Table of Contents

Updated: February 17, 2026

How to Calculate the Taxable Income of an Annuity

Annuity income is taxable. With qualified annuities, 100% of withdrawals are taxable. With non-qualified annuities, only a portion of the withdrawals are taxable. To calculate the taxable income from a non-qualified annuity, determine the cost basis, divide it by the accumulation value to get the exclusion ratio, and then subtract the exclusions.

Besides offering lifetime income, annuities also offer a way to earn interest and grow your retirement savings. One of the main advantages of annuities is that they’re tax-deferred (but not tax-free). Income tax deferral means that rather than owe taxes on annuity income in the tax year you earn the income, you owe it in the year you receive distributions.

Tax deferral is a huge benefit for two reasons.

First, tax deferral means that your money compounds and grows faster. Second, tax deferral means that most people end up paying taxes in retirement when their income is relatively low, and they fall into a lower tax bracket. The result is that they pay a lower marginal tax rate, and so pay less tax overall.

That’s a massive advantage, but it also complicates the calculation of what income you’ll have to pay taxes on. In this article, we provide a guide for how to calculate the taxable income of a deferred annuity.

Qualified vs. Non-Qualified Annuities

One of the first considerations when calculating the taxable income of an annuity is whether the annuity is qualified or non-qualified.

- Qualified annuities are funded with pre-tax dollars — money that hasn’t yet been taxed. When money is put directly into a retirement account like a 401(k) or an individual retirement account (IRA), it’s qualified.

- Non-qualified annuities are funded with after-tax dollars — money you’ve already paid tax on.

If your annuity is qualified, the entire distribution is taxable — 100% of it. You haven’t paid taxes on either your initial premiums or the interest you’ve earned over time; therefore, the entire withdrawal is taxable when you receive those distributions.

If your annuity is non-qualified, calculating the taxable income is more complicated. When you withdraw money — either in a lump sum payment or in smaller payments over a period of time — you don’t have to pay taxes on the principal. However, you will have to pay taxes on any interest income you earn.

Calculating how much of each withdrawal is “principal” and how much is “earned interest” requires some care. The Internal Revenue Service (IRS) will tell you when it’s time for you to pay it, but you can calculate this number yourself too.

Calculating the Taxable Portion of a Non-Qualified Annuity

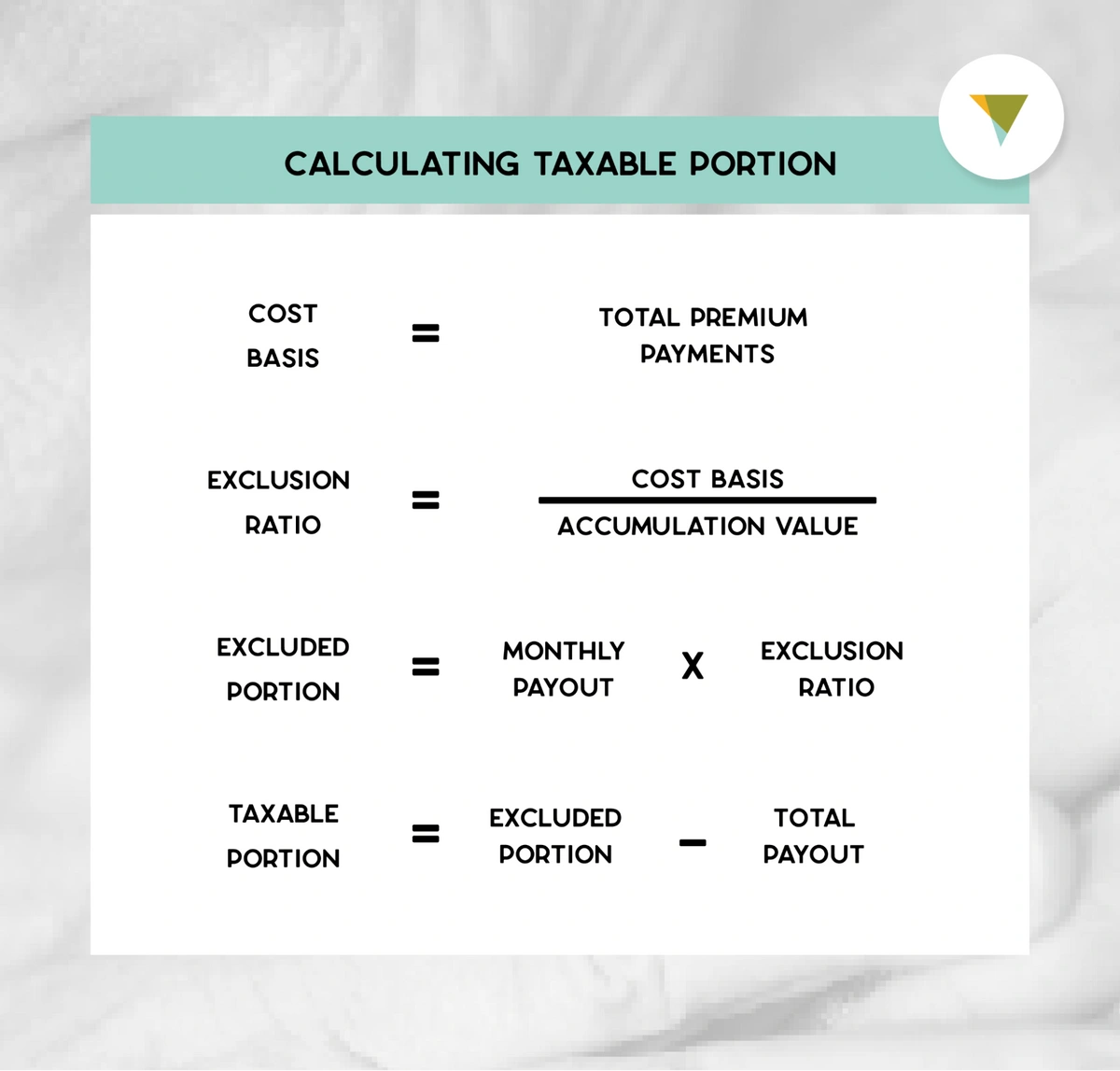

To calculate the amount of a non-qualified annuity payment that is taxable, you’ll need to:

- Determine the cost basis

- Divide your cost basis by the accumulation value to get the exclusion ratio

- Multiply your monthly payout by the exclusion ratio

- Subtract the excluded portion from the total payout

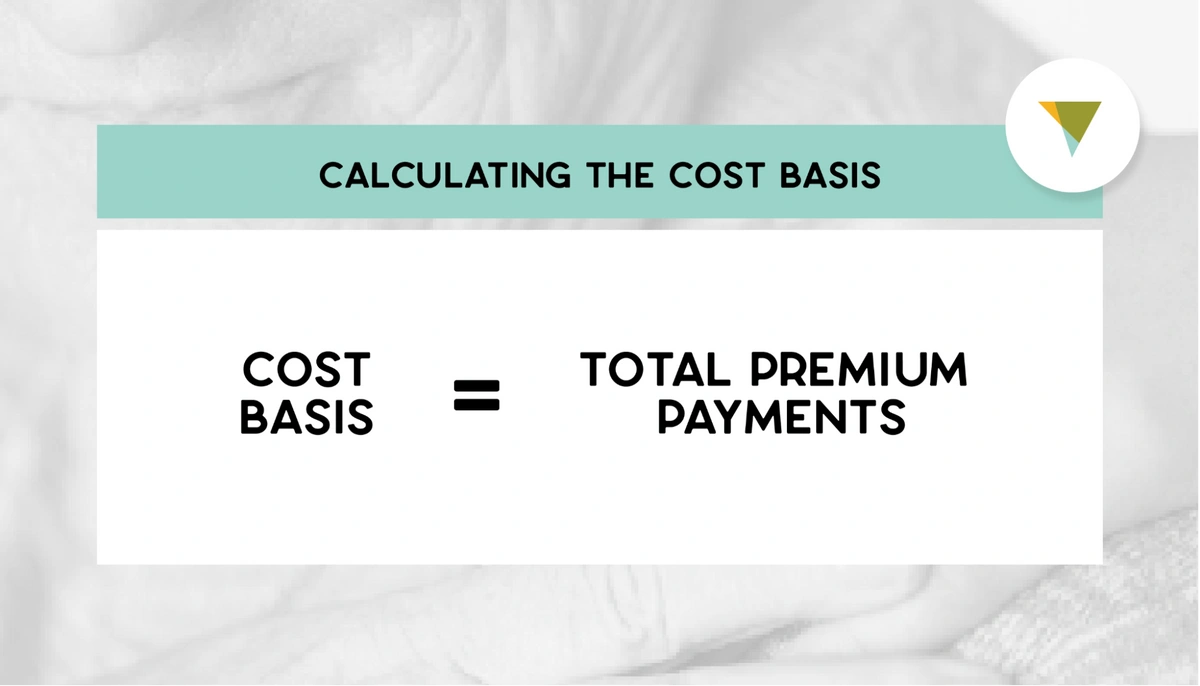

Step 1: Determine the Cost Basis

The “cost basis” is the amount of an annuity that you put in — i.e., the premiums that you contributed. This is your principal. With a non-qualified annuity, this is money that you might have had in savings or a CD and that you used to buy an annuity.

It’s easy to calculate the cost basis of your annuity account. It’s just the total value of your premium payments.

Cost basis = Total Premium Payments

For example: If you made a single lump sum premium payment of $100,000, then your cost basis is $100,000. Or, you might have made 10 payments of $10,000; in that case, your cost basis is still $100,000.

Step 2: Divide Your Cost Basis by the Accumulation Value to Get the Exclusion Ratio

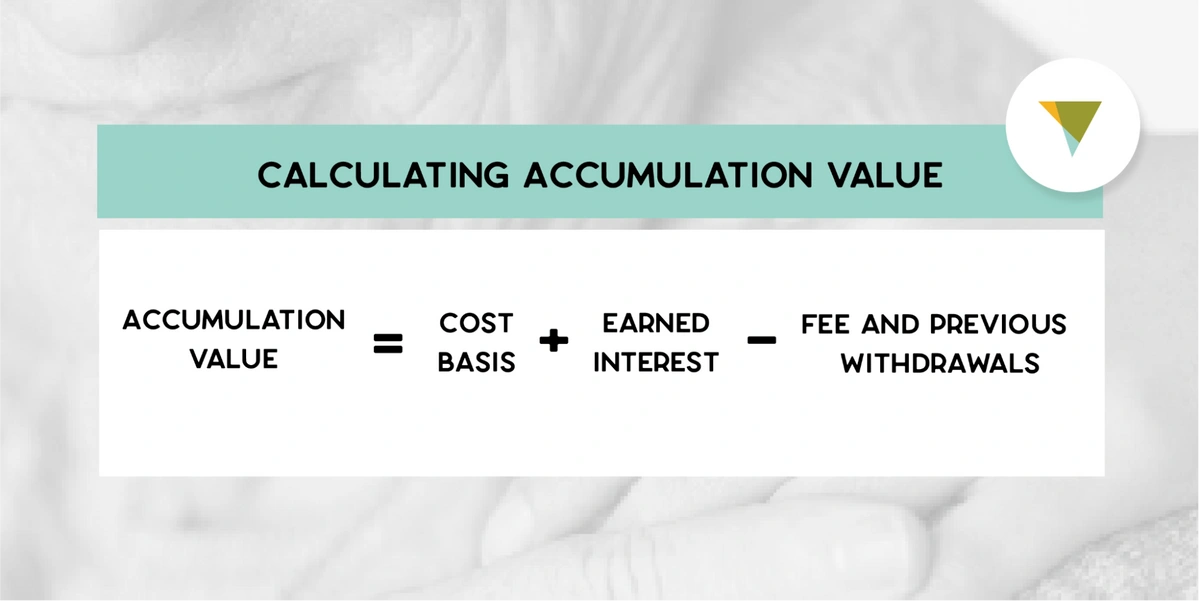

Next, you need to know the accumulation value.

The accumulation value of an annuity is the total value of the annuity account. It is made up of your premiums plus interest that those premiums have earned, minus any fees or withdrawals.

Accumulation Value = Cost Basis + Earned Interest - Fees and Previous Withdrawals

For example: Imagine that your $100,000 from the previous example had sat for several years and earned $50,000 in interest. And imagine you didn’t take any withdrawals, and there were no fees. Your accumulation value would be $100,000 + $50,000 - $0 = $150,000.

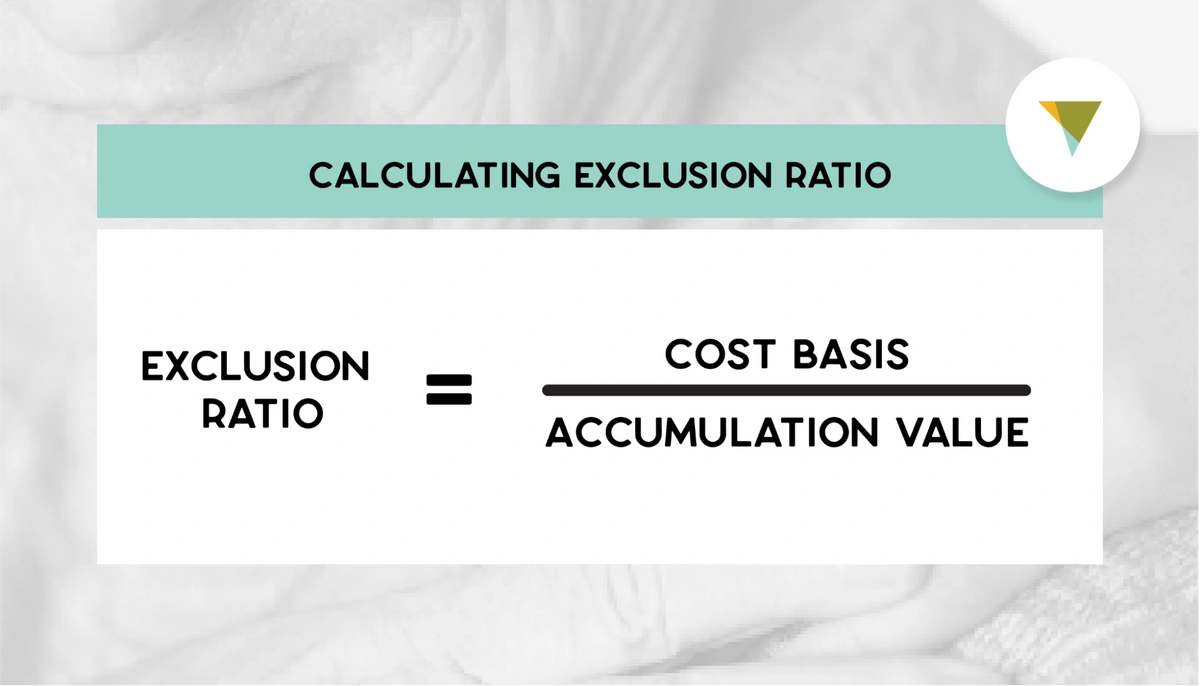

You need to know the accumulation value because it helps you determine something called the annuity exclusion ratio. The exclusion ratio helps us find the proportion of each payment that is excluded from being taxed, and we’ll use it in the next step.

To get the exclusion ratio, divide the cost basis by the accumulation value.

Exclusion Ratio = Cost Basis / Accumulation Value

For example: Our cost basis in the previous example is $100,000, and the accumulation value was $150,000. The exclusion ratio = $100,000 / $150,000 = 0.66 or 66%. In other words, about 66% of each payment is a return of your own capital and would be excluded from taxation.

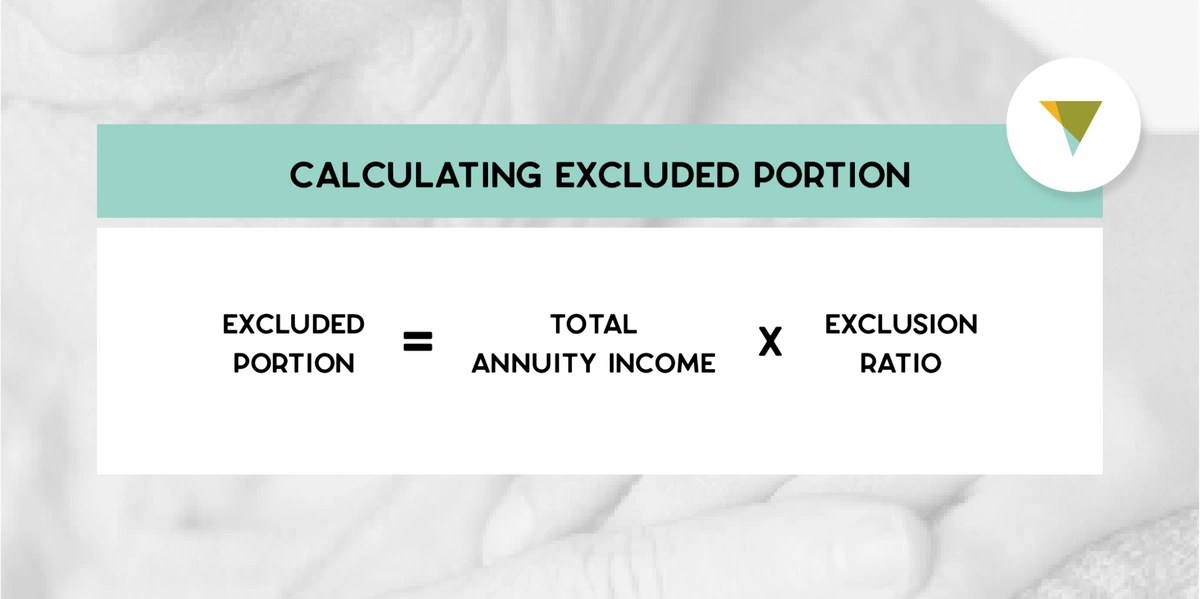

Step 3: Multiply Your Monthly Payout by the Exclusion Ratio

Now, use the exclusion ratio to find out how much of each withdrawal is excluded from taxation. Do this by multiplying the exclusion ratio by the withdrawal or payment amount.

Excluded Portion = Total Amount of Annuity Income * Exclusion Ratio

For example: Imagine your monthly payments were $350, and your exclusion ratio is 66%. Then the value excluded from your taxable income is $350 * 0.66 = $210.

That means that you won’t owe taxes on $210 of your $350 payment because it is simply a return to you of your own money that has already been taxed.

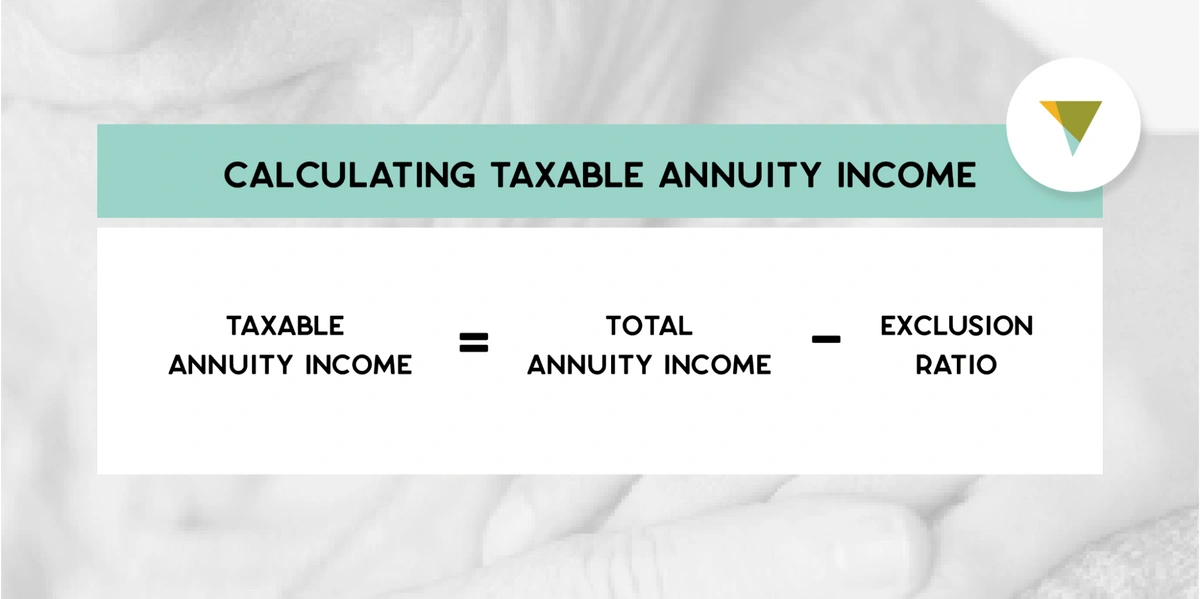

Step 4: Subtract the Excluded Portion from the Total Payout

Finally, to figure out the taxable portion — how much will be taxed — we subtract the excluded portion from your monthly payment.

Taxable Annuity Income = Total Amount of Annuity Income - Excluded Portion

For example: In the last step, our annuity income was $350 and the excluded portion was $210. The taxable income would be $350 – $210 = $140. So $140 of the payment would be taxable as ordinary income.

Do All Types of Annuities Use this Calculation?

The above is how you calculate the taxable income from withdrawals from a non-qualified annuity. It’s done this way so that you don’t end up paying taxes on the same money twice.

Of course, as previously mentioned, it’s different for qualified annuities. With qualified annuities, none of the money in your account has been taxed yet. So, when you withdraw it, 100% of it is taxable income.

Here’s another special case. If you are receiving lifetime income from a non-qualified annuity, you may live long enough that you outlive your principal. In other words, you may get to the point where all your initial premium payments have been paid back to you. From that point on, the payments are 100% taxable.

Other Things You Should Know About Annuities and Taxes

One other consideration is that annuity income is taxed as ordinary income tax rather than as capital gains. That means your overall income tax bracket will determine your tax rate. How much money you receive at a time can impact how much tax you pay overall.

In other words, the annuity payout option you choose has tax implications.

One payout option is to simply receive all your money back to you in a single lump-sum payment. The problem with this is that your income will be really high that year, so you’ll fall into a higher tax bracket, and you’ll pay a higher marginal tax rate. That means you may pay a higher amount of tax overall.

Instead, many retirees choose to spread their payments out over time. This doesn’t just help them ensure that they have a regular stream of income. It also helps them lower their income in any given year so that they stay in a lower tax bracket and pay a lower federal income tax rate.

Also, consider that early withdrawals from an annuity can not only cost you hefty surrender charge fees from your insurance company but also prompt a 10% tax penalty from the IRS if you withdraw before you’re 59½. So early withdrawals may be especially costly.

Note: Annuity taxation can be complicated, but it really matters. If you’re not sure how to optimize your taxes, consider speaking to a tax professional.

The Bottom Line

Annuities are the only financial product that can offer you a guaranteed retirement income. Besides social security and a pension, they’re one of the most secure ways to earn a retirement income. Annuity products are a powerful addition to your retirement plan, in part because they offer robust tax advantages.

Canvas Annuity offers simple, low-risk fixed annuity products that grow over time with guaranteed minimum interest rates. They have zero commissions, account charges, or fees.

Looking to learn more about our annuities and their tax implications? Reach out to Canvas’ friendly licensed reps for more information.

Resource Hub