Updated: July 28, 2025

How to Prepare for Healthcare Costs in Retirement

What You Don’t Want to Underestimate in Retirement

Healthcare is one of the most significant expenses retirees face. We’re talking more than annual doctor’s visits and medication. Any major surgeries, on-going treatment, and the big one, long-term care, can have you feeling the strain if you are not prepared.

Understanding what to expect and how much you should have saved can make a difference for your overall retirement strategy. In this article, we’ll walk through what health insurance like Medicare does and doesn’t cover, the average cost of healthcare in retirement, and ways to save for future healthcare expenses.

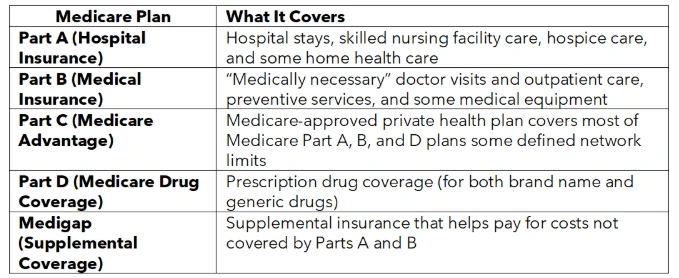

What Does Medicare Cover?

Medicare is a federal health insurance program available to people starting at age 65. There are different parts of Medicare, each covering different services. What are your plan options under Medicare? Here’s a quick round up:

What Does Medicare Not Cover?

While Medicare covers many essential health services, it doesn’t cover everything. Understanding what’s excluded can help you plan for additional costs.

Here are some common Medicare exclusions retirees should know about:

- Long-term care (help with daily activities like bathing or dressing at home or in a facility)

- Dental care (with some exceptions related to specific medical treatments)

- Hearing aids and fittings

- Eye exams and prescription eyeglasses

- Massage therapy

- Cosmetic procedures

These services must be paid out of pocket unless you have separate insurance or a savings plan in place.

Know When To Apply for Medicare Coverage

Ready to get on Medicare? Make sure you don’t miss your Initial Enrollment Period to avoid late enrollment penalties. The Initial Enrollment Period for applicant starts three months before the 65th birthday and ends three months after your birth month. Missing this window could add permanent penalties to your plan, like fixed higher monthly premiums that go up the longer you delay signing up.

You can make changes to your plan annually during the open enrollment period, but it’s important to know that won’t change premium rates that are locked in based on when you first enroll. The earlier you plan, the better.

Planning for Long-Term Care

With Medicare basics out of the way, let’s get into one of the highest healthcare costs you need to save for in retirement—long-term care. Long-term health care refers to services that can include medical and non-medical support with daily activities and is not covered by traditional Medicare. This type of care can include:

- Home health care: Care provided at home by aides or nurses

- Community care/assisted living: Shared living spaces with support services

- Nursing homes: Full-time medical and personal care facilities

These services that many retirees will eventually need do not come cheap. According to a 2024 study from Genworth home health care can average over $6,000/month, assisted living communities $5,900/month, and nursing home care anywhere from $9,000 to $10,000/month. That means you need to be prepared for a pretty significant amount of your nest egg to cover essential care when it becomes necessary.

How To Save for Healthcare in Retirement

Now that you know the costs and what is and is not covered by Medicare, how can you prepare? Along with growing a healthy 401(k), it’s worth considering these saving strategies for healthcare costs in retirement:

Health Savings Account (HSA)

This way to save for medical expenses is available if you have a high-deductible health plan. Contributions are tax-free, growth is tax-free, and withdrawals for qualified medical expenses are tax-free

Premiums are typically lower, but account holders typically need to pay more out-of-pocket before insurance coverage kicks in. You cannot contribute to an HSA if you are enrolled in Medicare, but you can still use existing HSA funds on qualifying medical expenses.

Health Coverage with COBRA

The Consolidated Omnibus Budget Reconciliation Act (COBRA) is a way for retirees to temporarily continue your employer’s health insurance after leaving a job, often bridging the gap before Medicare.

COBRA is more of a safety net than a long-term solution. Qualifying for COBRA extends a retiree’s employee-sponsored health coverage for up to an additional 18 months.

Diversifying Your Portfolio

Investing across a mix of stocks, bonds, and annuities can help grow your savings while managing risk. Stocks can offer higher growth, bonds add stability, and annuities, like what we offer at Canvas, can provide guaranteed income to help with essential costs like healthcare.

Diversification is important because it can protect your income from market swings. Knowing you have secure income sources is crucial, especially if you are faced with unexpected medical expenses.

Long-Term Care Insurance

Long-term care (LTC) insurance can help provide coverage for retirees since long-term care is not covered under Medicare or most other health insurance plans. They work like traditional insurance plans where you pay premiums to a policy that can provide funding for long-term care when you need it.

You can purchase LTC insurance on its own, but some insurance companies offer bundled policies with life insurance.

Long-Term Care Annuity

A long-term care annuity is a type of deferred annuity that includes built-in or optional long-term care benefits. These hybrid products combine the growth potential of a traditional annuity with added coverage and benefits similar to long-term care insurance.

Do You Know All the Costs of Retirement?

Healthcare is just one of many essential costs you’ll face in retirement. Housing, food, travel, and inflation all add up, so make sure you have a solid financial plan. With tools like HSAs, long-term care planning, and guaranteed income from annuities, you can be better prepared.

At Canvas, we can be part of that plan with fixed annuities that provide guaranteed income for life. By planning ahead, you can spend less time worrying and more time enjoy your retirement years.

Resource Hub