Updated: October 10, 2025

What Is a 403(b) Plan?

Saving for Retirement with 403(b) Plan

While 401(k)s are one the most common retirement plans, they are not the only one. Where work, whether that’s in the private sector, a nonprofit, or public service, often determines what type of retirement account you can invest in. If you are a professional working in public schools, healthcare or certain non-profits, you may be offered a 403(b) plan. In this article we’ll explore what a 403(b) retirement plan is, how they work, and the benefits of 403(b) investments in your retirement strategy.

What is a 403(b) Plan?

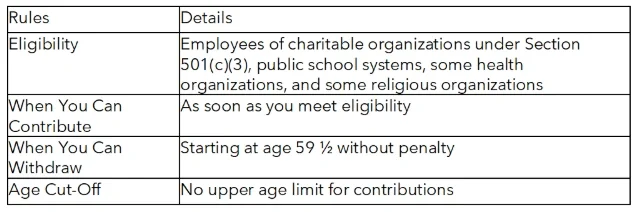

A 403(b) is a tax-advantaged retirement savings plan available to employees of public schools, healthcare, and some nonprofit organizations, and some churches. You can make contributions to a 403(b) from your paycheck, just like with a 401(k). Making contributions pre-tax is most common, but your organization may offer Roth 403(b) options as well to contribute post-tax.

The 403(b) plan was first introduced in 1958 as part of the Internal Revenue Code. 403(b) plans can also be referred to as a Tax-Sheltered Annuity (TSA). 403(b) plans compared to 401(k)s or 401(a)s have their own set of benefits and rules.

How Does a 403(b) Work?

Just like with other retirement plans, you get to decide how much of your paycheck to contribute to your 403(b) each pay period up to annual IRS limits. That money is then automatically invested into the options available through your plan, which may include mutual funds and annuities.

Once your money is in a 403(b), it starts growing through compounding. That means any returns you earn are reinvested and have the potential to earn even more over time. The longer your money stays invested, the more powerful that growth can become and can help you build a healthy retirement fund.

What Are the Current 403(b) Limits in 2025?

Each year, the IRS updates 403(b) contribution limits to keep up with inflation. For 2025, the limits are:

- Employee contribution limit: $23,500

Who is it for? This is the standard contribution limit for anyone with a 403(b).

- Catch-up contribution (age 50+): Additional $7,500

Who is it for? This is for people 50 and over with a 403(b). Catch-up contributions allow individuals to make higher contributions to help boost their 403(b) as they get closer to retirement age.

- Higher catch-up (age 60–63): Additional $11,250

Who is it for? This is for people ages 60 through 63 with a 403(b). High catch-up contributions are an upgrade from regular catch-up contributions and can only be taken advantage of for a limited time—so don’t miss out!

- 15-years of service catch-up: Additional $3,000 contribution per year with a $15,000 lifetime limit for qualifying plans

Who is it for? People who have 15 or more years of service at the same employer

What Types of 403(b)s Are There?

403(b) plans typically come in two plan options—a traditional 403(b) or a Roth 403(b). The main difference is when you will pay taxes on your contributions.

Traditional 403(b)

Traditional 403(b) contributions are made with pre-tax dollars. The benefit is you current income will have lower taxes, and those taxes will be delayed until you withdraw funds in retirement.

Roth 403(b)

Roth 403(b) contributions are made after taxes. The benefit is for the future so you can make qualified withdrawals from your plan in retirement that are tax-free.

What Are the Benefits of a 403(b)?

A 403(b) plan offers a variety of features that make it a strong option for long-term retirement savings. Here are some of this plan’s top benefits:

- Tax-deferred growth: You have the option for investments grow without being taxed each year. This means you can put more towards savings and you will only pay taxes when you begin taking distributions in retirement.

- Employer matching contributions: Some employers contribute to your 403(b) account based on how much you contribute yourself. This is free money that can significantly boost your retirement savings.

- Higher catch-up contributions: If you have worked for same employer for 15 years or more, you may qualify for extra catch-up contributions in addition to the standard IRS limits.

- Movability: If you switch jobs or retire, you may be able to roll your 403(b) into another qualified retirement plan or an IRA. This is important so you stay in control of your savings without penalties or unnecessary taxes.

What Are the Rules for a 403(b) Plan?

Your 403(b) plan can be a powerful retirement savings tool, but there are a few important rules to be aware of. Here’s a quick overview of what you should know to make the most of your plan.

Early withdrawals (before age 59½) usually face a 10% penalty and are taxed as ordinary income. Required Minimum Distributions (RMDs) apply at age 73 (or 75 depending on birth year) for traditional 403(b) accounts. Roth 403(b)s held by the original owner are RMD-exempt as of the SECURE 2.0 Act of 2024.

Your 403(b)’s Role in Retirement Planning

Consistent investment into retirement plans, like a 403(b), can help set you up for the retirement you want. But it’s just one part of your retirement puzzle. Pairing your 403(b) plan with other financial tools like annuities can help you build a dependable income stream. At Canvas Annuity, we can help pair your When all the pieces come together, you’ll feel more confident and in control of your financial future.

Resource Hub