Updated: March 7, 2024

Annuities vs. Dividend Stocks for Retirement: The Pros and Cons

Fixed annuities are very low risk. They can provide guaranteed growth plus guaranteed retirement income for the rest of your life. Dividend-paying stocks can also provide a regular income in retirement, but without a guarantee. They are riskier but can potentially offer higher earnings.

Annuities and stocks have different risk profiles and provide very different advantages. Both could be appropriate for your portfolio, but they fulfill different functions. Fixed annuities are a fantastic way to build out the more conservative side of your portfolio. Dividend-paying stocks can be a good choice for the more moderate and high-risk side. Fixed annuities provide stability and certainty, whereas stocks can be volitile with a potential for large earnings.

This article compares and contrasts these two different products. We will explain how you can determine the right one for you. You may find that the best option is a combination of both.

The Advantages of Annuities Over Stocks

An annuity contract is an insurance product that you buy from a life insurance company. Although an annuity can help you grow your money, it’s not exactly an investment. Instead, it is more like a private pension. You pay the annuity company a premium. Then your money grows over time (depending on the type of annuity). Later, you can choose to annuitize your contract. When you do, you convert your annuity into a steady, guaranteed income stream.

There are many different types of annuities and different options or riders (add-ons) you can choose. These customization options can make each annuity different from the next. For example, you might pay your annuity premiums with a single lump sum, or you might pay over a period of time. You can choose an immediate annuity that starts to pay you back right away or a deferred annuity that has time to grow before you get payments.

While annuities can vary in the details, they are generally designed to give you a guaranteed income in retirement. They provide financial certainty that other products can’t give you. Some of their main advantages include:

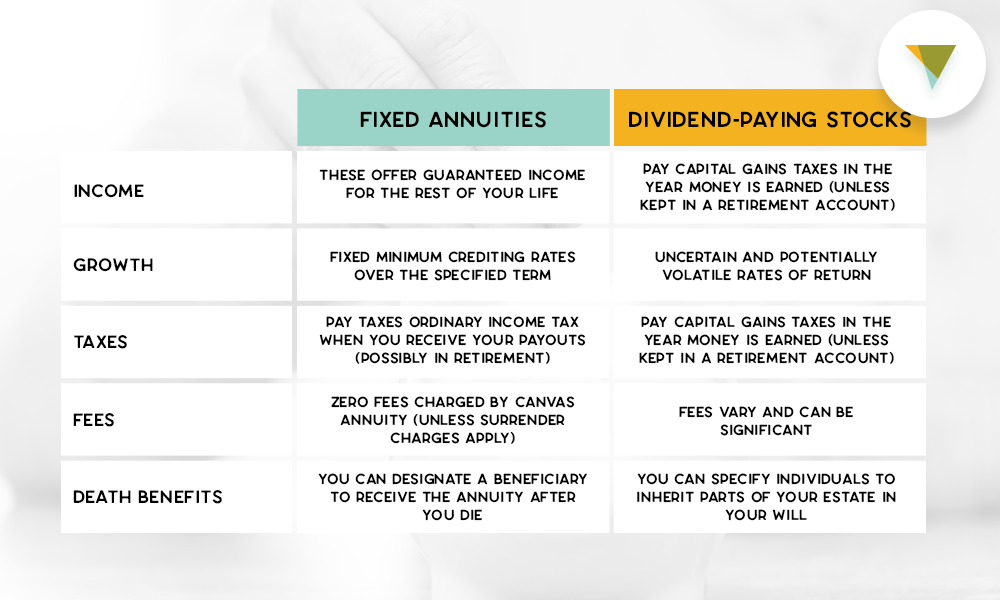

Guaranteed income for life. This is the biggest reason to buy an annuity. Most offer a lifetime payout option that will give you a lifetime income — a steady stream of cash for the rest of your life. This is not available with traditional investments like stocks. While you may earn income with dividend-paying stocks, that income is absolutely not guaranteed.

Guaranteed growth. Fixed annuities will grow by a fixed minimum crediting rate over the term of the annuity. Some will offer quite high rates of return for being such a low-risk product. Stocks are typically more volatile and cannot offer guaranteed rates of return. Note that not all annuities offer this guaranteed growth: Variable annuities and fixed-index annuities are two types of annuities that may not grow. Only fixed annuities offer guaranteed growth (as long as you keep your funds in the annuity for the length of the term).

Tax deferral. With stocks, you normally have to pay income tax on your capital gains earnings every year (unless they’re held in a tax-advantaged account like an IRA). When your annuity earns money, you won’t owe taxes until you take distributions in the future. Read about the tax advantages of annuities here.

Fixed annuities have low fees. The fees you pay with an annuity can vary greatly, and they’re typically larger for variable annuities. Fixed annuities from Canvas Annuity have zero account charges or fees (provided you don’t make early withdrawals). In contrast, brokerage firms can charge quite hefty fees for trading stocks.

Death benefits. Annuities let you designate a beneficiary so that any remaining funds are transferred to another person after you die. Stocks typically don’t offer this option — instead, they would be included in your estate and split up according to directions in your will.

The Advantages of Stocks Over Annuities

So what about dividend-paying stocks? What are their advantages?

Dividend-paying stocks are a special sub-group of stocks. Like normal stocks, owning dividend-paying stocks makes you a shareholder of the company that issued the stock. In addition to owning these stocks, the company pays out some of its profits to shareholders in the form of dividends. In other words, you don’t just have the potential to earn income when you sell your shares, but you also can earn dividend income simply from owning the stocks.

Companies typically only pay dividends when they are doing well and earning a profit. Some companies are very consistent with their dividend payments, while others aren’t. Note that companies are not obligated to pay their shareholders a dividend, so dividend payments could end at any time. Still, holding a portfolio of stocks in companies that regularly pay dividends is a good strategy for making a regular stream of income.

Some of the main advantages of this type of stock include:

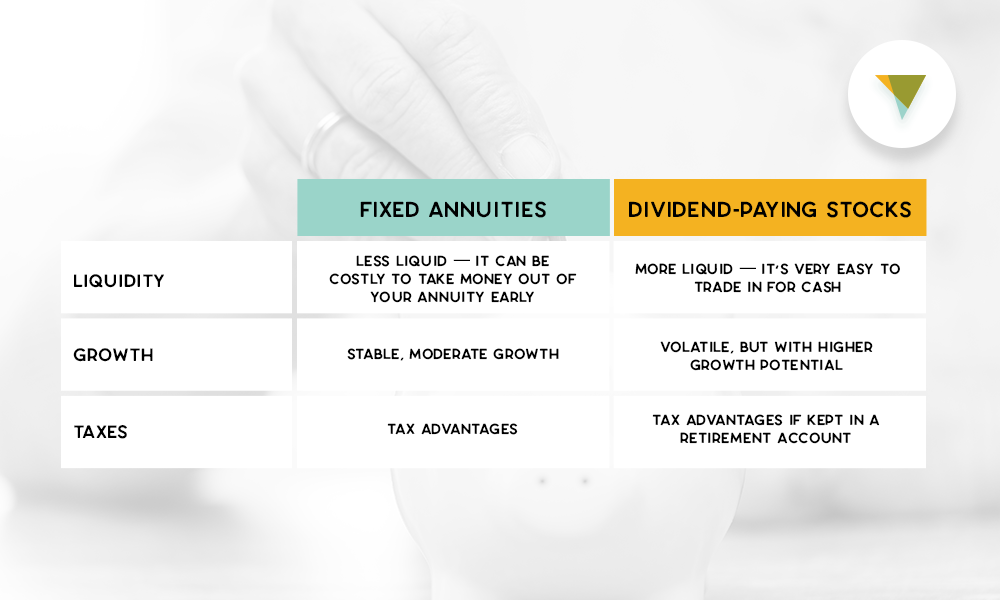

Liquidity. It’s usually quite easy to sell off your stocks and convert them to cash. In contrast, annuities are long-term products and you could face surrender charges or tax penalties if you make early withdrawals from your annuity.

Higher growth potential. The stock market is volatile. That volatility means that you may have the potential to generate high rates of return with stocks. On the other side of the coin, you can lose money too.

You can reduce your risk somewhat by diversifying the financial products in your portfolio. Options like mutual funds, ETFs, index funds and others build in some of this diversification automatically. The fact is that you could lose your money when you invest in stocks. (This downside also applies to variable annuities but it doesn’t apply to fixed annuities that earn a fixed minimum interest rate — as long as you keep your money in the account for the entire term.)

Tax advantages if kept in an IRA or other retirement account. While stocks by themselves are not tax-advantaged, you can keep your investment portfolio in a retirement account that is tax-advantaged. This could help your investments grow faster and help you pay less tax. Note that you may have limits on how much you contribute to your IRA and early withdrawal penalties may apply, similar to annuities. Learn more about the tax benefits of IRAs here.

Which is Right for You?

So which is the best for your retirement plan? It really depends on your circumstances, your financial goals, and your risk tolerance.

Fixed annuities are very safe, long-term options. You stow your money away and it grows steadily until retirement. They don’t offer massive growth, but they offer guaranteed growth and a stream of retirement income. They’re best for people who want to make sure that they have some retirement savings in the bank and need an income stream they can count on in retirement..

Stocks are less safe and can be short-term options. They are investment options that have a potential to create much larger returns, but you run the risk that you lose some money, too. Dividend-paying stocks add some additional income, but it is far from guaranteed.

Balancing Your Portfolio with Annuities and Stocks

Most people will want to ensure that their investment portfolios have a blend of lower-risk products (like fixed annuities) and some higher-risk products (like stocks). That means you might benefit from both fixed annuities and dividend-paying stocks.

Having both gives you the best of both worlds. It helps you feel safe because you know that the money you put in your annuity will grow steadily over time and can provide you with a guaranteed income in retirement. Meanwhile, you can use the money you invest in stocks to try to earn even larger returns.

How you balance your portfolio with lower- and higher-risk investments is up to you. You will likely change the mix over time as you get older and closer to retirement. As always, it’s a good idea to talk to a financial advisor for advice that’s specific to your own financial circumstances.

Read more: 6 Key Steps to Creating a Retirement Income Plan

Final Thoughts

The goal of retirement planning is to ensure you have enough money to pay your bills after you stop working. The difficult part is choosing a strategy to accomplish that. Do you want to play it safe and have very low-risk investments? Do you prefer to sacrifice some safety for potentially higher gains? Do you want a mix of both?

Both annuities and dividend-paying stocks can be a part of that strategy, but they have different functions. Fixed annuities give you security — they promise steady growth and guaranteed income. With fixed annuities, you know you won’t lose your retirement savings and that you’ll have a regular income to supplement your social security checks. While stocks can’t offer you the same security, they do offer potentially higher earnings.

Whichever you choose, it’s good practice to ensure some of your money is held in safe options, like annuities.

Canvas Annuity sells fixed retirement annuities with best-in-class rates and generous withdrawal features. Apply online today.

Resource Hub