Updated: October 9, 2025

What Is a 457 Plan?

Planning for Retirement with a 457(b)

Most Americans saving for retirement are familiar with a 401(k), but it’s not the only retirement plan out there. Depending on where you work, you may qualify for alternative retirement savings plans like a 457(b).

In this article, we’ll answer key questions on what a 457(b) plan is, the benefits of a 457(b) plan, and how it compares to other retirement options. Whether you're looking to boost your savings or just understand your benefits, this guide covers everything you need to know.

What is a 457(b) Plan?

A 457(b) is a tax-advantaged retirement savings plan offered to employees of state and local governments, as well as certain nonprofit organizations. It allows eligible workers to contribute a portion of their salary into a retirement account, where it grows with compounding interest, until withdrawn.

The 457(b) plan was first created under Section 457(b) of the Internal Revenue Code in 1978. 457(b) investments tend to be limited to annuities and mutual funds compared the wider variety of investment options you may get with a 401(k) plan.

How Does a 457(b) Work?

Just like with a 401(k) or a 403(b), you make elections on how much of your paycheck to contribute to your 457(b) plan, up to IRS limits. 457(b) plans are available in both traditional and Roth options.

Is a 457(b) taxed?

Yes, just like with any other retirement plan the money you invest will be taxed. However, the plan type you choose can affect when you are taxed. With a traditional 457(b) you invest money pre-tax and can delay tax obligations until you withdraw funds later on. Roth 457(b) contributions, if available with your employer, are made after-tax and allow for tax-free withdrawals in retirement.

What Are the Current 457(b) Limits in 2025?

Each year, the IRS adjusts contribution limits to reflect inflation. For 2025, the contribution limits for 457(b) plans are:

- Employee contribution limit: $23,500 or up to 100% of you salary if it is below the annual contribution limit

Who is it for? This is the standard contribution limit for anyone with a 457(b).

- Catch-up contribution (age 50+): Additional $7,500

Who is it for? This is for people 50 and over with a 457(b). Catch-up contributions allow individuals to make higher contributions to help boost their 457(b) as they get closer to retirement age.

- Higher catch-up (age 60-63): Additional $11,250

Who is it for? This is for people ages 60 through 63 with a 401(k). High catch-up contributions are an upgrade from regular catch-up contributions and can only be taken advantage of for a limited time—so don’t miss out!

- Special catch-up for final 3 years before retirement (specified in plan): Up to double the standard annual contribution limit if you qualify

Who is it for? For all 457(b) plan holders who qualify

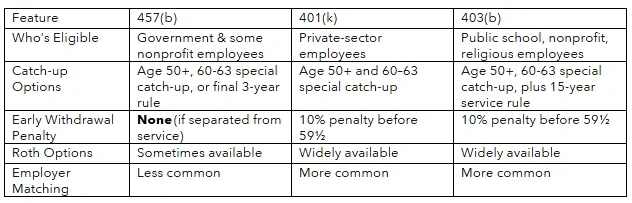

How Do a 457(b), 401(k), and 403(b) Plan Compare?

Wonder how your retirement plan options compare? Here’s a quick side-by-side look at how 457(b), 401(k), and 403(b) plans match-up on key features and benefits.

What Are the Benefits of a 457(b)?

457(b) retirement plans offer several unique advantages that make them a strong option for eligible employees, especially those working in government or nonprofit roles:

- No early withdrawal penalty: One of the most unique features of a 457(b) plan is the ability to withdraw funds penalty-free if you leave your job, even before age 59½.

- Tax-deferred growth: Your contributions can reduce your taxable income in the year they’re made. With a traditional 457(b) money grows tax-deferred until you begin taking distributions in retirement.

- Catch-up contributions: If you’re within three years of retirement age, you may qualify for a special catch-up rule that lets you contribute up to double the annual limit which can be a real lifeline to boosting savings later in your career.

- Movability: In some cases, you can roll your 457(b) funds into another qualified retirement plan like an IRA, 403(b), or 401(k).

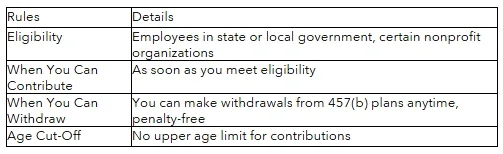

What Are the Rules for a 457(b) Plan?

Understanding the basic rules of a 457(b) plan can help you make the most of your retirement benefits. Here’s a quick overview on what you need to know:

Be aware that after you reach age 73 (or 75, depending on your birth year), Required Minimum Distributions (RMDs) kick in. That means you’ll need to start withdrawing a minimum amount each year from your 457(b), even if you don’t need the funds yet.

Your 457(b) Plan’s Role in Retirement Planning

A 457(b) retirement plan can provide unique savings options as you plan for retirement. With tax advantages, generous catch-up contributions, and no early withdrawal penalties after job separation, it offers features that help you save with fewer roadblocks.

Combining your retirement account with other financial tools like IRAs, HSAs, or annuities can get you well on the road to the retirement you deserve. When you need help choosing the right investments for your future, Canvas Annuity can help with annuity options that can work along your 457(b) plan. Get the conversation started with our team to today to see what we can do for you.

Resource Hub