Updated: March 7, 2024

What is the Cash Surrender Value of an Annuity? Is It the Same as Cash Value?

The Cash Surrender Value (CSV) of an annuity is the amount of money that you would receive if you surrender or cancel your annuity before the end of the surrender period.

It represents the amount of cash that you could access after the annuity issuer applies surrender charges and other fees, if any. So the CSV is not the same as the cash value.

The concept of cash value is usually associated with permanent (vs. term) life insurance policies. Life insurance cash value is the savings component of a whole life or universal life policy. Part of the premium payment of these policies goes into a savings or investment account that accumulates over time, and this portion is known as the cash value. You can usually access this cash value through withdrawals, loans, or by surrendering the policy.

When referring to annuities, cash value refers to the undiluted current value of the account.

Annuities are long term retirement products offered by insurance companies designed to help you accumulate money prior to retirement, then create a flow of money in retirement that you cannot outlive.

But accessing money from your account before retirement can be punitive, so it's important to understand some key terms and conditions. Let's dig in.

Cash Value vs. Cash Surrender Value

Cash value and cash surrender value have different definitions.

When determining how much cash you will ultimately receive, you must consider any fees your company will charge for removing money from your account.

To make this calculation, you must subtract the fees and possible withdrawal charges from the account value. Let's take a look at some definitions for clarity.

Cash Value

Cash value, also known as "account value" when discussing annuities, is the total accumulated current value of your annuity contract.

It represents the value of your account before any withdrawals are contemplated and any charges are applied.

Cash Surrender Value

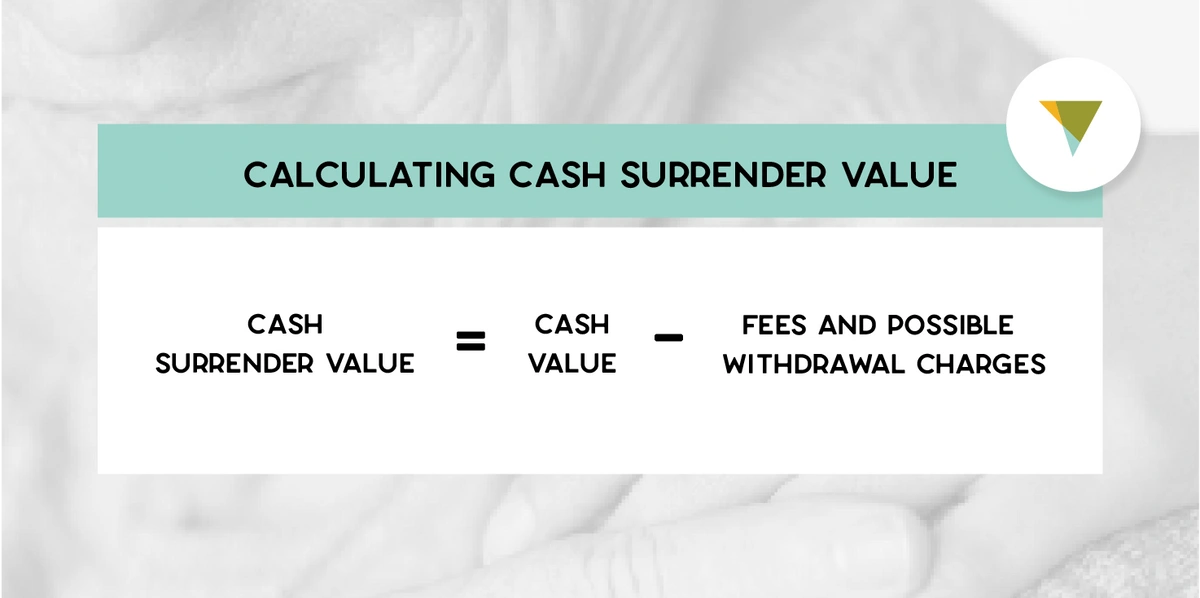

An annuity's cash surrender value is the ultimate amount of money you will receive if you choose to surrender all or part of your annuity contract.

It is the net money proceeds after the insurance company reduces the amount by applying items like surrender charges or outstanding loan balances.

Surrender charges are applied during the surrender period, which usually lasts from five to 10 years and ranges from 10% of your annuity cash value in the earlier years of the contract to 0% toward the end of the surrender period.

How Cash Surrender Value Works in Annuities

The cash surrender value is the net amount of money you receive after applicable surrender charges and/or loan balances are applied to the annuity.

Annuity surrender charges are fees imposed by the insurance company if you decide to surrender or terminate your annuity contract before it reaches the end of the surrender charge period, or before the end of your contract term.

Since annuities are long term contracts and insurers need to make a profit, surrender charges are designed to discourage early withdrawals so the insurer recoups some of the costs incurred in setting up and administering the contract.

The cash surrender value will change over time because surrender charge percentages decrease as you move through the surrender charge period.

The Role of Surrender Charges in Cash Surrender Value

Surrender charges can be a bit complex, but there are a few terms and concepts to keep in mind that can add clarity:

- Graduated Scale: Surrender charges are usually applied on a graduated scale, which means the percent charged decreases over time. Surrender charges usually decline annually over a period of time indicated in your contract, such as 5, 7 or 10 years.

- Percentage of Withdrawal Amount: Surrender charges are calculated as a percentage of the withdrawal amount. For instance, if the surrender charge is 5%, and you withdraw $10,000 before the surrender period ends, you will be subject to a $500 surrender charge, which makes your net withdrawal $9,500.

- Exceptions: Many annuities (like those from Canvas Annuity) allow for penalty-free withdrawals up to a certain percentage of the account value each year. This is typically known as the "free withdrawal" amount, which allows a small percentage, such as 5% or 10% of the account value, to be withdrawn free of surrender charges. However, you may have to pay income taxes on these amounts.

- End of Contract Term: After the surrender period ends, you can typically withdraw funds without incurring any surrender charges. Be careful, though, because many annuity providers provide a "window of time" within which you need to make a decision. If no decision is made, your money may end up in a new contract with new surrender charges. Most annuity companies give you plenty of notice regarding the upcoming window.

Surrender charges can have a major impact on your surrender value. These charges will impact the amount you will receive if you decide to surrender your annuity before the end of your term. The CSV is calculated by subtracting any applicable surrender charges and fees from the account value.

During the surrender period, the surrender charges can significantly impact the cash surrender value, reducing the amount the annuity holder will receive if they choose to withdraw their funds.

For example, if the annuity has a 10% surrender charge, and the account value is $100,000, the cash surrender value after one year of ownership would be $90,000 if the annuity holder decided to surrender the annuity. As the surrender period progresses, the surrender charges decrease, so the impact on the cash surrender value lessens over time.

You can avoid surrender charges if you carefully plan your withdrawals based on the free withdrawal provisions of your contract. Many people use this free withdrawal provision for items like property taxes, vacations or other expenses.

Tax Implications of Cashing in the Surrender Value

In addition to surrender charges, making early withdrawals (prior to age 59 1/2) from your annuity could lead to a 10% federal tax penalty from the Internal Revenue Service (IRS). This rule applies to annuities that are considered "qualified" meaning funded with pre-tax dollars.

This is similar to rules that apply to early distributions from your 401(k) or individual retirement account (IRA). Because the IRS considers an annuity a retirement product, they have implemented additional tax penalties on early withdrawals to discourage people from using annuities for short-term tax advantages.

In addition to the 10% early withdrawal penalty, withdrawals from any type of annuity (qualified and non qualified) are subject to ordinary income tax treatment.

Annuity payments are taxed as regular income (not capital gains) in the year that they are received. Canvas has assembled a comprehensive guide to annuity taxation that provides more detailed information regarding the impact of taxation on early annuity withdrawals.

Final Thoughts

You have worked hard to fund financial vehicles that can help you enjoy a comfortable retirement. That's why understanding annuity cash value and withdrawal rules is critical.

If you are ever confused by the rules or need clarification regarding your options, it is a good idea to contact your financial representative or the customer service area of your annuity company to ensure peace of mind. It's always better to know the rules before you take any action, especially regarding withdrawals.

Canvas annuities are fixed annuity products that you can buy directly or with the help of a licensed contact center professional. This makes it easy to get great rates (some of the most competitive in the country) and avoid having to meet face to face with an agent.

Resource Hub