Updated: March 7, 2024

What Is A Fixed Annuity?

A fixed annuity is a type of annuity contract issued by a life insurance company where the buyer receives a specific, guaranteed interest rate on the contributions they make to the account.

The accumulated money is paid out later as retirement income, usually in monthly installments. As the name implies, the insurance company offers a fixed minimum interest rate that stays the same throughout your annuity contract.

The company may (and often does) declare an interest rate higher than the minimum for a set period of time (as with a multi-year guaranteed annuity) or annually. The minimum interest rate on a fixed annuity can not be lower than the regulatory prescribed minimum interest rate.

In most cases, this will be calculated at or above 1% per year. This ensures that your money grows at a guaranteed rate of return for the entirety of the specified period. Fixed annuities are designed in many different varieties.

With a deferred fixed annuity, you accumulate money before retirement, also known as the accumulation phase, and receive payouts during retirement (the annuitization phase). With an immediate annuity, there is no accumulation phase.

Instead, you pay into the annuity as a lump sum and begin receiving payouts almost immediately (hence the name). One of the main benefits of annuities is the fact that they can offer guaranteed lifetime income.

Fixed annuity products may be a good fit as part of a comprehensive financial portfolio, either pre-or post-retirement. Because of their fixed interest rate and steady growth, they certainly fit easily into the safest and most conservative bucket of your financial plan.

How Do Fixed Annuities Work?

Fixed annuities or declared rate annuities are very simple. First, the owner (contract-holder) deposits money into the annuity. The fixed rate of return does not adjust for inflation and is not linked to any index. Instead, the money receives steady, guaranteed growth throughout the specific period designated in the annuity contract.

Then, the annuitant receives payouts based on the type of annuity and the annuity contract's specifications.

You can buy fixed annuities either through licensed agents or, in the case of Canvas Annuity, directly online at your convenience. The guarantee of the payouts is backed by the financial strength of the insurance company. For that reason, it is important to purchase an annuity from a reputable financial institution and compare all possible annuity plans. But how your fixed annuity will work really depends on the type of fixed annuity product you purchase.

There are two types of fixed annuities that determine how you pay into it and when you will receive payouts.

Types of Fixed Annuities

There are two primary types of fixed annuities: deferred annuities and immediate annuities.

Fixed Deferred Annuities

Fixed-rate deferred annuities are annuity contracts that offer you a guaranteed fixed rate of interest over a specified period that you select. This period is usually a number of years: one, three, five, or seven years. With a deferred annuity, you deposit a specific amount of money with the insurance company and they guarantee you a fixed rate of return on that money.

During the accumulation phase, the money grows tax-deferred, meaning it is not subject to taxes until the contract begins to payout.

When your rate guarantee period ends, that doesn’t mean your contract ends but it is when your minimum fixed interest rate comes into play. For example, if you purchase a 3-year fixed annuity, your contract will show the guaranteed rate of interest you will receive for those three years as well as the minimum interest rate your insurance company can credit you from the time your guarantee term ends until your contract matures (usually around the time you turn 100).

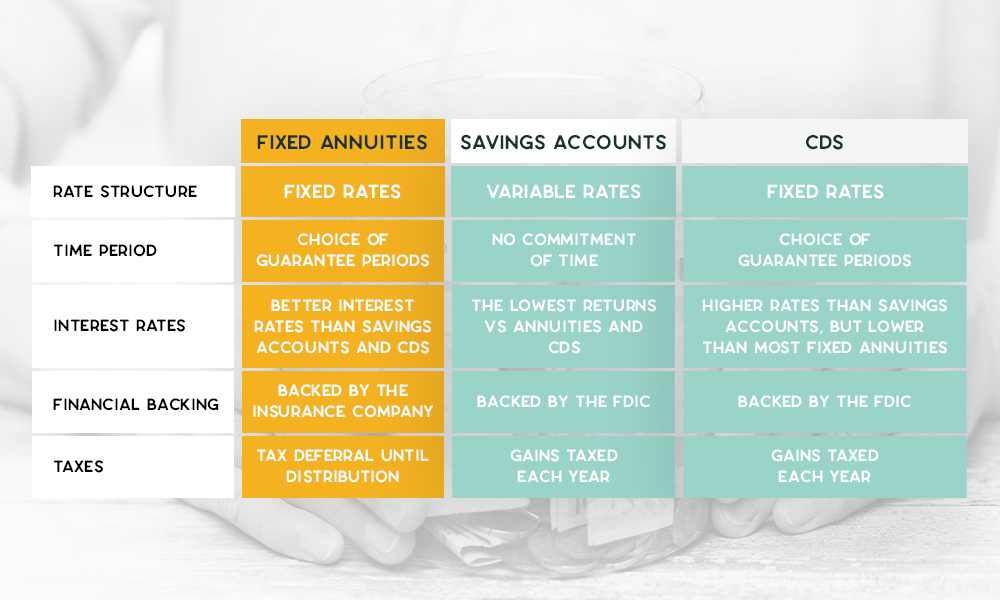

Your insurance company may credit you more than the minimum, but never less. Fixed deferred annuities are great if you’ve yet to retire, and you’re making a retirement plan. They help you accumulate tax-deferred money. Plus, interest rates are often superior to bank savings accounts and CDs (more discussion on that topic later).

Fixed Immediate Annuities (Income Annuities)

Fixed-rate immediate annuities differ from deferred annuities because your money is distributed immediately at a fixed rate determined by the insurer. You pay a lump sum (single premium) into the annuity, and immediately begin receiving payouts. These payouts are calculated based on the term you select.

For instance, if you choose a lifetime payout and live for another 30 years, the return will be calculated for that specific amount of time. It’s a little more straightforward for period certain annuity payouts because you are selecting the specific period of time that you’d like to receive payments (10 years, for instance).

Fixed-income annuities are great for those people who are entering retirement and who require a steady, guaranteed amount of money in retirement to supplement any social security income. No other product can provide this peace of mind.

Pros of a Fixed Annuity

First and foremost, fixed annuities are the easiest type of annuity to understand and buy. With a deferred annuity, you receive steady, tax-deferred earnings with a guaranteed minimum interest rate. As mentioned earlier, these annuities are generally a better alternative to lower-yielding savings products, like savings accounts and CDs.

This is not only because their crediting rates are usually much higher, but the earnings are not taxable until they are distributed. With other bank products, you pay income tax on earnings each year. This tax-deferral feature is important and unique to annuities. With a fixed immediate annuity, you still receive a fixed rate of return, but you receive payouts immediately. The insurer guarantees to pay out the annuity in the frequency and term that you select.

For instance, you may select to receive payments for the rest of your life. Or, you may decide that you want payouts for ten years. If you choose the second option and pass away during the specified ten-year period, your beneficiary would continue to receive your payments.

As a retiree, a fixed immediate annuity can provide you with a lot of peace of mind, knowing that you have a stream of income that can supplement your social security payments! Both immediate and deferred annuities can offer you this income stream.

Cons of a Fixed Annuity

While fixed annuities are the most conservative annuity type, their "safe" nature can lead to some issues.

First, like all annuities and even CDs, there are penalties for early withdrawal known as surrender charges. Surrender charges can eat into your returns, so when buying a deferred annuity, ensure that you’re using funds that you won't need for a while. Surrender charges generally run between five and ten years, depending on the product.

Because of the surrender charges, it's a good idea to not put too much of your retirement savings in any one bucket, including fixed annuities.

The key to a successful retirement plan is diversification, and a fixed annuity can play a part in this diverse mix of products.

Second, because you are locking in guaranteed rates of return, you may lose out on more robust gains that can come from other investment vehicles, like indexed annuities, variable annuities, mutual funds, stocks, or bonds. And with single-premium fixed immediate annuities, once you make the deposit, that money is no longer available to you, even if you have an emergency.

It will only be available via the payout schedule in the insurance contract. Because of this loss of liquidity, think deeply about how much of your retirement nest egg you should allocate to income annuities.

Fixed Annuities vs Indexed or Variable Annuities

In addition to fixed annuities, there are two other types of annuities: indexed annuities and variable annuities.

These annuities are generally much more complex than fixed annuities, but they can offer higher rates of return.

When choosing an annuity, it's important to understand the different types so you can make the right decision based on your finances.

Fixed Annuities

To review, fixed annuities offer steady, fixed-rate, and tax-deferred growth. Fixed annuities generally have better interest rates than traditional bank savings products.

Indexed Annuities

Indexed annuities (also known as fixed indexed annuities) can offer better returns than fixed annuities. This is because their return rate is based on equity indexes, like the S&P 500.

Most indexed annuities have a death benefit feature paid out to a beneficiary if the annuitant dies. Some even have features called riders. Riders are enhancements to the annuity that can provide great benefits, but also may come with costs.

An example of a rider may be that the annuitant receives enhanced or accelerated payments if they enter into a nursing home. Finally, most indexed annuities offer principal protection, meaning that you will never lose more than the initial deposit put into the annuity.

Variable Annuities

Variable annuities use mutual funds and stock investments to maximize possible returns. As such, you can trade and shift money around without generating a capital gains tax liability.

However, the IRS requires that you pay ordinary income tax on accumulated earnings when you take out funds. Variable annuities are generally a good fit for people who have already contributed the maximum to their tax-deferred retirement plans or IRAs.

If this is you, and you need a place to put additional after-tax money for tax-deferred growth, a variable annuity could be the right choice. Because of the complexity of variable annuities, we suggest seeking the advice of a financial advisor before purchasing.

These annuity products may also have a high fee structure, including investment "loads" and high commissions. There is also a high potential for loss as compared to fixed annuities and fixed-indexed annuities.

Annuities Vs Bank Savings Products

Banks provide an array of financial services, including savings products like savings accounts and certificates of deposit (CDs). While these products are safe and protected from loss by the FDIC, they generally offer lower rates than fixed annuities.

So if you are seeking higher interest rates backed by the security of the insurance company, annuities—even the most conservative and safe fixed versions—may provide a great alternative.

The Role of Fixed Annuities In Your Retirement Plan

As we mentioned earlier, a well-balanced retirement portfolio consists of both conservative and more risky investments, including, but not limited to stocks, bonds, CDs, mutual funds, and annuities. Fixed annuities are among the most simple pieces of the retirement planning puzzle.

They can help you accumulate money with very attractive interest rates. Then, when you are ready to create additional guaranteed monthly income, you can “annuitize” them, giving you a regular stream of monthly payments.

So, whether you are interested in growing your money safely prior to retirement, or distributing it to yourself in retirement to complement other retirement income, fixed annuities are perhaps the most simple type of annuity to purchase. At Canvas, our annuities are simple, straightforward, and people-first.

You can buy our annuities directly online, meaning you don't have to work with an agent. That means no commission, account, or annual fees. If you are looking for a very attractive guaranteed fixed annuity rates, and don’t need full access to your money for a few years, the Canvas Annuity may be a good fit. But we also offer penalty-free withdrawals for qualifying medical emergencies and partial withdrawals up to 10% of your account value.

Our annuities are flexible, helping you deal with life when it happens. Canvas annuities are backed by the Puritan Life Insurance Company of America, a company rated B++ by A.M. Best. Ready to get started? See which Canvas annuity is right for you, and we can help you get it up and running today.

Citations

Morningstar, A Primer on Annuities (Miller 2020) https://www.morningstar.com/articles/972416/a-primer-on-annuities

Resource Hub