Updated: March 7, 2024

What is an Annuity Exclusion Ratio? How Does It Work?

The government likes to collect taxes. But there’s good news if you want to use an annuity to secure guaranteed lifetime income as part of your comprehensive retirement plan. Depending on the source you use to fund the annuity, a portion of each annuity payment may not be subject to income tax. This is called the annuity exclusion ratio.

Annuities are issued by life insurance companies and are a great way to secure a stable, guaranteed flow of income in retirement. When you decide to fund a portion of your retirement with an annuity, the source of the funds you use is important from a tax perspective.

Taxes can take a bite out of your annuity income, but the exclusion ratio defines just how much of the payment you receive will be tax free. As an annuitant, or the person receiving the income, you want to understand what the monthly expected return is on your purchase of an annuity. Let’s dive into some of the specifics of how the exclusion ratio works.

Exclusion Ratios Explained

The annuity exclusion ratio is the portion of an annuity payout that is not taxed. The exclusion ratio is only applicable if you bought your annuity using after-tax money that was sitting in vehicles like savings accounts, CDs, etc.

When you receive payouts from an annuity funded with after-tax money, the part of your payout that qualifies as the initial premium comes back to you tax free but you will owe taxes on the gains, or interest, you earned on your annuity. After all, if you are using after-tax money to fund your annuity, you don’t want to pay taxes twice on that amount! That’s why the exclusion ratio exists.

To summarize, when you purchase an annuity with after-tax money (also known as non-qualified annuities), the principal is not taxable.

If you use before-tax funds, like tax-advantaged retirement accounts (401k, pensions, IRAs), then the exclusion ratio does not apply and you pay taxes on the entire amount of your withdrawal.

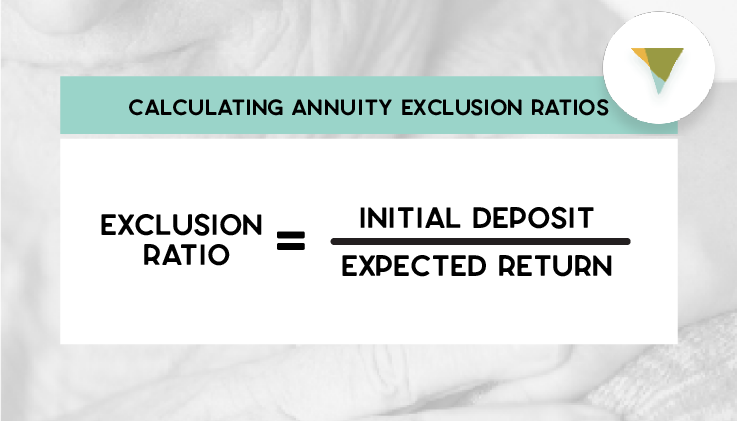

Calculating Annuity Exclusion Ratios

How can you calculate the exclusion ratio (tax-free portion) of your income annuity? Here is a simple explanation:

Determine your initial deposit amount. This is the money you used to fund your annuity.

Calculate your expected return. This is the amount you expect to receive annually adjusted by the type of payout you choose when you annuitize your contract. The number of annuitants (if it’s a single or joint-life annuity) also comes into play. The IRS provides a document called Publication 939 with worksheets that can help you with the calculation. It is recommended that you complete these forms with your tax professional or financial adviser so you have a better understanding of the payout amounts.

Calculate the exclusion ratio. Divide the initial deposit by the expected return. See an example below under “Fixed Annuities.“

Determine the tax-free portion. Once you know the ratio, multiply the exclusion ratio by the payment you receive from the annuity company to find the tax-free portion of your monthly payment.

Calculations for Fixed Annuities

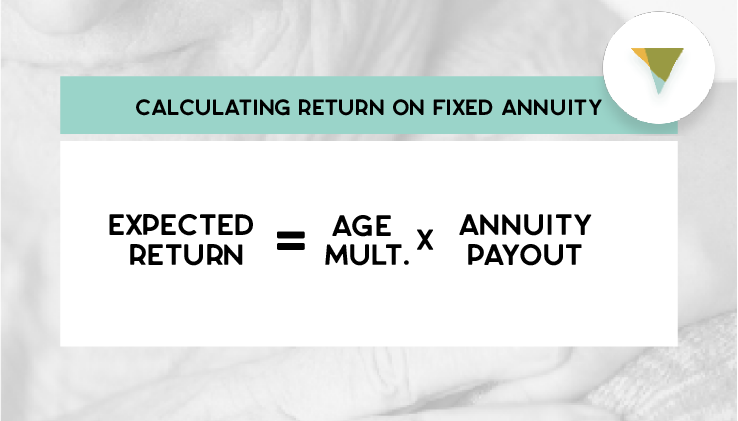

Let‘s say you buy an immediate fixed annuity and deposit $100,000 with the insurance company. As part of the contract, the company pays you $1,000 per month ($12,000 per year) for the rest of your life. So with an initial deposit of $100,000, you then need to determine your expected return.

To do this, you multiply your annual annuity payout ($12,000) times the correct multiplier based on your age and the type of payment you receive (essentially calculating your life expectancy).

In this case, your annuity payment is based on your life only (meaning no beneficiaries receive continuing payments after you die) and will be paid distributions from the annuity for as long as you live, so you should use the aforementioned IRS Publication 939 and refer to Table V.

Other payout scenarios are presented within other tables in the publication. Let‘s assume you are 70-years-old at the time of your purchase. According to the table, your multiplier is 16. Therefore, your expected lifetime return is 16 x $12,000 or $192,000.

The exclusion ratio is then calculated as:

Investment / Expected Return = $100,000 / $192,000 = 52%

Fifty-two percent is the portion of your payment that is tax-free. It’s equal to $6,240 per year (52% of $12,000). The remaining $5,760 is the taxable portion.

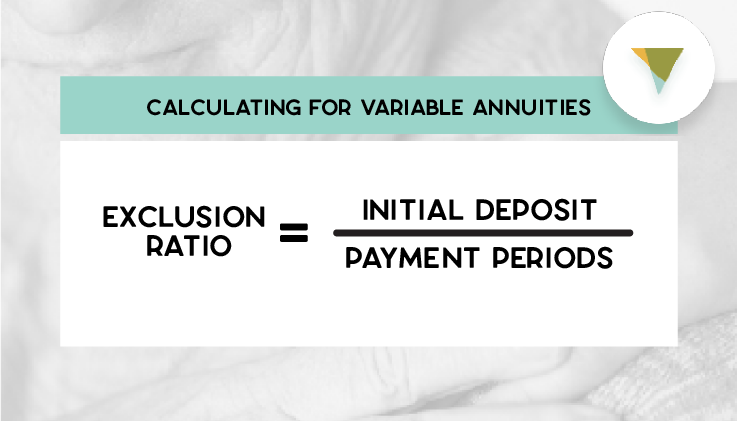

Calculations for Variable Annuities

A variable annuity works differently than a fixed annuity since this product is exposed to investment risk. For these types of products, you calculate the exclusion ratio by dividing the initial investment over the payment period. This amount is removed from the taxable income of the segment, with anything over that amount taxed as ordinary income.

If you purchase a variable annuity for $100,000 with a payment period of 10 years or 120 months, you would calculate your exclusion ratio by dividing your initial investment by your number of payment periods, or $100,000 divided by 120. Each month your exclusion ratio would be around $833 and any gains earned would be considered taxable income.

Does an Early Withdrawal Affect the Exclusion Ratio?

What happens if you withdraw funds early? Generally you should avoid early withdrawals because this can lead to significant tax penalties.

In fact, the internal revenue code dictates that this money must be treated as earnings in a last-in/first-out formula. You would pay taxes on the whole amount of money withdrawn early until the annuity only has the initial investment amount remaining. At this point, you can withdraw that principal amount tax free.

Other Special Considerations

Here are a few other items to keep in mind related to the exclusion ratio:

- What if you live longer than the IRS exclusion ratio estimate? In this case, the IRS assumes that you will use up your principal by the end of your estimated lifespan—say 16 years. If you live longer, then 100% of your payments are taxable each year thereafter until you die.

- What if you are using qualified money (IRAs, 401k money, etc.) to buy an annuity? In this case, the exclusion ratio does not apply, and you pay taxes on the entire amount each year. That’s because you haven’t paid any taxes on that money yet.

The Bottom Line

The annuity exclusion ratio tells you what percent of your annual annuity income you will have to pay taxes on when you begin taking periodic payments in retirement. If you are using non-qualified money, you already paid taxes on the principal, so the annuity exclusion rate is calculated by dividing your principal paid by your expected return.

If you buy your annuity with qualified money, though—like money in a retirement savings plan—you will pay taxes on the entire annuity payout amount.

Starting your annuity journey with a fixed annuity allows you to safely build assets prior to needing the money in retirement. Canvas annuities are multi-year guarantee annuities, or MYGAS. Even though MYGAs are conservative products, offering guaranteed rates and 100% protection from loss of principal, they offer very competitive interest rate returns that are almost always better than other conservative investments like CDs and savings accounts.

Sources:

annuity.org — Annuity exclusion ratio (Christian 2022)

Smart Asset — What Is the Annuity Exclusion Ratio? (Reed 2019)

The Balance — What is an Exclusion Ratio? (Munyi 2021)

Resource Hub