Updated: June 13, 2024

How Does a 1035 Exchange Work for Annuities and Life Insurance?

A 1035 exchange allows you, as a contract owner, to transfer funds from an existing life insurance, endowment, or annuity contract to a new policy, without owing taxes on the amount transferred.

If you have an annuity that’s nearing the end of its guarantee term, if you are seeking better rates or terms, or if you have concerns about the financial solvency of your insurer, we hope the information presented here is helpful. Use this information as a guide of what to consider before beginning a 1035 exchange.

This article covers what a 1035 exchange is, how it works, and some items to consider before exchanging your annuity for a new annuity contract.

What Is a Section 1035 Exchange?

A 1035 exchange is a way to exchange an existing annuity policy for a new contract. The new product may either help you meet a different goal or provide a better rate of return.

With a 1035 exchange, you get to transfer your funds to a new policy without paying taxes on the funds. This section of the IRS tax code essentially acknowledges that you're not taking a distribution of money.

Instead, you're simply transferring funds from one product to another, all while maintaining the funds' tax-deferred status and the original cost basis. This is similar to IRA to IRA rollovers. “Direct” transfers are always better than receiving the money then making the transfer, at least from the perspective of the IRS.

Understanding this tax-free exchange process is the best place to start for non-qualified annuity owners unhappy with their current company, contract, or rate.

How a 1035 Exchange Works

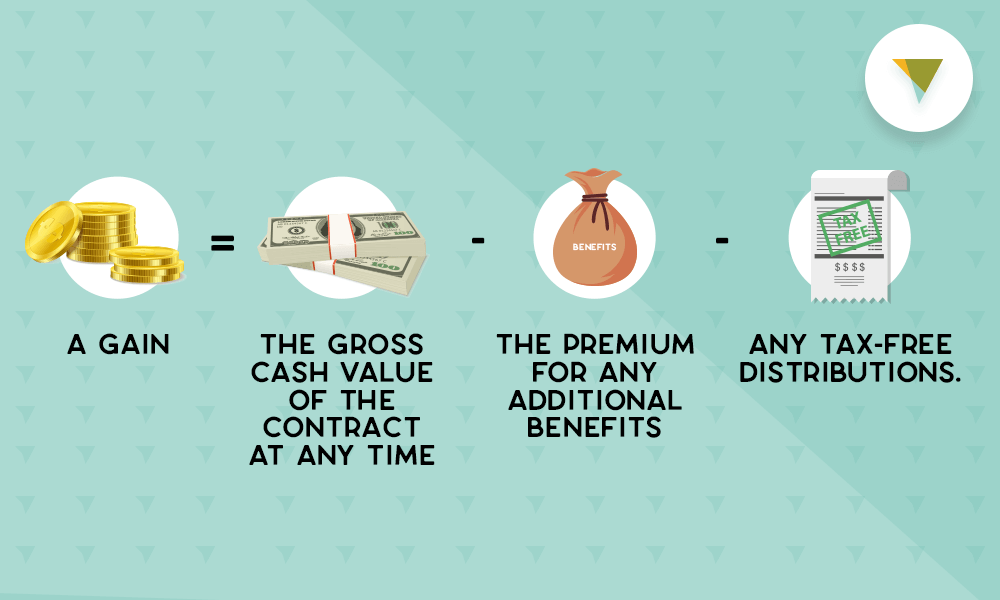

To understand how the 1035 exchange works, we must first understand what gains are. A gain is the difference between the gross cash value of the contract at any time and its premium tax basis (the amount placed in the contract) minus the premium for any additional benefits and minus any tax-free distributions.

With an annuity, your gains are tax-deferred. Meaning, unlike savings accounts or CDs, you don't have to pay taxes on them in the year you earn them. Instead, you only pay taxes on gains in the year you receive them.

Section 1035 of the Internal Revenue Code allows you to continue deferring taxes on any gains. But only as long as all the proceeds from the original policy transfer into the new policy. Also, there can't be any outstanding loans on the policy at the time of the exchange.

Which Policies Qualify For a 1035 Exchange?

Only non-qualified funds (i.e., the money you’ve already paid taxes on) can qualify for a 1035 exchange. If the funds are qualified, then the annuity exchange is governed by the IRA’s plan rules (the rules of whatever qualified plan holds the annuity).

Not all annuity contracts can be exchanged, but most annuities do allow for full or partial exchanges. All annuities that have some liquidity or have a surrender schedule—including fixed, indexed, and variable annuities—can be exchanged.

The annuities that cannot be exchanged are known as "irrevocable annuities." These types of products do not qualify for 1035 exchanges. Irrevocable annuities include income annuities like longevity and immediate annuities.

1035 exchanges can also involve life insurance policies. You can exchange a life insurance policy for an annuity under the 1035 exchange rules. But the reverse is not true; you cannot exchange an annuity contract for a life insurance policy.

Suppose you surrender your annuity without a 1035 exchange. In that case, you will owe ordinary income tax (not capital gains tax) on the earnings from the original annuity contract. But even if there are no gains in the original contract, you still may want to take advantage of the other tax benefits of a 1035 exchange. These benefits are not available if you simply surrender the annuity contract.

Reasons to Do a 1035 Exchange

There are various reasons why you may want to exchange an existing policy for a new one. For example:

- You find that you can get a comparable policy at a lower cost.

- You have concerns with the solvency of the insurance company that issued the original policy.

- You have concerns with the service of the agent who sold you the policy.

- A new life insurance or annuity policy may have more desirable features or benefits.

Reasons Not to Do a 1035 Exchange

There are also key reasons why replacing an existing insurance or annuity policy may not be a good idea. For example:

- The new company can apply first-year expenses to the new life insurance policy. This can reduce the cash value of your policy.

- Whole life insurance or annuity policies may include early surrender charges, reducing the cash value available to exchange for the new policy.

- The new policy will likely have its own new surrender charge schedule, which may extend beyond the original policy’s schedule.

- You may pay higher premiums if, for example, your health has declined since the purchase of the current policy (this only applies to a life exchange).

- The new policy typically will have a new contestability period—a two-year period from the issuance of the new policy. During this period, the insurance company can challenge a death claim based on the application’s misstatement (this also only applies to a life policy).

- There may be unfavorable tax consequences caused by surrendering an existing policy, such as a potential tax on outstanding policy loans.

What to Consider Before Doing an Exchange

When deciding if a 1035 exchange makes sense, consider why you purchased the annuity in the first place. Then, ask yourself why you believe it is no longer meeting your goals.

If you are considering exchanging an annuity, revisit your reasons for purchasing the existing annuity contract, including features like guaranteed growth, the ability to pass it along after you die, tax deferral, and growth upside. Then, compare that original goal to your current objective. This comparison can help to determine if your annuity is still meeting your needs or if you should consider a new option.

Here are several factors to keep in mind before you make your decision to exchange an annuity:

1. Make Sure You’re Getting a Better Deal

If your annuity provides a guaranteed interest rate, you’ll want to confirm the new rate with the new insurer. Ask under what circumstances it could change in the future.

You want to do this to ensure that you're getting a better deal by exchanging for a new annuity. Regulations require that you get a better deal when you do a 1035 exchange. Plus, it’s in your financial interest.

2. Understand Your Surrender Schedule

Most fixed annuities have a surrender charge schedule. If you exchange an annuity while it’s still in the surrender charge period, you’ll have to pay the penalty.

You must prove to the new insurer that you can receive a better interest rate or a higher income rate even after paying surrender charge. That is part of the required suitability review.

3. Know When You Can Do the 1035 Exchange Without a Penalty

If your annuity is outside its surrender charge period, you should be able to do an exchange without a penalty. Some MYGAs have built in 30-day windows in the middle of the surrender charge period that allow you to surrender or exchange your contract without a penalty. If your product has a window, it's important to be aware of when it starts so you are ready to act at the start of the window.

Because paperwork must go between the new insurer and the old insurer, in some cases via regular mail, the 1035 exchange process may take anywhere from 1-5 weeks.

4. Keep Your Important Policy Details Handy

If you decide to begin the 1035 exchange process, you’ll need to provide the new insurer with the details of your existing annuity. That way, they’ll be able to determine if an exchange is suitable given your situation. They’ll also be able to request funds from your current insurance company. Minimally, they require:

- The insurer name

- Product type (fixed annuity, variable annuity, fixed indexed annuity)

- Contract/policy number

- Reason for exchange

- Any surrender charge you will incur as a result of the exchange

You can find the majority of the information in your policy documents. Look for a page that’s titled “Contract Summary” or “Contract Details.” You can also typically find the required information on your policy's annual statement.

5. Choose an Insurer You’re Happy With

When you exchange an annuity, you are not required to stay with the same insurance company. Similarly, you don’t have to work with the same insurance agent when doing a 1035 exchange. A 1035 exchange is a great way to start over and build a new relationship with another agent or agency.

6. Understand the Primary Goal of the New Plan

No matter the type of annuity you have, you can exchange it for any other type. It’s best to start by defining your goals and then finding a product that gets you closest to achieving these goals.

- Consider exchanging your existing contract for an immediate annuity if you want guaranteed income that starts today.

- If you want guaranteed growth, consider exchanging for a fixed annuity.

- If you want the potential for market upside, consider exchanging for a fixed indexed annuity or variable annuity.

1035 Exchange FAQ

The following are some of the most commonly asked questions about 1035 exchanges. If you have any additional questions, be sure to speak with a tax professional or financial advisor.

When is Surrendering a Policy Better than Doing a 1035 Exchange?

There are a few cases where surrendering your policy vs. using a 1035 exchange may be advantageous. If your existing policy has no earnings or if you have outstanding loans, a 1035 exchange would likely not offer an advantage over a surrender.

Also, if you are in a hurry to make the change, a 1035 exchange generally involves much more effort to deploy than a policy surrender. The timing of the exchange can be uncertain because you are dependent on two insurance companies communicating with each other, which means the process can often take several weeks.

Finally, annuities are meant to be long term contracts. You should only consider a 1035 exchange if you are in a position to keep your money in the new annuity for the duration of the new surrender charge period.

What are "Like-Kind" Exchanges that Qualify for 1035 Exchanges?

Since 1035 exchanges can happen “product-to-product,” it is essential to know what product combinations are allowed for so-called “like-kind” exchanges:

- Life insurance for life insurance

- Life insurance for endowment

- Life insurance for non-qualified annuity

- Endowment for endowment, with a maturity not later than the original endowment

- Endowment for non-qualified annuity

- Non-qualified annuity for non-qualified annuity

Can Multiple Contracts be Used for a 1035 Exchange?

You may exchange multiple existing contracts for one new contract. However, you may not exchange one existing contract for multiple new contracts.

Can the Owner be Changed During a Tax-Free 1035 Exchange?

A penalty-free ownership change is not allowed in a 1035 exchange. If an ownership change occurs, depending on the specifics, you may incur income tax and gift tax consequences.

If you wish to make a change in ownership for the new policy, you should first change the ownership of the existing policy before initiating the exchange. Consult a tax advisor before making an ownership change.

Bottom Line: Who Is a Section 1035 Exchange Right for?

The bottom line with life insurance 1035 exchanges? Make sure you understand the advantages and disadvantages of exchanging or replacing your existing policy before switching to the new policy. You should also ask:

- What is the total cost to me of this exchange?

- What are the new features being offered?

- Why do I need these new features?

- Are these new features worth the cost?

- Can the existing policy be modified or supplemented to provide some or all of these same features?

- Will the agent involved in the new sale receive a commission for the exchange, and if so, how much is it?

- Will I need access to my money before the end of the new surrender charge period?

Don’t sign anything until you study all your options carefully. Also, make sure you have answers to all of your questions, and ensure that the new policy is a better fit for you than your current policy.

If you have any questions, speak with a financial professional. They can help you with your specific personal finance goals.

If you are considering moving money from an existing annuity to achieve a greater return, Canvas Annuities may be able to help. With guaranteed, fixed rates as high as 6.55% and the ability to speak with a helpful non-commissioned agent, we can help facilitate a 1035 exchange quickly, easily, and 100% online.

Resource Hub