Updated: March 7, 2024

What Is an Immediate Annuity | Are There Better Options?

Annuities are like a financial security blanket—they help alleviate your anxiety around retiring by providing you with guaranteed income in retirement.

Immediate annuities are one of the most common types of annuity. They’re unique because once you fund them, they begin to pay you back almost immediately.

In this article, we explain what immediate annuities are and how they work. We also cover their advantages and disadvantages, and we discuss who could benefit the most from them.

What Is an Immediate Income Annuity?

Annuities are powerful life insurance products. You purchase an annuity by paying a premium—either all at once in a lump sum of money or through regular payments over a period of time. Then, later, your money plus any earnings are paid back to you in a steady stream of income.

An immediate income annuity, sometimes also called an “instant annuity,” is a type of annuity where the payouts begin very soon after you buy it—usually within a year. It is distinct from a deferred annuity because deferred annuities pay out many years in the future, giving the money time to accumulate earnings.

How Does an Immediate Annuity Work?

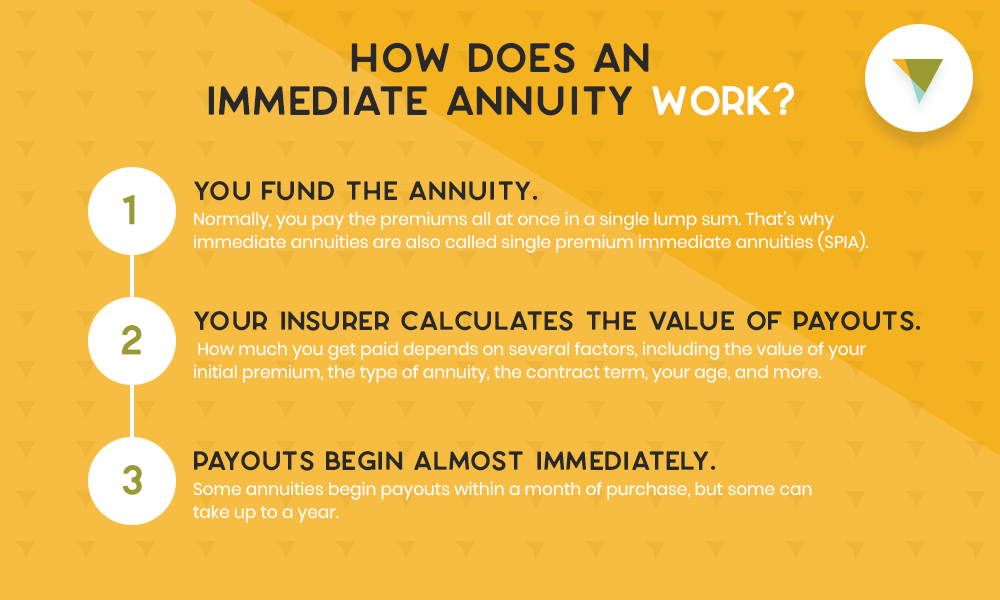

Immediate annuities work like this:

- You fund the annuity. Normally, you pay the premiums all at once in a single lump sum. That’s why immediate annuities are also called single premium immediate annuities (SPIA).

- Your insurer calculates the value of payouts. How much you get paid depends on several factors, including the value of your initial premium, the type of annuity, the contract term, your age, and more.

- Payouts begin almost immediately. Some annuities begin payouts within a month of purchase, but some can take up to a year. Once the payments start, you can sit back and enjoy the security that comes with steady retirement income.

Types of Immediate Annuities

There are many different types of annuities, even within the “immediate annuity” category. Each is designed for different financial circumstances and preferences. If you’re unsure about which is right for you, consult with a financial professional.

Fixed immediate annuities. This is the most common type of immediate annuity. With fixed immediate annuities, you receive a set periodic income. This value stays the same throughout the annuity contract term. Typically, you can choose whether you receive annual, quarterly, or monthly income payments.

Variable immediate annuities. This type of annuity is a tad more complex. With this type of annuity, stock market performance determines your payouts to some extent. When you buy a variable annuity, you select a number of sub-accounts to place your funds into. These act like mutual funds and are invested in a set of assets, like stocks and bonds.

Depending on the performance of these investments, your annuity payments may be higher or lower. Just like with other kinds of investments that rely on stock market performance, you may lose money with variable annuities.

Inflation-protected annuities. This type of immediate annuity guarantees a real rate of return. Your payments adjust up or down depending on whether inflation increases or decreases. This ensures that your payments increase during periods of inflation, so you don’t lose the purchasing power of your annuity. On the other hand, in periods of deflation, your payments decrease.

Lifetime immediate annuities. In a life annuity, your payments last for the rest of your life. These annuities ensure you always have at least some income for as long as you’re alive.

Term immediate annuities. In a term annuity, sometimes called a “period certain annuity,” your payments last for the term specified in your annuity contract.

For example, if you purchase a 10-year immediate annuity, payments will last for 10 years—and no more.

Immediate vs. Deferred Annuities

If you don’t need your payments to begin right away, it may be advantageous to choose a deferred annuity.

In a deferred annuity, you pay your premium and allow the money to earn interest over a set period of time. Depending on the contract, you can pay your premium in one lump sum, or you can choose to pay it over a number of years. The latter is advantageous for anyone who doesn’t have a big chunk of retirement savings already saved up.

You also choose an annuity contract term, i.e., the amount of time you want the annuity to collect interest. (Deferred annuity contract terms are usually between 3 and 10 years.) Over that time, your account earns interest and accumulates in value. Then, at the end of the term, you can choose to annuitize and convert your annuity to start paying you back.

Or, you can leave your money in the contract and let the money continue to grow.

Advantages and Disadvantages of Immediate Annuities

Immediate annuities have some powerful benefits, but they have significant disadvantages too. Let’s have a look at both the benefits and drawbacks of immediate annuities.

Advantages

Immediate annuities are great for people about to retire or already in retirement. They can help supplement other investments, retirement savings, and social security checks with an immediate source of income. Here are some of the benefits of an immediate annuity for retirees.

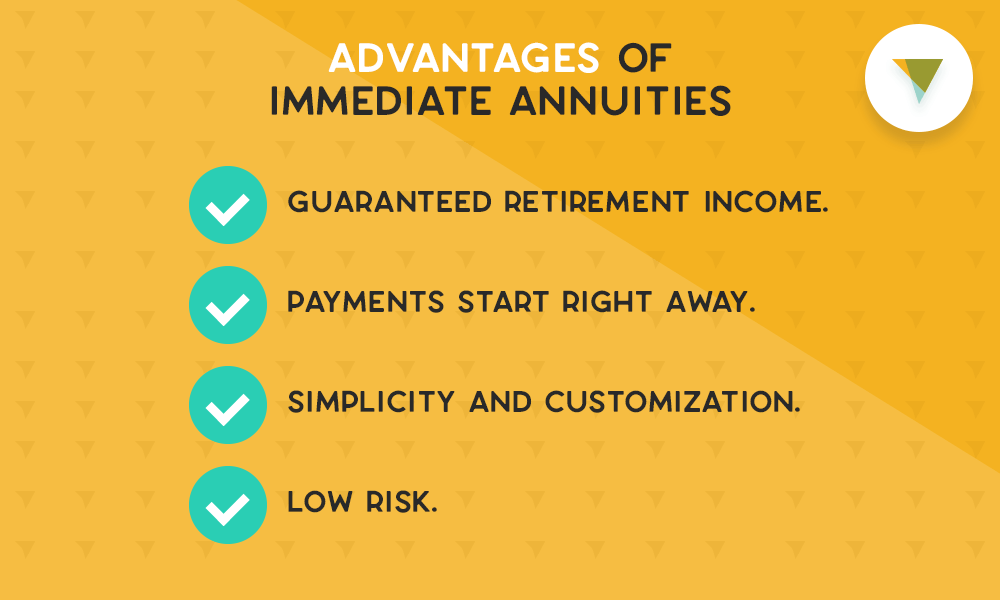

- Guaranteed retirement income. Like all annuities, the major advantage of immediate annuities is that they provide a steady stream of retirement income. Guarantees are backed by the financial strength of the issuing life insurance company.

- Payments start right away. If you're close to retirement or already retired, immediate payments are great. Immediate annuities allow you to start receiving your retirement income as soon as possible.

- Simplicity and customization. The classic fixed immediate annuity is very straightforward to understand. You pay your premium and then start receiving your income soon after. Most also offer customized add-ons like cost-of-living adjustments, joint-life policies for spouses, and more.

- Low risk. Your fixed immediate annuity income won’t be affected by stock market volatility. So if the market tanks and your other investments lose money, you’ll feel secure knowing you still have your steady annuity income. (Note that this doesn’t apply to variable immediate annuities.)

Disadvantages

Immediate annuities aren’t for everyone. Here are some of the drawbacks to this type of annuity.

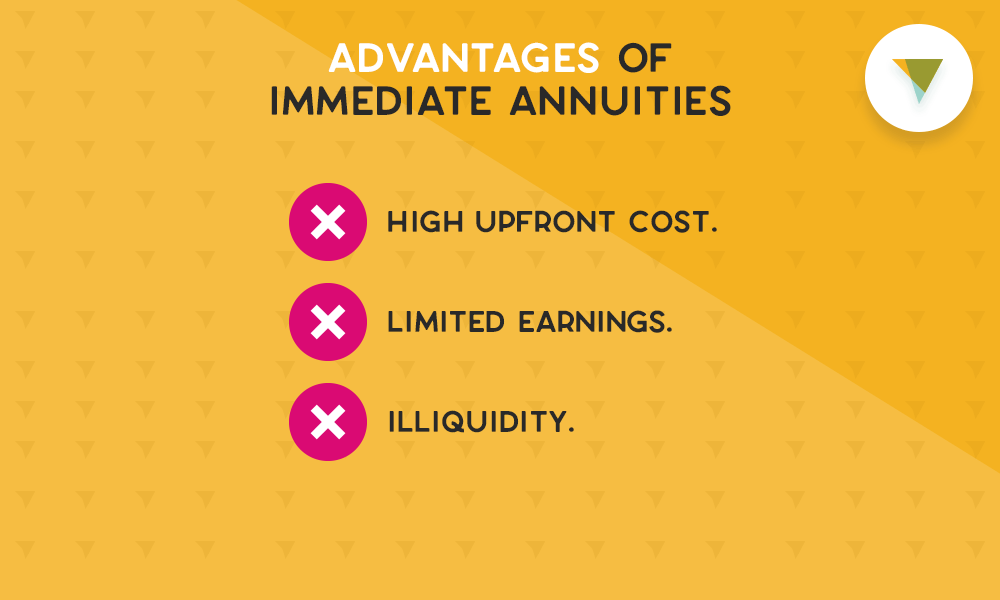

- High upfront cost. You need a lot of starting capital to fund an immediate annuity. For lots of people, it’s much easier to fund a deferred annuity in a series of payments over several years.

- Limited earnings. Immediate annuities don’t give your money a chance to earn or accumulate in value. In contrast, deferred annuities provide much more earning potential with good interest rates.

- Illiquidity. Liquidity is how easily you can convert an asset to cash. With immediate annuities, your money is locked up. You can’t withdraw from an immediate annuity; you just have to wait until it’s paid back to you over time.

- Finding the right insurance company to buy from. SPIA payments have an interest component built-in; the insurance company doesn’t just return your premium back to you over time, they also pay you interest. The SPIA market is very competitive which can be a good thing for consumers but can be confusing. You want to make sure you get the best rate but also purchase with a company that you trust with your hard-earned savings.

Is an Immediate Annuity Right for Me?

Immediate annuities are ideal for those already in retirement or very close to it, and who need their payments to start now. They are a great personal finance tool if you want to turn your retirement savings into a steady income that will last you the rest of your life.

But they’re not right for everyone. If you’re not yet close to retirement, or even if you’re in retirement but can wait a few years before you need income payments, a deferred annuity may be a better option.

Deferred annuities typically provide much higher crediting rates. They also tend to let you withdraw your money early if you need to, making them more liquid. (However, it's best to check your deferred annuity contract for your specific terms and conditions.)

Immediate Annuities Start Sooner but Deferred Annuities Earn More

Immediate annuities provide individuals with immediate guaranteed lifetime income. They’re a great way to turn your retirement savings into reliable income so you can be sure you’ll always have some cash coming in.

But they’re not ideal if you don’t need your payments right now. If you can wait a few years, deferred annuities will also provide you with guaranteed income, and you’ll receive much more than you started with. Plus, deferred annuities offer more flexibility than immediate income annuities.

Canvas Annuity offers some of the highest fixed deferred annuity rates in the business. Our annuity products are safe, straightforward, and easy to buy online. Get in touch with our licensed representatives to learn more about how a deferred annuity can fit into your retirement plan and provide you with a guaranteed retirement income.

Resource Hub