Updated: March 14, 2025

Coordinating Social Security Benefits with Annuities

Should I Combine Annuities with Social Security?

For most retirees, Social Security provides a foundation of income, but it’s rarely enough to cover all expenses. As of January 2025, the average monthly benefit retired workers claim from Social Security is $1,976 according to the Social Security Administration (SSA). For many retirees this could be lower, since higher income workers can drive this figure up. Do you think Social Security alone is enough to cover your expenses in retirement? Adding annuities to your retirement income strategy can help fill that gap, offering guaranteed income for life.

So how can Social Security and the right annuity strategy help fund your retirement? In this article, we’ll explore how annuities work as growth and income tools, so you can set up a retirement plan that makes sense for your life.

Social Security Alone vs. Combining with an Annuity

How Social Security Works

Social Security and annuities both provide a steady income stream, but they work in different ways. Social Security is a government program funded by payroll taxes from workers and employers. To qualify for benefits, you need at least 10 years of covered earnings.

If you qualify, the Social Security Administration then calculates what your benefit will be based on your highest 35 years of earnings, adjusted for wage growth. You can claim these benefits when you reach retirement age or delay. Your benefit claim with then earn retirement credits for higher monthly payments when you eventually do choose to collect benefits (retirement credits cap at age 70). Once claimed, Social Security benefits are paid for life and adjusted annually for inflation to help protect against rising costs.

How Annuities Work

Annuities, on the other hand, are privately purchased insurance products. You pay a one-time premium (or multiple payments) in exchange for monthly income for the rest of your life. The amount you receive depends on factors like interest rates at the time of purchase and your life expectancy. Unlike Social Security, annuities aren’t tied to your work history but can work together with Social Security to providing additional guaranteed income for life. Together, they can form a strong foundation for a reliable retirement income strategy.

How Social Security and Annuities Can Work Together

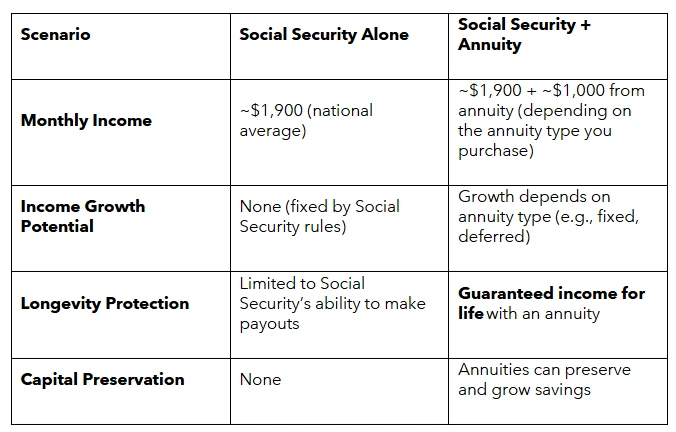

What does it look like to retire with Social Security alone compared to combing Social Security earnings with financial tools like annuities? Take a look at our comparison chart:

Are Annuities a Smart Addition to Your Retirement Income Plan?

Annuities are a versatile and dependable way to earn guaranteed income for life. Whether you’re looking for immediate payouts, long-term growth, or a balance of safety and market potential, annuities offer options tailored to your financial needs. Below is a breakdown of the some common types of annuities, how they work, and who they are best suited for.

Fixed Annuities

Fixed annuities provide a guaranteed interest rate for a specific period (usually three, five, or seven years), ensuring steady growth with a guaranteed rate of return. Fixed annuities also grow tax-deferred for the best growth outcome.

- Best for: Retirees who are risk-averse and want reliable, stable income without market exposure.

Immediate Annuities

Immediate annuities (also called income annuities) convert a lump sum payment into guaranteed income that begins almost immediately. This income can last for a specific period or for the rest of your life, depending on your contract.

- Best for: Retirees who need income right away to cover living expenses or supplement Social Security.

Fixed Indexed Annuities

Fixed indexed annuities are tied to the performance of a stock market index, such as the S&P 500. They offer the potential for higher returns than fixed annuities, along with a guaranteed minimum return so you at least keep the value of your starting deposit.

- Best for: Retirees who want moderate growth potential with some exposure to market performance and are more comfortable with risk.

Combining Annuities and Social Security in Your Retirement Strategy

Now you know there are a variety of annuity types you can choose to combine with Social Security as part of a balanced retirement income strategy. Wondering how much you need in addition to Social Security for your retirement? Follow this step-by-step guide to see how annuities can supplement your income:

Step 1: Assess Your Expenses

List your essential expenses, such as housing, healthcare, and daily living costs. Determine how much of these are covered by Social Security. Having an estimate of your budget by month can help you figure out where you have gaps in retirement funds and how long what you currently have saved will last.

Step 2: Evaluate Your Risk Tolerance

- If you prefer stable, guaranteed income, consider fixed annuities.

- Tip: Considering Canvas Annuity products? You can use our annuity calculator to learn how much your annuity could be worth in a personalized report.

- If you’re comfortable with some risk for higher returns, explore indexed or variable annuities.

Step 3: Match Annuities to Your Timeline

- Need immediate income and are with lower payouts? → Choose an immediate annuity.

· Have time to grow your savings? → A deferred annuity may be better.

Step 4: Consult a Financial Advisor

Get in touch with a financial expert you trust to help you choose the best annuities for guaranteed income based on your specific goals for retirement.

Start Your Annuity Journey with Canvas

Combining Social Security with annuities can transform your retirement income strategy, locking in guaranteed income for life while preserving and growing your savings. Whether you’re comparing pensions vs. annuities or weighing an annuity vs. fixed income investments, the right choice depends on your needs and goals.

Take control of your retirement today with Canvas Annuity. Request a free retirement guide or contact our team to learn more about how our Flex Fund or Future Fund annuities could fit into your retirement plan.

Resource Hub