Updated: March 7, 2024

How Does An Indexed Annuity Differ From A Fixed Annuity?

With an indexed annuity, your account grows with an interest rate calculated using an underlying stock market index. With a fixed annuity, your account grows with a fixed minimum interest rate. Fixed annuities are safer, but fixed-indexed annuities have the potential for higher growth.

Retirement planning is fundamentally about planning for an uncertain future. On the one hand, you want to grow your nest egg as much as possible. On the other hand, you typically want to choose relatively safe investment options so that you don’t lose your money in a volitile market.

The difference between fixed annuities and indexed annuities is in their risk. With fixed annuities, your money is guaranteed to grow steadily. Indexed annuities are more volatile because they are tied to a stock market index that fluctuates with the performance of the stock market.

Read on to learn exactly how each of these options works and the pros and cons of each.

Indexed Annuities

Indexed annuities, often called either fixed-indexed annuities or equity-indexed annuities, work just like regular annuities. They are annuity contracts that you buy from a life insurance company. During the accumulation phase, your premiums are added to your annuity account. That account earns interest and grows over the term of the annuity.

You can then annuitize your annuity to start the payout phase. When you do that, you turn your annuity account into a steady stream of income payments.

What makes fixed-indexed annuities different from other types of annuities is how they calculate the interest crediting rate.

How They Work

When you buy a fixed-indexed annuity, you select a market index for your annuity to follow.

A market index measures the performance of a group of securities. For example, the S&P 500 index tracks the performance of 500 large US companies. Some other market indexes include the Dow Jones Industrial Average and the Nasdaq Composite Index.

The interest crediting rate your premiums earn depends on your chosen market index. If your index performs well over the term of the annuity, your interest crediting rate goes up, and your account grows faster. If your index performs poorly, your rate of return decreases, and your account doesn’t grow as fast.

The amount that you are credited to your account depends not just on your market index but also on some other factors.

- Participation rate. This is the percentage of a market index’s return that you earn. For example, you might have an 80% participation rate. That means that if your market index returns 10%, you will only receive 80% of that gain for a rate of return of 8%.

- Spread/asset/margin fees. Some annuity companies charge spread fees, which are subtracted from your earnings. For example, if your index gained 8% and the spread fee was 2%, you would only earn 6%.

- Rate floors. The rate floor means that you will not lose money with a fixed-indexed annuity on account of poor market performance. Most fixed-indexed annuities have a rate floor of 0% or 1%. Your rate will not fall below that number.

- Rate caps. Fixed-indexed annuities typically have a rate cap, also called a rate ceiling. That means that even if your market index performs very well, your rate will be capped. For example, if your annuity has a cap of 6%, even if your index gains 20%, the rate you are credited will only go as high as 6%.

Are fixed-indexed annuities a good investment? It depends on what you’re looking for.

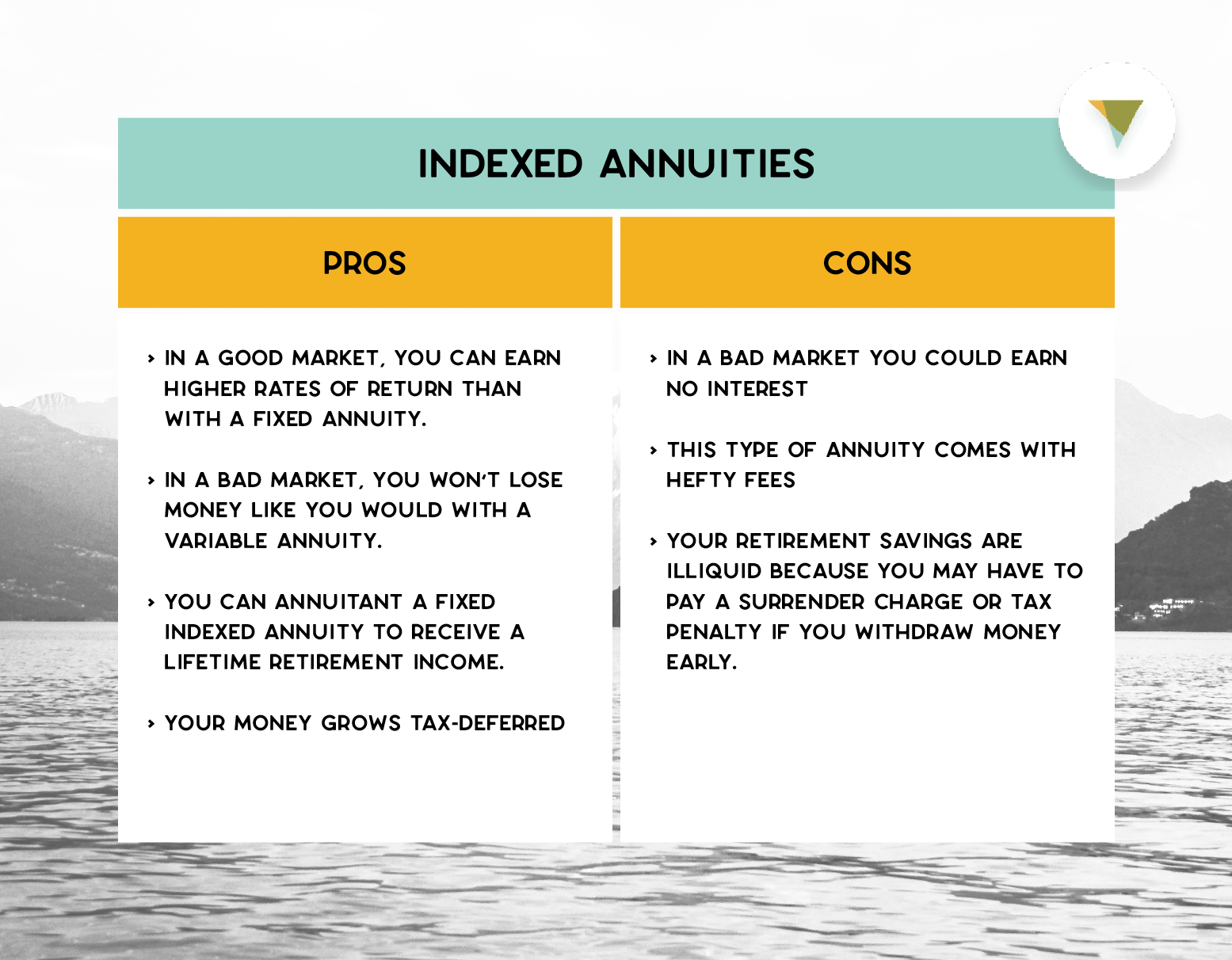

Pros

There are several benefits to owning a fixed-indexed annuity.

- If the market is good, you can earn higher rates of return than you can with a fixed annuity.

- If the market is bad, you won’t lose money like you could with a variable annuity.

- You can annuitize your fixed-indexed annuity to receive a lifetime retirement income.

- Your money grows tax-deferred.

Cons

Fixed-indexed annuities do have some drawbacks, including:

- In a bad market, you could earn no interest.

- This type of annuity can come with hefty fees.

- Your retirement savings are illiquid because you may have to pay a surrender charge or tax penalty if you withdraw money early.

Fixed Annuities

So how do fixed annuities compare?

Fixed annuities are the simplest form of annuity products. You can buy them with a lump sum payment (single premium) or with several payments over time (flexible premium). You can buy them as an immediate annuity that starts to pay you back right away or as a deferred annuity that has time to grow over the term of the contract.

After annuitization, they begin to pay you a regular income stream.

How They Work

When you buy a fixed deferred annuity, you are offered a guaranteed minimum rate of interest. That means that the fixed rate of interest you are credited will never be lower than the amount listed. Your money is guaranteed to grow over the term of the annuity.

For example, Canvas Annuity currently offers the Future Fund fixed annuity product with a guaranteed interest rate of 4.60%. (Check out the most recent fixed annuity rates here). With this product, the interest rate you are credited will never fall below 4.60% during the term of the annuity.

Like other annuities, fixed annuities grow tax deferred. That means you don’t pay taxes on withdrawals or any earnings in the year you earn them. Instead, you pay ordinary income tax when you receive withdrawals—often when you’re retired. Read more about annuity taxation here.

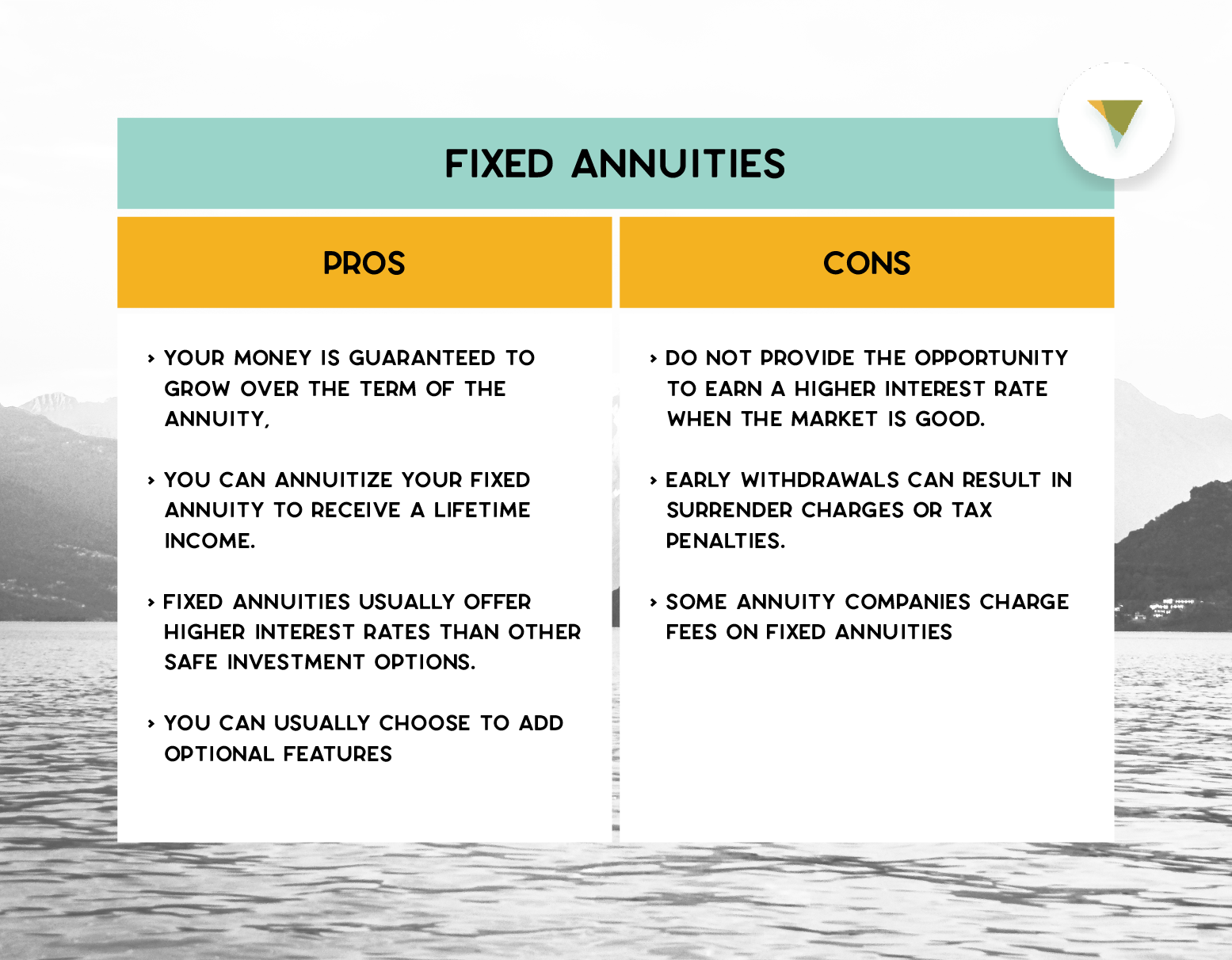

Pros

Fixed annuities are very popular retirement planning products because they offer a number of benefits. Here are some of the advantages of a fixed annuity:

- Your money is guaranteed to grow over the term of the annuity, even during a recession (as long as you don’t make early withdrawals).

- You can annuitize your fixed annuity to receive a lifetime income.

- Fixed annuities usually offer higher interest rates than other safe investment options like certificates of deposit (CDs).

- You can usually choose to add optional features, like death benefits.

Cons

Fixed annuities are not for everyone. Drawbacks of this type of annuity include:

- Fixed annuities do not provide the opportunity to earn a higher interest rate when the market is good.

- Early withdrawals from your annuity can result in surrender charges or tax penalties.

- Some annuity companies charge fees on fixed annuities (Canvas Annuity offers fixed annuity products with zero commissions, account charges, or fees).

What to Know Before Purchasing an Annuity

Annuities are powerful retirement planning tools. They don’t just offer tax-advantaged growth, but they’re also the only product that can provide a guaranteed income that lasts for the rest of your life.

Still, they’re not for everyone. You may want to think about your financial situation, your financial goals, and your risk tolerance before buying an annuity. Consider:

- Length of investment. Annuities are best over the long term. They’re not ideal for short-term investments because you may have to pay a surrender charge or a tax penalty if you take your money out early. Before you buy an annuity, think about whether you’ll need that money in the short term.

- Legacy planning. Many annuities can be passed on to beneficiaries, but not all can. If you want to ensure that your loved ones receive your annuity when you die, think about buying an annuity with death benefits.

- Risk tolerance. Fixed annuities are very safe investments. Fixed-indexed annuities are less safe because they are exposed to market risk, but they are still much safer than other investment options. If you’re looking for very risky investments with lots of upside potential, neither of these kinds of annuities may be right for you. You may prefer mutual funds or stocks.

If you’re not sure if an annuity is right for you, consider speaking to a financial advisor.

Which is Best for You?

Which of these different types of annuities is right for you?

Fixed annuities are best for those who want a very safe place to put their retirement savings because they offer guaranteed growth. For that reason, they’re also typically a better choice in a recession.

Fixed-indexed annuities are better for people with higher risk tolerance who want the potential for higher growth. Buyers must be comfortable with the chance that their annuity account value will not grow if the market index they choose to follow performs poorly.

In both cases, you can annuitize to receive income for the rest of your life.

Ready to buy a low-risk fixed annuity and set yourself up for a guaranteed retirement income? Check out Canvas’ annuity products and, when you’re ready, apply for one online.

Resource Hub