Table of Contents

- Lifetime Annuities are a Payout Structure, Not an Annuity Type

- How Do Lifetime Payout Structures Work?

- What Types of Annuities Offer Lifetime Payout Options?

- Pros and Cons of Choosing a Lifetime Annuity

- Key Factors to Consider When Choosing a Lifetime Annuity

- Making the Choice: Is a Lifetime Annuity Right for You?

Updated: March 7, 2024

What is a Lifetime Annuity?

A lifetime annuity is a financial product that offers guaranteed income payments for the rest of your life.

Planning for retirement is complicated. You know you need to save as much money as possible — but how much is enough? What if you run out?

Lifetime income annuities are designed to reduce that uncertainty. They help give you peace of mind knowing that you’ll have a regular paycheck until you die. In this article, you’ll learn what a lifetime annuity is, how they work, and key factors to consider when deciding whether they’re right for you.

Lifetime Annuities are a Payout Structure, Not an Annuity Type

Annuities are contracts you make with a life insurance or annuity company. You agree to fund your annuity account by paying premiums, and the life insurance company agrees to pay you that money, plus interest, back to you through annuity payments.

Rather than a distinct type of annuity product, lifetime annuity (straight life or life annuity) usually refers to a payout structure where you opt for payments to last until you die.

Technically, any annuity can become a lifetime annuity. When you’re ready to annuitize your annuity and start receiving your income, you choose between payout options. One of the payout options you can choose is to receive income for life.

If you choose that payout option, you’re choosing to have a “lifetime annuity” and your payments will only stop when you die.

How Do Lifetime Payout Structures Work?

Lifetime payout structures can vary. Typically, you’ll get to choose whether to receive monthly, quarterly, or yearly payments. The value of those payments will be determined by several factors, including:

- The value of your premium payments

- What type of annuity you chose and how much interest your annuity earned

- Your age when you annuitize and your life expectancy

- Additional options, like whether you have a joint annuitant

When you’re annuitizing, you usually don’t have to choose a lifetime payout option. Some of the other common payout options you’ll have are:

- Term certain. In this option (also called fixed period or period certain) you receive payments for a specific term — say, 10 years. After that period, payments stop. If you die before the term ends, any remaining funds are paid to your beneficiaries.

- Lump sum. In this option, you’ll receive your income in a single, lump sum payment.

- Life annuity with term certain. In this option, your payments last until you die. If you die within the specified term — for example, 10 years — the remaining funds are paid to your beneficiaries.

- Joint and survivor. In this option, your payments last while both you and a joint annuitant, like your spouse, are alive. Payments stop when both of you die.

What Types of Annuities Offer Lifetime Payout Options?

Annuity types that often offer a lifetime payout option include:

- Immediate annuities. These are annuities that annuitize immediately and begin to pay you back soon after you buy them.

- Deferred annuities. These grow your money over a specified term, often several years. They let you steadily increase your annuity account before converting it into a stream of income.

- Fixed annuities. These grow your annuity account at a fixed minimum interest crediting rate.

- Variable annuities. These grow your annuity account at an interest rate that is determined in part by stock market performance.

- Fixed-indexed annuities. These grow your annuities at an interest rate that is tied to a market index like the S&P 500.

One of the main features of annuities is the option of having guaranteed income for the rest of your life. Check with your annuity provider before purchasing to find out about all the payout options they offer.

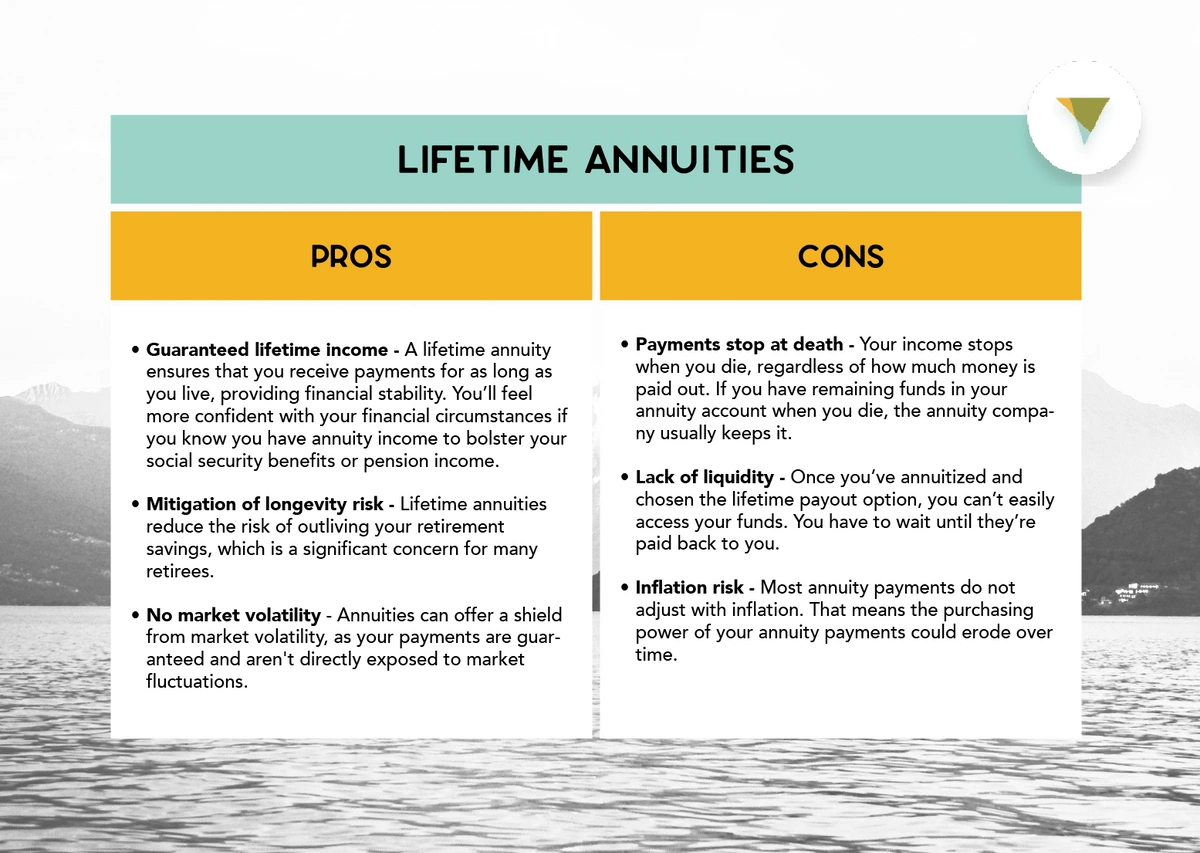

Pros and Cons of Choosing a Lifetime Annuity

Should you choose the lifetime payout option when you’re annuitizing your annuity? It depends. Here are some of the pros and cons.

Advantages include the following:

- Guaranteed lifetime income. A lifetime annuity ensures that you receive payments for as long as you live, providing financial stability. You’ll feel more confident with your financial circumstances if you know you have annuity income to bolster your social security benefits or pension income.

- Mitigation of longevity risk. Lifetime annuities reduce the risk of outliving your retirement savings, which is a significant concern for many retirees.

- Protected against market volatility. Annuities can offer a shield from market volatility, as your payments are guaranteed and aren't directly exposed to market fluctuations.

However, there are also some potential drawbacks, such as:

- Payments stop at death. Your annuity payments stop when you die, regardless of how much money the contract has paid out. If you have remaining funds in your annuity account when you die, the annuity company usually keeps it.

- Lack of liquidity. Once you’ve annuitized and chosen the lifetime payout option, you can’t easily access your funds. You have to wait until they’re paid back to you.

- Inflation risk. Most annuity payments do not adjust with inflation. That means the purchasing power of your annuity payments could erode over time.

Key Factors to Consider When Choosing a Lifetime Annuity

Choosing a lifetime annuity payout option can significantly impact your financial well-being in retirement. Here are some key factors you should consider before making the choice:

- Payout value and length. Lifetime annuity payout options are usually lower than if you choose a period-certain payout option. On the other hand, they could last longer. Consider whether you prefer larger payments for potentially less time or smaller payments over a potentially longer period of time.

- Health and life expectancy. Consider your current health status and family history. If you are in good health and have a family history of longevity, a lifetime annuity may be a good option because it will continue to pay you for as long as you live.

- Spousal or survivor benefits. If you want your spouse or another person to continue receiving income after your death, you can choose a joint-and-survivor annuity. However, this option usually results in a lower monthly payment than a single-life annuity.

- Financial stability of the insurer. An annuity is a promise by the insurance company to pay you an income in the future. It's important to consider the financial strength of the insurance company selling the annuity because this will affect their ability to meet those promises.

- Liquidity needs. Annuities are usually illiquid. Once you annuitize, you usually cannot get your money back except by waiting for your income payments. If you anticipate needing access to your funds in the case of emergencies or unexpected expenses, the lifetime payout option may not be ideal for you.

- Tax considerations. Annuity payouts are typically subject to tax in the year you receive the payouts. Lifetime income payouts spread out your payments so you typically pay less taxes in any given year.

As with any financial decision, it's usually a good idea to speak with a qualified financial advisor before choosing an annuity payout option. They can help you evaluate your personal financial situation, goals, and risk tolerance to make the best choice for you.

Making the Choice: Is a Lifetime Annuity Right for You?

Whether a lifetime annuity payout option is right for you depends on your individual circumstances, financial goals, and risk tolerance.

It’s ideal for anyone who wants a low-risk way to secure an income in retirement. It may not be as good if you prefer to receive your income all at once or over a certain period of time.

Canvas Annuity offers a lifetime payout option on all annuity products. Our fixed annuities give you a safe place to grow your money. When you’re ready, you can annuitize and choose a lifetime payout option.

Learn more about Canvas’ annuity products and annuity rates, or apply today.

Resource Hub