Updated: February 27, 2026

Retirement Savings Goals by Age: How Much Should You Have to Retire?

Experts recommend that you save the equivalent of your annual salary by age 30. Then, they suggest saving three times your annual salary by 40, six times your annual salary by 50, and eight times your annual salary by 60 years old. By the time you’re ready to retire, you should have 10 times your annual income saved.

The problem with planning for retirement is that it’s uncertain. How long will you live? How much will your lifestyle cost? Will you have any trouble with your health? If you knew the answers to these questions, it would be easier to know how much money you’ll need to retire.

Unfortunately, we don’t know the answers to those questions. Instead, we typically use guidelines—rules of thumb—to help people ensure they save enough. Experts recommend that, by the time you’re 67, you’ll have saved 10 times your annual salary.

That’s a lot of money. It may even feel impossible to do, but if you save over time, it’s easier. In this article, we give guidelines for retirement savings goals by age and provide suggestions about how to meet those goals.

How Much Do You Need to Retire?

There are two important factors in planning your retirement finances: income and savings. You can invest savings and earn an income. With a large enough average retirement income, you won’t eat into your savings. That means you can live sustainably.

How Much Retirement Income Do You Need?

For retirement income, experts recommend trying to earn at least 80% of your annual pre-retirement income. For example, if your annual salary was $80,000 a year while you worked, you would want to set yourself up to earn $64,000 a year in retirement income.

That’s one benchmark. Of course, how much you need to retire depends on many factors. If you plan to live lavishly, you may need more than $1 million to retire. If you plan to live modestly, you may need much less. It also depends where you live: some cities are more expensive than others.

How Can You Earn a Retirement Income?

We’ve written a full guide on the best ways to invest for a retirement income, but the top sources of income for retirees besides social security are annuities, retirement income funds, rental real estate, and investments in securities.

- Annuities: Annuities work like private pensions. You pay premiums to an insurance company and fund your annuity. Depending on the type of annuity you buy, your account accumulates interest, tax deferred. Then, when you reach retirement age, you can annuitize and begin taking withdrawals. When you annuitize you can select from different income options, from a set amount for a short amount of time or guaranteed income for the rest of your life. Guaranteed lifetime income makes an annuity an important consideration when creating you’re retirement income plan.

- Retirement Income Funds (RIFs): RIFs are a special type of mutual fund. They’re actively managed and usually are quite conservative. Keep them in your individual retirement account (IRA) or another retirement savings plan for additional tax benefits.

- Real estate: If you own real estate property, you can earn rental income. If you don’t, you can buy shares in real estate investment trusts (REITs) and earn some of the profits from companies that manage rental properties.

- Securities: You can invest in stocks, bonds, CDs, index funds, and mutual funds. Again, if you keep these in a retirement savings account, like a traditional IRA or a Roth IRA, you’ll benefit from significant tax benefits. Note that IRAs have contribution limits.

How Much Should You Have Saved by Age

That was retirement income. Now, let’s look at saving for retirement.

The trick to developing a retirement savings plan is to start early. It’s difficult to build up a big enough nest egg in just a few years. It’s much easier to do over a span of decades. Starting early means that you will benefit from compound interest. The money that you save continues to grow and earn you money towards your retirement fund.

To know you’re on track, set savings targets for yourself at different ages. One rule of thumb that financial planners use is to save a multiple of your annual income by certain ages. In the table below, we’ve provided recommendations on how much to save as a multiple of your annual salary. We’ve broken it down by decade.

For example, a 40-year-old making $50,000 a year should have between $150,000 and $200,000 saved. That is three to four times their annual income.

Another approach is to set a savings goal of some percentage each year. For example, some experts suggest saving 15% of your gross salary each year. This works best if you start in your 20s. If you start later, you may need to increase your savings rate to catch up. Other experts recommend saving as much as 25% of your gross salary. This might be a good strategy if you’re starting to save later—say, in your 40s.

What should you do to save now? Here are some tips, broken down by age group.

Savings Goals at 20

For most 20-year-olds, retirement is a long way off. It’s still critical to think about now—that way, you’re not playing catch up later. You should try to set aside 10% to 15% of each paycheck for retirement.

One good way to start is by putting money into an emergency fund. Experts recommend having an emergency fund of about three to six months worth of your salary. Keep this fund accessible—for example, in a high-yield savings account or a short-term CD. That way, it earns some interest while it’s sitting around but is easy to get to if you need to use it. Your emergency fund can ultimately be part of your retirement fund if you don’t need it. But if you lose your job or have an unexpected health issue, you’ll be glad it’s there.

Once you’ve saved up your emergency fund, put your 10% to 15% in a tax-advantaged account like an individual retirement account. This is a good time to talk to a financial advisor for advice on investments to grow your money faster.

Savings Goals at 30

Hello millennial, welcome to your 30s. By 30, you might be more settled in your career and earning more. You might have a young family or have recently bought a house. You may also still have student loans. These things can be expensive, but don’t let them distract you from saving for retirement.

What are some strategies you can use?

First, keep trying to save 15% of your income each year. Second, if you work for a company that offers a 401(k), take advantage of it—especially if your employer matches your contributions. You can subtract the amount your company matches from your 15% savings goal. For example, if your company matches 5% of your 401(k) contributions, you only have to put in 10%. That 10% plus your employer’s 5% gets you to the 15% target.

Savings Goals at 40

We typically hit our highest-earning years starting in our 40s and most people will have their student loans paid off, making this a good time to double down on saving. Especially if you’re behind, now is your chance to get back on track. Focus on hitting those retirement savings milestones.

Continue to put aside 15% of your salary. If you can, maybe bump it up to 20% or even 25%. Some of this can go to higher-risk investments, but it’s also a good time to start thinking about buying an annuity. Annuities are very safe, long-term investments for retirement. They provide guaranteed growth and can help you ensure a guaranteed income in retirement.

Savings Goals at 50

By the time you hit 50, retirement is around the corner. If you earn $50,000 a year or more, you should have at least $300,000 saved by now. If you’re a long way off from that, take a look at your budget and try to get on track. Consider talking to a personal finance professional to start seriously planning for retirement. Note that once you’re 50, you can contribute an extra $1,000 a year to your IRA as a catch-up contribution.

If you don’t have an annuity by now, consider buying one. Most experts recommend a fairly large portion of your portfolio kept in safe investments at this age. Annuities provide very good growth for being so low risk.

By the time you’re 59 1/2 you can start withdrawing from retirement accounts and annuities without tax penalties. But it’s better to put that off if you can. The longer your savings continue to grow, the more financial security you’ll have in retirement.

Savings Goals at 60

You may be about to retire. If you make $50,000 a year, you’ll hopefully have $500,000 saved for retirement. Ideally, it will also be earning interest.

At this age, there are still some decisions you can make to increase your retirement savings. One is choosing to receive your social security benefit later. The later you begin to take your social security income, the larger the benefit. You’ll get the largest benefits if you start claiming your benefits at 70.

You can still buy an annuity at 60. This is a low risk way to steadily grow your money. When you’re ready, you can annuitize and earn an income for the rest of your life.

Savings Goals at Retirement

By this time, hopefully, you’re set for retirement. The goal now is to convert your nest egg into a source of retirement income. If you bought an annuity, you can annuitize it and start receiving your income payments. Or, you may start taking systematic withdrawals from your retirement accounts. If you’re still short of your savings goals, you may choose to keep working—even part-time.

If you’ve planned well, you’ll earn a retirement income equal to about 80% of your working income. That will help you live sustainably for the rest of your life.

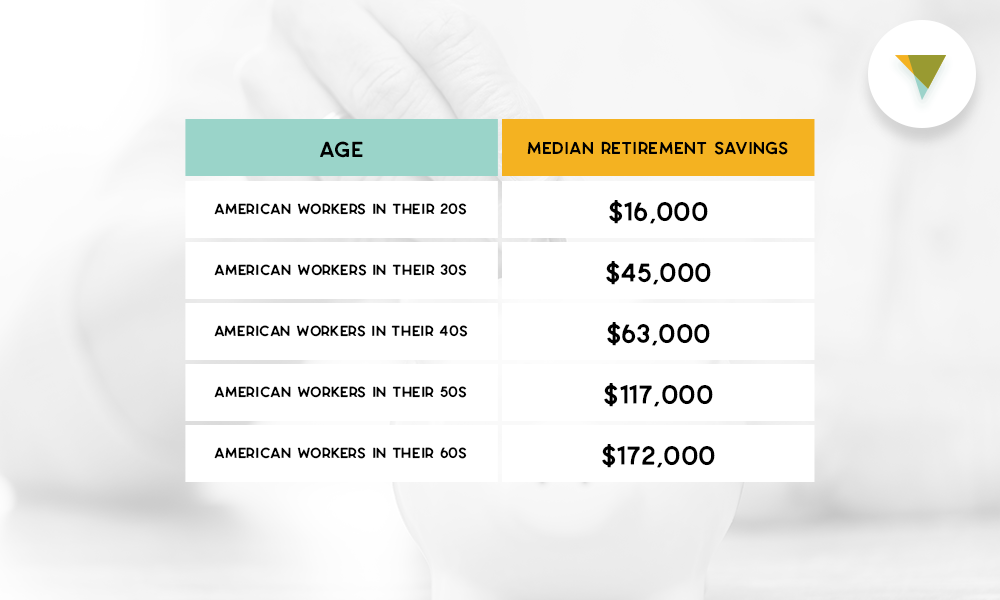

Median Retirement Savings by Age

Are you reading this article and feeling like you’re significantly behind? You’re not the only one. Very few Americans have achieved the savings targets that experts have set. Here are the statistics for the median retirement savings by age group:

Preparing for Retirement

There’s an old proverb that says, “The best time to plant a tree was 20 years ago. The second best time is today.” If you’re like most Americans, you’re not as prepared for retirement as you’d like to be. Perhaps you wish you started 20 years ago. Well, you can’t go back to the past, but you can start thinking about retirement now.

If you’re just starting, the following can be a useful rough guide.

- Start saving. Set aside at least 10% to 15% of your gross income each paycheck. If you’re starting later in life, try for 20% or even 25%.

- Decide where to put it. Make contributions to your 401(k) if you have one and contribute to your IRA or annuities for tax advantages.

- Think about your portfolio. Younger folks can have more risky asset classes, like stocks. Older folks should focus more on low-risk investments, like annuities.

- Plan your retirement income. Think about how to set yourself up to receive a retirement income. Again, annuities shine here. They are the only financial product that can guarantee you an income in retirement.

- Stick with the long term. Saving works best when you commit to it for many years. That’s how you’ll successfully prepare for retirement.

These are general steps that can help you achieve a comfortable retirement. Talk to a financial advisor for more specific financial planning and tax advice targeted at your particular situation.

Adding an Annuity to Your Retirement Portfolio

It might be uncomfortable to see the retirement savings recommendations by age. Lots of people aren’t where they would like to be. It can be scary thinking about retirement if you’re not well prepared for it.

At Canvas Annuity, we believe in the power of fixed annuities in helping people feel confident as they transition into retirement. Annuities provide something no other product can–certainty. They help you feel safe knowing that you’ll have income for the rest of your life. That peace of mind is priceless.

Annuities also help you achieve your savings goals because they can help you earn a significant interest rate. See the current fixed-annuity rates here.

If you’re looking for a low-risk way to meet your retirement savings goals, consider one of our annuities. Apply online today.

Resource Hub