Updated: November 7, 2025

What Is the Difference Between a Simple IRA vs. Traditional IRA?

Do You Need an IRA to Retire?

Individual Retirement Accounts (IRAs) are one of the most common ways to save for retirement, either in addition to a workplace 401(k) or as a primary retirement investment account. There are different types of IRAs you can choose from, but two of the most common are the SIMPLE IRA and the Traditional IRA. While they may sound similar, each IRA comes with their own set of rules and unique benefits.

In this article, we’ll explore the key differences between a SIMPLE IRA and a Traditional IRA, how each works, and how to decide which might be a safe place to put your retirement money.

What Is a Simple IRA?

A SIMPLE IRA (Savings Incentive Match Plan for Employees) is a retirement savings plan geared towards small businesses with 100 or fewer employees. Both employers and employees can make contributions to a SIMPLE IRA and its works like a simplified 401(k).

How Does a Simple IRA Work?

A SIMPLE IRA is funded with pre-tax contributions, meaning the money you put in lowers your taxable income for the year. Again, both the employee and employer can contribute—employers are required to either match up to 3% of their employee’s pay or make a flat 2% contribution for all eligible employees.

The money you add to a SIMPLE IRA is automatically invested, so your savings will grow tax-deferred until you start taking withdrawals in retirement.

What Are the Rules for a Simple IRA Plan?

A SIMPLE IRA lessens the burden for small businesses to provide retirement accounts for their employees, but plan does come with its own set of rules:

- Employees must earn at least $5,000 in compensation to join (earned in the 2 preceding years to the current year).

- Employers must make either matching or non-elective contributions each year.

- The 2025 contribution limit for companies with 26 to 100 employees is $16,500, with an additional $3,500 catch-up for employees 50 and older.

- The 2025 contribution limit for companies with 25 or less employees is $17,600, with an additional $3,850 catch-up for employees 50 and older.

- Withdrawals before age 59½ are generally subject to income taxes and penalties.

- RMDs (Required Minimum Distributions) begin at age 73 (or 75, depending on your birth year).

- You’re always 100% vested, meaning all contributions belong to you right away.

Why Should I Get a Simple IRA?

A SIMPLE IRA is a great option if you work for a small business that offers it or if you are self-employed and looking for a tax-advantaged retirement plan. It provides the benefit of employer contributions when you workplace does not have the resources to support a full 401(k) plan.

Simple IRA Pros and Cons

Pros:

- Employer contributions are guaranteed

- Sometimes higher contribution limits than a Traditional IRA

- Simple to set up and manage

Cons:

- Lower limits than a 401(k)

- Early withdrawals (within two years) face a 25% penalty

- No Roth (after-tax) option available

What Is a Traditional IRA?

A Traditional IRA is an individual retirement account that you open and manage on your own, not through your employer. It is designed to help you save for retirement, take advantage of potential tax deductions, and provides flexible investment options.

How Does a Traditional IRA Work?

With a traditional you contribute your own money, up to annual IRS limits, and your investments grow tax-deferred until retirement. Typically, IRAs can hold investments for assets like mutual funds, ETFs, stocks, and bonds, which you can customize for control over your portfolio.

Your contributions may be tax-deductible, depending on your income level and whether you have access to another retirement plan through work

What Are the Rules for a Traditional IRA Plan?

Just like with a SIMPLE IRA, Traditional IRAs have their own rules. Here’s what you should know:

- Anyone with earned income can contribute and there is no age limit.

- The contribution limit for 2025 is $7,000, with an additional $1,000 catch-up for those age 50 or older.

- Tax deductibility depends on income and participation in other workplace plans.

- RMDs (Required Minimum Distributions) begin at age 73 (or 75, depending on your birth year).

Why Should I Get a Traditional IRA?

A Traditional IRA is a good fit for anyone who wants to save for retirement on their own, especially if they don’t have access to a 401(k) or SIMPLE IRA. Contributions grow tax-free to maximize interest earned and stashing money into a Traditional IRA can help lower your taxable income.

Traditional IRA Pros and Cons

Pros:

- Tax-deductible contributions

- Flexible investment options

- Available to anyone with earned income

Cons:

- No employer match

- Lower contribution limits than a SIMPLE IRA or 401(k)

- Withdrawals before 59½ face a 10% penalty

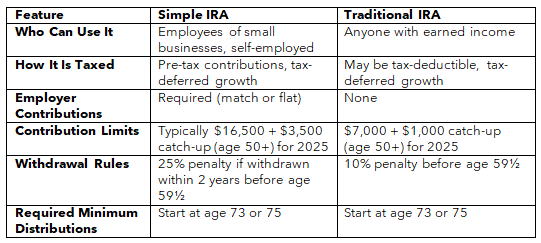

How Does a Simple IRA vs. a Traditional IRA Compare?

If you’re deciding between a SIMPLE IRA and a Traditional IRA, it helps to see how they stack up side by side. Use our comparison chart to help you decide with plan fits best with your retirement goals:

Including IRAs in Your Retirement Financial Portfolio

Both SIMPLE and Traditional IRAs can play an important role in how you save for retirement. They offer valuable tax advantages and flexibility for a wide range of savers—whether you're working for a small business or managing your savings independently.

To build a well-rounded retirement strategy, think about how your IRA can pair with other income sources like Social Security, a 401(k), or even an annuity. At Canvas, we offer annuities that work alongside your retirement accounts to provide guaranteed income you can count on. Learn more about other smart saving strategies like how to rollover a 401(k) to an annuity, and explore how we can help you make the right financial moves as you prepare for retirement.

Resource Hub