Updated: December 23, 2025

Single Premium Immediate Annuities: The Pros and Cons

A single premium immediate annuity (SPIA) is a contract with an insurance company where you pay a single premium upfront in return for guaranteed income. Payments begin immediately or soon after you purchase the annuity.

As you approach retirement, you might be worried about how you’re going to afford it. Ideally, you’ll be able to create multiple sources of retirement income.

The SPIA is one tool among many that can help you generate guaranteed retirement income. In this article, you’ll learn what SPIAs are, whether they’re a good choice for you, and how they compare to other options.

What is an SPIA?

The SPIA is a specific type of annuity. It sounds complicated, but it’s fairly straightforward.

SPIAs are annuities. Annuities are financial instruments designed to guarantee a consistent income stream over a specified period — typically for securing retirement finances. There are many different kinds of annuities, each with unique terms and conditions.

SPIAs are “single premium.” In the context of annuities, a premium refers to the initial payment you use to buy the annuity and start your annuity contract. A single premium means that you fund the annuity in one big lump sum payment. Other annuities have “flexible premiums” that you fund with several payments over time.

SPIAs are immediate annuities. This means that they begin to pay you an income right away — no more than a year after your purchase. Other annuities are “deferred,” which means that they earn interest in your account for a time before your income payments start.

In summary, a single premium immediate annuity (SPIA) is an annuity contract that you fund in a single, lump sum payment and that begins to pay you income right away.

How Does an SPIA Annuity Work?

First, you agree to the terms of the contract. Then you fund the annuity with your initial investment. Finally, you begin to receive payments.

Let’s explore each step in detail.

- Establishment of income terms. When you purchase an SPIA, you agree on the terms with the insurance company regarding how much income you'll receive and how frequently. Your income depends on several factors, like the amount of your premium, your age, your life expectancy, and the payout options you choose.

- Fund your annuity. Next, you fund your annuity. In the case of an SPIA, you make a single, lump-sum payment to your annuity company. You can usually pay the premium from a savings account or with retirement funds that you've accumulated over the years.

- Receive your payments. An SPIA begins to pay you back immediately. You usually get to choose if you want your payments monthly, quarterly, or annually.

When do your payments stop? It depends on your contract. You might choose to receive payments for a designated number of years ("period certain"). Or, you might choose to receive payments for the rest of your life ("life annuity").

Finally, you might be able to add on some extras.

For example, you might be able to add death benefits, which would transfer money remaining in your annuity to a beneficiary after you die. Or, you could opt for a joint life annuity, where your annuity continues to pay out while either you or the joint annuitant (usually your spouse) is alive.

Pros and Cons of SPIA Annuities

SPIAs are designed for a specific use case —converting a chunk of cash into a guaranteed income. That might be exactly what you need, or it might not be the right fit for you.

Here, we go through the advantages and disadvantages of SPIAs.

Pros of SPIA Annuities

SPIAs offer several compelling benefits that make them an attractive choice for some individuals. Here are specific advantages of SPIAs:

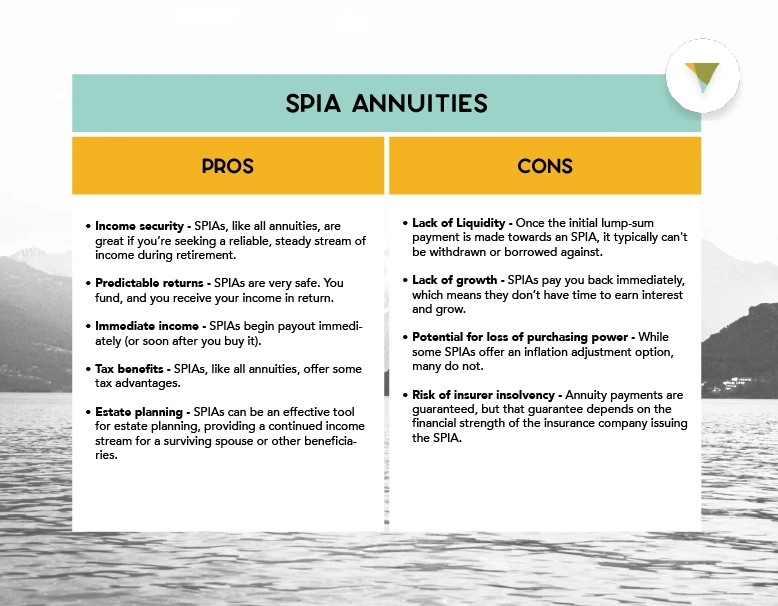

- Income security. SPIAs, like all annuities, are great if you’re seeking a reliable, steady stream of income during retirement. Once the SPIA contract is established, regular payments are guaranteed.

- Predictable returns. SPIAs are very safe. You fund, and you receive your income in return. This makes SPIAs a great choice for individuals who are risk-averse or who want to ensure a predictable income.

- Immediate income. SPIAs begin payout immediately (or soon after you buy it). That’s beneficial for those who require an immediate income source, such as recent retirees.

- Tax benefits. SPIAs, like all annuities, offer some tax advantages. Part of each payment is considered a return on the original investment and thus is not taxed, reducing the overall tax burden.

- Estate planning. SPIAs can be an effective tool for estate planning, providing a continued income stream for a surviving spouse or other beneficiaries.

Cons of SPIA Annuities

Despite the numerous benefits associated with SPIAs, they have certain limitations and potential pitfalls that should be kept in mind:

- Lack of Liquidity. Once the initial lump-sum payment is made towards an SPIA, it typically can't be withdrawn or borrowed against. Your money is stuck there and will only be paid to you as an income payout. This can pose a challenge if unexpected expenses crop up.

- Lack of growth. SPIAs pay you back immediately, which means they don’t have time to earn interest and grow. On the other hand, deferred annuities can grow your money with relatively low risk and good interest rates.

- Potential for loss of purchasing power. While some SPIAs offer an inflation adjustment option, many do not. If your SPIA doesn't adjust for inflation, the fixed income stream could lose real value over time as the cost of living rises. This could potentially erode the purchasing power of the annuity payments in the long term.

- Risk of insurer insolvency. Annuity payments are guaranteed, but that guarantee depends on the financial strength of the insurance company issuing the SPIA. If the insurer faces insolvency, it could impact your annuity payments. While there are some state guaranty associations that protect annuities, it's essential to consider the financial stability of the insurance company when purchasing an SPIA.

Navigating these potential downsides requires a solid understanding of your financial landscape and careful planning. It's crucial to weigh these factors against the benefits to ensure an SPIA aligns with your long-term financial goals.

SPIA Annuities Compared to Other Annuity Types

SPIAs differ from other annuity types in a few key ways. Here's a closer look at these differences.

Fixed Deferred Annuities vs. SPIAs

Fixed annuities are the classic type of annuity. You fund your annuity. Then it grows at a fixed interest rate. Then you can annuitize it and start receiving your income.

They’re “fixed” because the interest crediting rate never drops below the fixed minimum specified in your contract.

One major distinction between fixed annuities and SPIAs is in the payout timing. While SPIAs begin making income payouts immediately or within a year of purchase, deferred annuities delay income payouts — often for several years — allowing your investment to grow.

Another difference is that fixed annuities often offer flexible premiums. That means that you can contribute to them in several premiums over time rather than in one lump sum.

Variable Deferred Annuities vs. SPIAs

Variable annuities are also deferred, meaning that you’ll receive your income payments often years after you buy this annuity. But unlike fixed annuities, the crediting rate is variable. It’s tied to a set of investments that you choose.

That makes variable annuities more risky than deferred annuities —if your investments tank, you could lose your money. On the other hand, if your investments do well, you could earn more money than with other types of annuities.

While SPIAs offer income certainty, variable annuities introduce the potential for higher returns (along with higher risk).

Equity-Indexed Annuities vs. SPIAs

Fixed-indexed annuities (or equity-indexed annuities) are a kind of hybrid between fixed annuities and variable annuities. They offer returns tied to a specific market index, which can result in higher potential returns than an SPIA would. However, this also comes with a greater level of risk, as returns can be lower if the linked index performs poorly.

Again, SPIAs offer a guaranteed income now. Equity-indexed returns offer the potential for growth (and higher returns) later but with some risk.

SPIAs vs. MYGAs

Multi-year guaranteed annuities (MYGAs) are a specific kind of fixed annuity. They guarantee a fixed interest rate for a certain term period —usually three, five, or seven years. Your money grows during that time, and at the end of the term, you have the option to turn it into a stream of income.

So SPIAs pay you back right away but with lower returns. MYGAs pay you back later, but your money grows steadily over time.

Who is an SPIA Annuity Right For?

After all those details, is an SPIA right for you?

SPIAs essentially convert a chunk of your retirement savings into an immediate, guaranteed income. They might be right for you if:

- You’re currently in retirement or close to it and want a retirement starting very soon.

- You need your income now. SPIAs give you an income immediately.

- You have already saved up a comfortable nest egg. SPIAs are funded with a single, lump-sum premium payment.

- You can spare some of your nest egg to go into an annuity and are confident you won’t need to access it. SPIAs tie up your money and make it unavailable until you get it back as income.

- You don’t need to grow your nest egg anymore. SPIAs don’t grow your money over time.

- You’re looking for low-risk. SPIAs provide guaranteed income. If you’re looking for higher-risk investments with larger returns, SPIAs may not be ideal.

If that sounds like you, SPIAs could be right for you. Ultimately, the decision to opt for an SPIA depends on your unique financial circumstances and objectives.

If you’re not sure, consider consulting with a financial advisor to help you understand whether an SPIA aligns with your specific needs and that you’re making an informed decision about your retirement income strategy.

Annuities Provide Peace of Mind

SPIAs convert some of your retirement savings into a guaranteed stream of income that starts very soon. If you have the money to do it and you need the income immediately, they’re a good option.

If you don’t need the income immediately, fixed annuities may be a better option.

Fixed annuities let you grow your savings at a guaranteed interest rate for a few years before receiving your income.

Canvas Annuity offers some of the highest crediting rates in the industry on our fixed annuity products. They’re also designed to be simple with no fees. Have a look, and feel free to contact our licensed reps with any questions.

Resource Hub