401(k) can be best for people who expect to be in a lower tax bracket after they retire.

Roth 401(k)

With a Roth 401(k), contributions are made after taxes, so you won’t pay taxes on qualified withdrawals in retirement. A Roth 401(k) has the same contributions limits as a traditional 401(k), which means you can make higher contributions compared to a comparable Roth IRA plan. A Roth 401(k) can be best for those who expect to be in a higher tax bracket in the future.

Remember, you don’t necessarily have to go all in on one plan. Some employers offer both traditional and Roth 401(k) options, allowing you to split contributions between the two.

What Are the Benefits of a 401(k)?

Your 401(k) plan comes with a wide range of benefits, so make sure you don’t miss out built-in tools that can grow your savings. Whether you’re wondering how a 401(k) match works or how to adjust contributions, check out these benefits that come with 401(k)s:

- Employer matching contributions: Some employers offer a 401(k) match to your contributions; basically, free money added to your retirement savings. This can either be a full match (meaning your contributions are matched dollar for dollar) or partial match (using a percentage formula). Employer matching contributions do not count towards your individual annual contribution limit which can help boost your account.

- Tax advantages: Contributions lower your taxable income in your working years, and your investments grow tax-deferred in a traditional 401(k). This means you won’t pay taxes on gains until you withdraw the money.

- Compounding growth: Over time, your earnings generate returns, which then earn returns themselves. Taking advantage by contributing early can help grow your 401(k) in the long run.

- Flexible contributions: Within plan and IRS rules, you can adjust how much of your paycheck goes into your 401(k) at any time.

- Your savings belong to you: The money you contribute is yours, and if you change jobs, you can take it with you.

- Easy to manage: You can set up automatic contributions from your paycheck, making it a simple “set-it-and-forget-it” way to save. · Rollover options: You can roll over your 401(k) into other retirement products like an annuity to help secure guaranteed income for life.

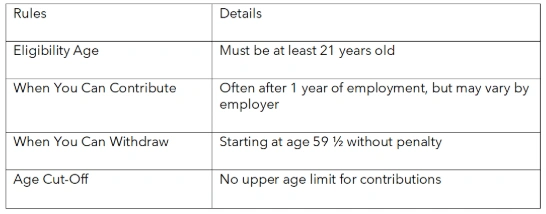

What Are the Rules for a 401(k) Plan?

Your 401(k) can do a lot for you, but there are some rules you should keep in mind. Here’s a quick summary of 401(k) plan rules to know:

401(k) plans are built to save money long term. So, if you tap into funds early, you can run into some penalties. Early withdrawals (before you turn 59½) usually face a 10% penalty and income taxes.

Additionally, once you reach age 73 (or 75 for those born after 1960), you’ll be required to take Required Minimum Distributions (RMDs) for a traditional 401(k). RMDs are calculated each year based on your account balance and life expectancy. Have a Roth 401(k)? You’re in the clear. You do not have to take RMDs from Roth 401(k) following rule changes from the SECURE 2.0 Act passed in 2024.

Your 401(k)’s Role in Retirement Planning

A 401(k) is a powerful savings tool that offers tax advantages and long-term growth, but it’s only part of a complete retirement strategy. By combining your 401(k) with a diversified portfolio, including stocks, bonds, and guaranteed income products like annuities, you can reduce risk and be confident in your future.

At Canvas Annuity, we offer simple, secure annuities that can work alongside your 401(k). Whether you’re early in your career or nearing retirement, having a thoughtful, flexible plan can make all the difference.

Resource Hub