Updated: March 7, 2024

Who Assumes the Investment Risk With a Fixed Annuity Contract?

When you purchase a fixed annuity as part of your overall retirement strategy, the issuing insurance company offers you a guaranteed rate for a specific period of time that you choose. The good news is that the company assumes the investment risk while you are guaranteed to receive the rate of return stipulated in the contract.

While there are a few types of annuities, a fixed annuity is the most conservative choice for savvy investors looking to create a foundation for retirement income.

Unlike variable and fixed-indexed annuities, fixed annuities do not require you to select the underlying investments that support the interest rate you receive. The insurance company invests your money, usually in bonds and other investments, and makes money from the difference between their investment returns and the rate you are credited for your annuity.

How Does the Insurance Company Manage Risk?

In general, life insurance companies are conservative investors.

A combination of regulatory oversight and a discipline of closely matching investment maturities with obligations like annuities and life insurance contracts keeps these companies keenly focused on managing investment risk.

The goal is to balance risk and reward while ensuring the company can fulfill its financial commitments. The investment types typically include:

- Fixed-Income Investments: These low-risk vehicles include government bonds, corporate bonds, and municipal bonds. They provide a steady stream of income and help insurers meet their guaranteed payouts to policyholders.

- Real Estate: Companies may invest in real estate properties and real estate investment trusts (REITs) to diversify their portfolios and generate capital appreciation.

- Mortgages: Insurance companies often invest in mortgages or mortgage-backed securities, including residential and commercial mortgages, to earn interest income. These investments are typically secured by the underlying properties.

- Loans and Other Debt Instruments: Life insurers may invest in various forms of loans and debt instruments, including corporate loans, structured finance products, and collateralized debt obligations.

- Cash and Cash Equivalents: To maintain liquidity and cover policyholder withdrawals, insurance companies hold a portion of their portfolios in cash and cash equivalents, like money market funds.

So what does this mean for you?

Diversifying investment types allows insurance companies to offer competitive rates to fixed annuity clients. These investments and risk mitigations help them do that while maintaining a spread that helps run the insurance sales and operations functions of the company.

It also helps provide a return to investors (if it is a stock company) and/or pay dividends back to policyholders.

Safety of Fixed Annuities Relative to Other Retirement Products

Fixed annuities are among the safest tools to help build guaranteed returns prior to retirement and lock in a series of payments once you retire.

There are two phases to a fixed annuity. The first is the accumulation phase. During this phase, the rate offered is fixed and will not change for the duration of the guarantee period that you choose (typically 3, 5 or 7 years in duration).

While there are other conservative accumulation tools like CDs and savings accounts, fixed annuities allow your gains to be tax-deferred until you take distributions.

CDs and savings accounts require you to pay taxes on any gains for the year they are received. Riskier investments like mutual funds, stocks, bonds, and variable annuities can also play a role in a well-rounded accumulation portfolio but do not provide the stable returns of fixed annuities.

The second phase of an annuity is the distribution or annuitization phase. During this phase, you create a guaranteed series of monthly payments that can create a solid foundation for your retirement income plan.

No other financial product can provide this level of guarantee.

Because the insurer bears the responsibility for investing, you want to make sure to choose a company with a strong financial balance sheet. Rating agencies take a look at many variables when providing "claims-paying ability" ratings for insurance companies.

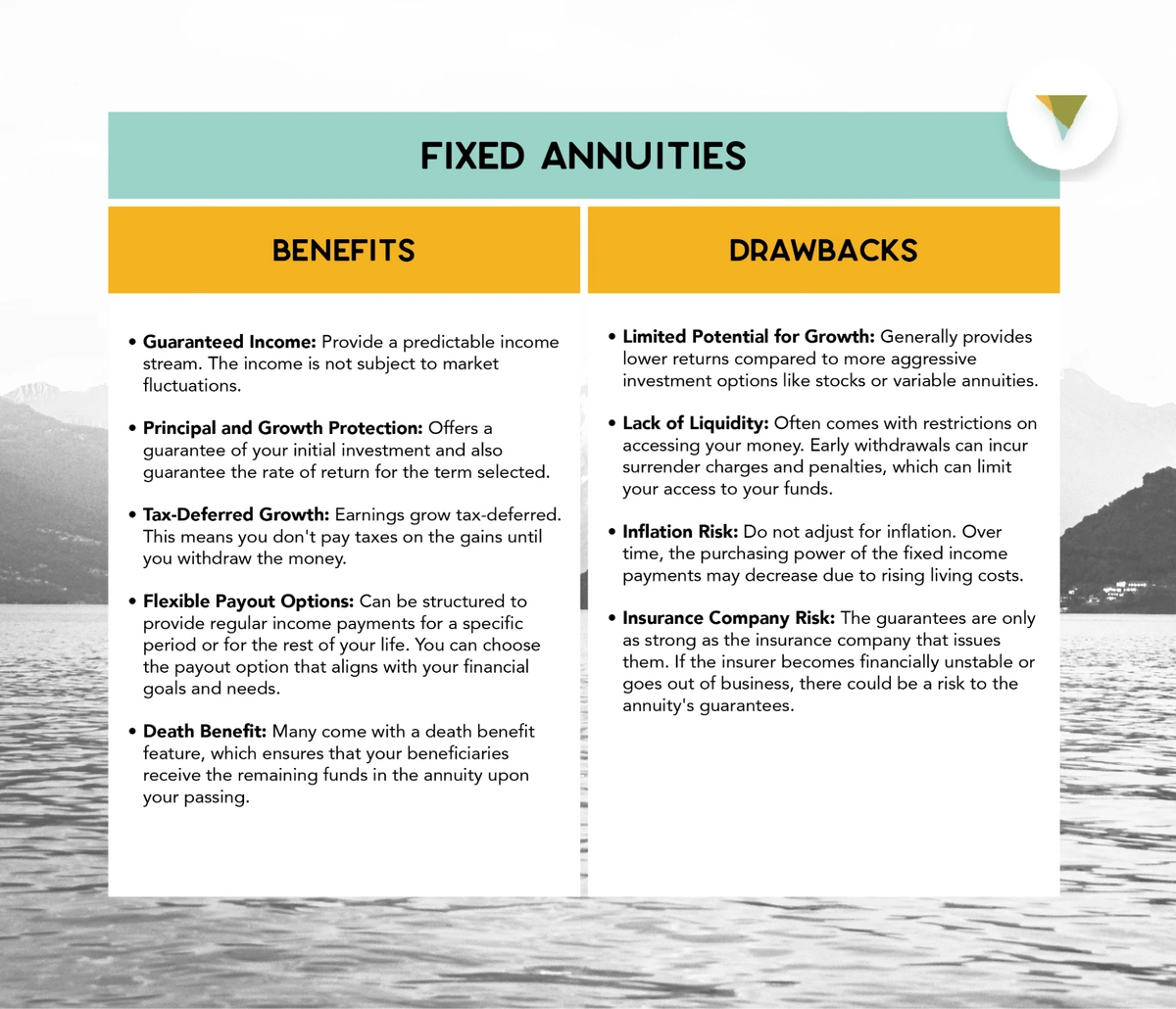

Benefits and Limitations of Fixed Annuities

Like any financial product, fixed annuities may not be for everyone. Here are the core benefits and drawbacks:

Primary Benefits

- Guaranteed Income: Fixed annuities provide a predictable income stream, which can be a valuable source of financial security in retirement. The income is not subject to market fluctuations.

- Principal and Growth Protection: Fixed annuities offer a guarantee of your initial investment (principal) and also guarantee the rate of return for the term selected. This makes them a relatively low-risk option that typically provides better returns than traditional savings accounts or CDs

- Tax-Deferred Growth: Earnings in a fixed annuity grow tax-deferred. This means you don't pay taxes on the gains until you withdraw the money, allowing your money to grow more quickly.

- Flexible Payout Options: Fixed annuities can be structured to provide regular income payments for a specific period or for the rest of your life. You can choose the payout option that aligns with your financial goals and needs.

- Death Benefit: Many fixed annuities come with a death benefit feature, which ensures that your beneficiaries receive the remaining funds in the annuity upon your passing.

Primary Drawbacks

- Limited Potential for Growth: While fixed annuities offer safety and stability, they generally provide lower returns compared to more aggressive investment options like stocks or variable annuities.

- Lack of Liquidity: Like most annuities, fixed annuities often come with restrictions on accessing your money. Early withdrawals can incur surrender charges and penalties, which can limit your access to your funds.

- Inflation Risk: Fixed annuities do not adjust for inflation. Over time, the purchasing power of the fixed income payments may decrease due to rising living costs.

- Insurance Company Risk: The guarantees in a fixed annuity are only as strong as the insurance company that issues them. If the insurer becomes financially unstable or goes out of business, there could be a risk to the annuity's guarantees.

Because fixed annuities may not be the appropriate product for everyone, it's a good idea to understand the terms and conditions before purchasing.

Final Thoughts

When buying a financial product, it is important to know the risks.

One risk is investment risk. With most products like stocks, bonds, and variable annuities, you, the buyer, select the investments and assume the risk.

With fixed annuities, insurance companies take the guesswork out of buying by offering you a rate of return while taking on all the risk.

Canvas Annuity’s products feature some of the most competitive, risk-free rates in the country. And you can purchase online or right over the phone without the need to meet with an agent. Take a look at Canvas’ annuity rates and consider a risk-free purchase today.

Resource Hub