Table of Contents

Updated: June 2, 2026

Annuities are insurance contracts that can deliver guaranteed income in retirement. Before you buy, it’s important to know how you’ll fund the annuity—with pre‑tax (qualified) or after‑tax (non‑qualified) dollars—because funding source drives taxes, RMD rules, and access to money.

This guide explains qualified vs. non‑qualified annuities in plain language, shows when each makes sense, and answers common questions.

Funding Your Annuity

When you (the owner) purchase an annuity, you’re essentially buying a contract from an insurance company.

You fund the annuity with a set amount of money (the premium), and it grows over time.

Then in retirement, the insurance company provides the person you choose as the annuitant (many times the owner makes themself the annuitant) with retirement income in the form of annuity payout options. That’s right—annuities provide guaranteed income in retirement.

But before you can reap the benefits of an annuity, you have to buy one. And where the money comes from to fund the annuity can impact how your retirement income is taxed and when you’ll be able to begin receiving payouts. Let's dig into the two types of annuity funding.

Non-Qualified Annuities

A non‑qualified annuity is funded with money that has already been taxed (after‑tax dollars). These dollars can come from savings accounts, CDs, brokerage accounts, or other vehicles that hold money you’ve already paid taxes on.

A benefit to non‑qualified annuities is that there is no government‑mandated contribution limit, unlike IRAs and many workplace plans. (Your insurer may set deposit limits, commonly $500,000–$1,000,000.)

Another benefit of buying an annuity with after‑tax dollars is that you are not required to start taking payouts at a certain age.

Like Roth IRAs, the IRS does not require you to take payouts from a non‑qualified annuity, meaning your money can keep growing.

Growing Funds

When you withdraw money from a non‑qualified annuity—whether it’s a lump‑sum payment or a series of payments—no taxes are due on the principal (your after‑tax contributions). Earnings are taxable as ordinary income, and under LIFO rules the first dollars out are treated as earnings.

Money withdrawn from principal (your “cost basis”) is tax‑free because taxes were already paid on it.

Exclusion Ratio Defined

The exclusion ratio determines what portion of each annuity payout is a return of principal (non‑taxable) versus earnings (taxable). For life‑only or life‑contingent payouts, life expectancy is part of the calculation.

If you live beyond the calculated life expectancy, subsequent payments are fully taxable as income.

Example: A 70‑year‑old purchases an immediate annuity with a $20,000 premium and an expected total payout of $32,500. The exclusion ratio is $20,000 ÷ $32,500 = 61.5%. If the monthly payment is $200, then roughly $123 (61.5%) is excluded from income and $77 is taxable. Your insurer will provide the exclusion‑ratio details for your contract.

Qualified Annuities

A qualified annuity is funded with pre‑tax, tax‑deferred dollars from qualified accounts such as traditional IRAs, employer 401(k)s, or 403(b) plans.

Because they use tax‑deferred money, qualified annuities are subject to required minimum distribution (RMD) rules.

RMD starting age:

Updated for 2025: RMDs generally begin at age 73 (rising to 75 in 2033).

Excise‑tax penalty for missed RMDs:

Updated for 2025: 25% of the shortfall (reduced to 10% if corrected in a timely manner).

Taxation: Withdrawals from a qualified annuity are generally 100% taxable as ordinary income because contributions and growth were tax‑deferred.

Like 401(k)s and IRAs, the minimum age threshold to make qualified withdrawals without the early‑distribution penalty is 59½. Earlier withdrawals may incur a 10% federal penalty (plus any applicable surrender charges).

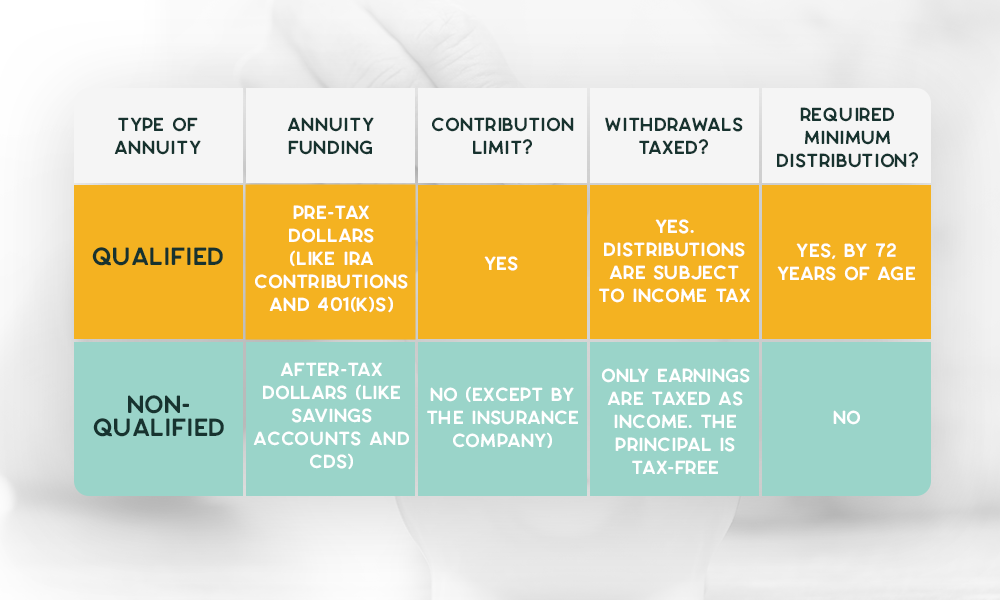

Qualified vs. Non-Qualified Annuities - Quick Comparison

Remember that the primary difference between qualified and non-qualified annuities is how they are taxed and when you want to access money. And as we discussed, there are a handful of critical factors that should drive your decision, including contribution limits, required minimum distribution, and income tax rules.

Here's a snapshot of the differences between qualified and non-qualified annuities:

* Table is an educational summary, not tax advice. Confirm specifics with your tax professional.

Choosing the Right Type of Annuity for You

The right structure depends on your tax situation, funding source, and retirement income goals. A licensed professional or tax advisor can help you evaluate trade‑offs.

Key questions to discuss with your advisor:

- Will funding with qualified or non‑qualified dollars reduce my lifetime tax bill?

- Do RMDs at age 73 fit my plan—or would non‑qualified funding provide more flexibility?

- What payout options (life‑only, period‑certain, joint life) align with my needs?

- Should I consider a COLA (inflation) rider?

What Is a Non‑Qualified Annuity?

Definition recap: A non‑qualified annuity is funded with after‑tax dollars; withdrawals are taxed on earnings only, while your original contributions (basis) come back tax‑free. There are no IRS‑mandated RMDs.

Qualified vs. Non‑Qualified Annuity: Which Is Better?

It depends on your situation. If most of your savings are pre‑tax, a qualified annuity may integrate cleanly with RMDs and rollover rules. If you want distribution flexibility and to avoid RMDs, non‑qualified funding can help—while still deferring taxes on growth. Model both with a tax professional.

Qualified and Non‑Qualified Annuities: Practical Examples

Example 1 (Qualified): Rolling a portion of a 401(k) to a traditional IRA and purchasing an immediate annuity to cover essential expenses in retirement; RMDs begin at 73.

Example 2 (Non‑Qualified): Investing after‑tax savings into a deferred fixed annuity to grow tax‑deferred and later annuitize a portion for guaranteed income, with no RMD requirement.

Frequently Asked Questions

Is a non qualified annuity taxable?

Earnings are taxable as ordinary income when withdrawn. Your after‑tax contributions (basis) come back tax‑free.

Do I have to take RMDs from a non qualified annuity?

No. RMDs apply to qualified annuities funded with pre‑tax dollars. Non‑qualified contracts are not subject to RMDs.

What is the RMD age for qualified annuities?

Generally 73 in 2025 (rising to 75 in 2033). Missing an RMD may trigger a 25% excise tax, reduced to 10% if corrected promptly.

Citations

1. Smart Asset (Lake, January 2020), Non qualified vs qualified annuities www.smartasset.com

2. Insured Retirement Institute, (Buckingham, 2018), The Truth About Annuities https://irionline.org/

Resource Hub