Updated: March 21, 2024

Annuities vs. Money Market Accounts

Fixed annuities are insurance products that offer tax benefits, a guaranteed retirement income, and a guaranteed interest crediting rate. Money market accounts (MMAs) are bank accounts held by financial institutions that offer higher interest rates than typical bank accounts.

Both annuities and money market accounts are very safe places to put your money. But they are designed for different purposes and have different pros and cons. In this article, we explain the difference between the two and how you can decide which one is appropriate for you.

What is a Money Market Account?

A money market account (MMA) is a type of bank account. You keep money in the account for a period of time and the bank pays you interest on it. Banks created MMAs as an alternative to savings accounts in order to offer more competitive interest rates. Your money can usually grow faster in an MMA than it would in a regular savings account.

Many MMAs have tiered savings levels that offer higher interest rates for higher bank balances. The more money you keep in the account, the higher the interest rate they will offer. To earn the highest interest rate available, you must maintain a minimum daily balance. As of this writing, the highest interest rates for MMAs are about 0.75% with minimum deposits ranging from $0 to $100.

An MMA is neither a checking account nor a savings account, although it has elements of both. You will usually receive checks or a debit card for your MMA and will be able to make a few transactions a month. Because they are considered a savings-type instrument, withdrawals are limited by federal regulation to six per month. If more than six withdrawals occur within a month, the bank is obliged to change the account status to an unpaid checking account.

MMAs are deposit accounts insured by the Federal Deposit Insurance Corporation (FDIC) as long as you buy one from an FDIC-insured bank.

What MMAs Aren’t

Note that MMAs are not retirement accounts like IRAs or 401(k)s. By themselves, they do not offer tax-deferred growth, although you can hold an MMA within an IRA and get tax benefits that way.

Read more: Tax-Deferred Annuities: The Pros and Cons

Also, note that a money market account is not the same as a money market fund. Money market funds are separate insurance products that function like mutual funds for short-term debt instruments. Money market funds are very different from MMAs, so we won’t discuss them in detail here.

Pros and Cons of Money Market Accounts and Annuities

MMAs are great if you want a conservative investment and don’t need high growth but they’re not great if you want moderate growth or are trying to grow your money tax-deferred or over the long term.

Like MMAs, annuities are also very safe investments. An annuity is an insurance product that you buy from an insurance company. There are many different types of annuities, including fixed annuities, variable annuities, and fixed-indexed annuities. Fixed annuities are the ones closest to MMAs (because they are the safest and offer a fixed minimum interest rate) so they’re the ones we’ll compare to MMAs in this article.

Read more: What are annuities and how do they work?

Here is a quick description of the pros and cons of both MMAs and annuities.

Risk

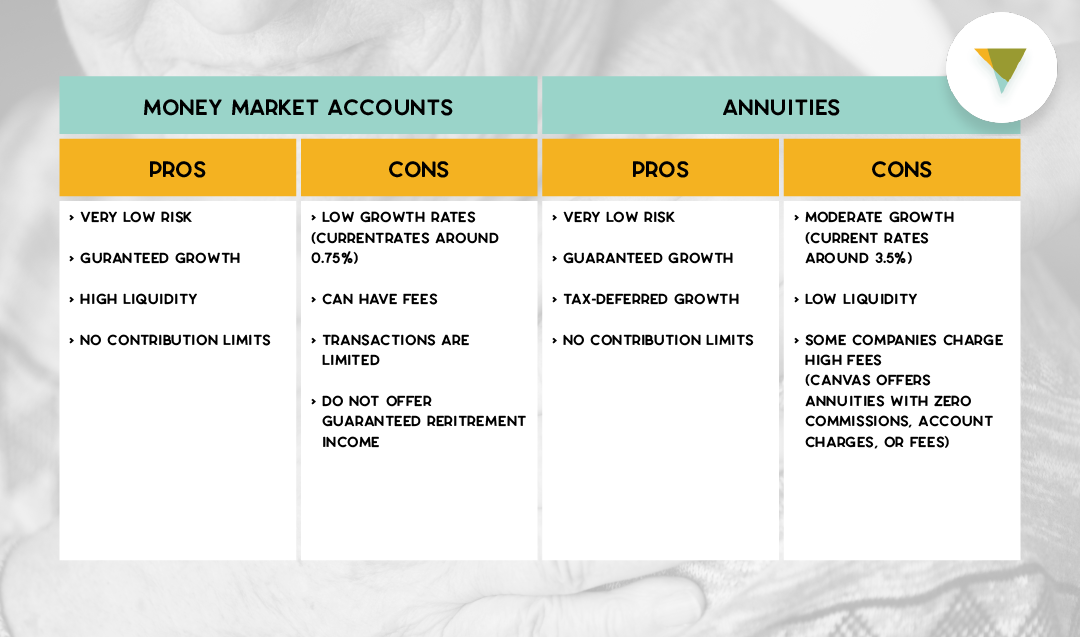

The main advantage of MMAs is that they are very low-risk. They offer a fixed interest rate which guarantees your money will grow. Also, they are FDIC-insured if they are opened in an FDIC-insured bank. That means that if the bank goes out of business, your deposits are insured for up to $250,000.

Fixed annuities are also very safe. They offer a fixed minimum interest rate, which means your money is guaranteed to grow over time. Annuities, which are not FDIC insured are sold by insurance companies. They are backed by the claims-paying ability of the insurance company.

Note that some annuities are higher risk. Both variable annuities and fixed-indexed annuities have interest rates that fluctuate with underlying investments or a linked index. These annuities are higher risk—and you could even lose money when you choose them. All the annuities Canvas Annuity sells are low-risk, fixed annuities.

Liquidity

Liquidity refers to how easily you can access your money without it losing value. Your bank account is very liquid because you can quickly take money out of the bank and, when you do, the balance in the account is what you can take out. Money invested in real estate isn’t very liquid because it can take a long time to convert your property to cash, and you could lose some value when you do.

MMAs are fairly liquid. They are a lot like a checking account. There are some restrictions on how many transactions you can make each month, but you have access to your entire account balance at any time.

Annuities are much less liquid. They are designed for retirement savings, so they’re meant to be a place you keep your money over a long period of time. Early withdrawals from your annuity could be subject to withdrawal penalties like surrender charges or IRS tax penalties. Before purchasing an annuity you should make sure you have set aside funds for use in emergencies and can pay all of your monthly expenses.

Having less liquidity may seem like a disadvantage, but there is a benefit. Insurance companies can offer higher crediting rates than banks specifically because annuities are a long-term product. Surrender charges disincentivize people from taking money out earlier and allow the insurance company to provide those higher rates for more people. Plus, leaving your money in the annuity means you are earning tax-deferred interest over a long period of time. The larger your annuity balance is when you decide to annuitize, the larger your lifetime paycheck will be so it’s in your best interest to leave your money in the contract.

Many insurance companies do have a free withdrawal provision on their annuities. Canvas annuities even let you withdraw 10% of your accumulation value each year, without incurring surrender charges.

Rate of Return

MMAs traditionally offer rates of return that are higher than regular savings account rates. They often offer the best rates when you keep more money in them. For example, you might have to keep as much as $25,000 in an MMA to get the best rates.

As of this writing, the highest MMA rates are not that much better than regular savings account rates, with the best MMA rates around 0.75%. In comparison, some high-yield savings account interest rates are as high as 1%. So while the rate of return on MMAs can be better than regular bank accounts, that’s not always the case.

Annuity account interest crediting rates are typically much higher than both MMAs and regular savings accounts. Canvas offers some of the best rates in the industry, with rates as high as 4.30% as of this writing. Check out the current fixed annuity rates for Canvas products here.

Read more: Best fixed-annuity rates

Fees

Many MMAs do not charge fees, but some do. When they charge fees, it’s common to charge fees only when you do not keep a minimum daily balance.

Some companies charge fees on annuity products, but others don’t. For example, variable annuities can have quite high fees. In contrast, fixed annuities typically have few or no fees. Canvas does not charge account fees on our annuity products.

Tax benefits

MMAs do not offer any tax benefits by themselves. If you hold your MMA in a tax-advantaged account, like an individual retirement account (IRA), then it will receive the tax benefits of that account.

Annuities are considered retirement products, so they receive significant tax advantages like tax deferral. Read all about annuity taxation here.

Which One is the Better Option?

Which option is best for you? It really depends on your goals.

If you need a short-term way to save, MMAs could be appropriate. They allow you much more flexibility as to when you take out your money. Before you open an MMA, make sure you check other rates at your financial institution — you might be better off buying certificates of deposit or opening a high-yield savings account for your short-term savings goals.

If you need a longer-term solution for growing your retirement savings, then an annuity product may be more appropriate. Fixed annuities typically offer much better interest rates than MMAs, so your money will grow faster. They also offer tax benefits as well as a guaranteed income in retirement. So if you’re looking for a steady income to supplement your social security check, an annuity could be perfect for you.

If you’re not sure, consider consulting with a financial advisor to create a retirement plan. They can tell you about all the investment options that there are at your disposal and which investment choices may be most appropriate for your particular circumstances.

Interested in buying an annuity? Apply online right now.

Resource Hub