Updated: March 7, 2024

Annuities in Connecticut: A Guide for Annuity Beginners

Connecticut residents who want to add an annuity to their retirement plan have many options.

Annuities are for sale in Connecticut via life insurance agents, financial advisors, and, in the case of the newest entrant in the state, Canvas Annuity, direct from the company.

With all of your options, one thing always holds true. It is important to explore options based on your unique goals. Whether you’re buying through an agent or direct from an annuity company, finding the right tool for you is key.

While annuities for sale in Connecticut have basically the same features and benefits as those available in other states, there are some unique attributes to consider.

A good place to start is with the state insurance department (see below), but some of their guidance may be confusing for people new to annuities. That’s why we made this guide to give Connecticut residents a firm foundation to explore their options.

Connecticut's Tax Treatment of Annuities

Each state treats annuities differently when it comes to taxes. Here’s what you should know about the way taxes on annuities work in Connecticut.

State Income Tax

State income taxes range from 3% to 6.99%, depending on filing status and income.

The good news is that Connecticut currently exempts all pension and annuity earnings from the state income tax — but only for individuals whose overall income from all sources is less than $75,000 per year.

For married couples, retirement earnings are totally exempt if the household’s overall income is less than $100,000. If your income exceeds these limits, even by $1, the exception becomes void.

There is a bill pending this year (2023) that proposes to adjust these exceptions to be less punitive.

For example, with the proposed rules, a single filer with a total income below $75,000 still would receive a full exemption. Those whose income exceeds $75,000 would receive a partial exemption, which would shrink gradually as income increases and vanish entirely for filers topping $100,000.

Similarly, couples would continue to get the full exemption if their total income is below $100,000 but also would get a partial tax break if their income falls between $100,000 and $150,000.

Early Withdrawal Tax Treatment

Connecticut does not assess any premium taxes and does not charge any additional tax for early withdrawals from your annuity.

However, the issuing annuity company may charge surrender fees for early withdrawals. Also, the Internal Revenue Service (IRS) may assess a premature withdrawal penalty of 10% and charge income tax on the withdrawn funds.

The amount of the surrender charge depends on how long you stay in the contract. The penalty for early withdrawal depends on your age and the circumstances for making the withdrawal.

Annuity Laws and Regulations in Connecticut

The Connecticut Insurance Department's focus is on advocating for consumers of insurance and related products like annuities.

To accomplish this, they monitor insurance companies’ financial stability and ensure they follow the state's laws and treat consumers fairly.

They offer guidance, support, and education for consumers and regulate the industry in a way that promotes fair competition and makes sure insurance is available to everyone.

Rules for Protecting Your Money

The Connecticut Life and Health Insurance Guaranty Association (the guaranty association) is composed of all insurers licensed to sell life insurance, accident and health insurance, and individual annuities in the state of Connecticut.

In the event that a company member of the association is found to be insolvent and is ordered to be liquidated by a court, the Guaranty Association Act enables the guaranty association to provide protection (up to the limits spelled out in the Act) to Connecticut residents who are holders of individual annuities.

Agent Licensing Requirements

For an individual to sell life insurance and annuity products in Connecticut, they are required to take a pre-licensing course before taking the Producer Licensing Exam.

Connecticut requires 40 hours of pre-licensing education courses. A pre-license education course provides very specific industry knowledge that will be tested during the exam.

Beyond helping agents prepare for and pass the life insurance licensing exam, a pre-license education course gives prospective agents a solid understanding of the duties of a life insurance agent.

Once an agent passes the test, they can apply for a producer's license. The application is received by a national producer registry known as the National Insurance Producer Registry (NIPR).

Buying an Annuity in Connecticut

Like most Americans, people in Connecticut generally buy annuities for two reasons — they want to grow money on a tax-deferred basis before retirement, or they want to create a guaranteed flow of income in retirement.

Accumulation

The accumulation phase starts when you buy an annuity. It’s the period of time during which your annuity earns interest and grows prior to retirement. Annuities can be a valuable part of a retirement savings plan, especially fixed annuities, the most conservative type.

In this phase, the money in your account earns interest, and the interest crediting rate is determined by the type of annuity you have (explained below). Your money accumulates on a tax-deferred basis.

Some annuities, called immediate annuities, skip the accumulation phase. They start to pay you back immediately or soon after you pay your premiums.

Distribution/Annuitization

Your money continues to earn interest and grow until you annuitize it. When you annuitize, you end the accumulation period and start receiving regular income payouts. This is called the annuitization period or payout phase.

When you annuitize, you’ll choose between different payout options, like how often you want your income payouts, how long you want your income payments to last, and whether you want to add a joint annuitant.

For example, you might choose monthly payments for the rest of your life. Or, you might choose to receive monthly payments for a specified period, like 10 years. In the first option, each payout would be much lower than the payouts in the second option.

Steps to Consider When Buying an Annuity in Connecticut

Before buying an annuity, there are a handful of things to consider:

- The goal of the purchase: Accumulate money or create a stream of income.

- Your comfort with risk: Annuities come in a few varieties based on your appetite for risk. Fixed annuities are the most conservative type, followed by fixed-indexed and variable annuities.

- The financial strength of the issuing insurance company: The life insurance companies that issue annuities receive financial strength ratings from a few notable rating agencies, including A.M. Best, Fitch, and others. It's a good idea to research the company that is issuing your annuity and make sure they have a "good" rating from these agencies.

- Fees associated with the annuity: There are some annuity fees to be aware of, regardless of the type of annuity you are considering.

- Death benefit provisions: Most annuities feature a standard death benefit. This feature lets you pass on assets from the annuity heirs after your death. The feature may also appear as an optional annuity rider and may have a cost related to it.

Types of Annuities Available in Connecticut

Most companies that have products available in Connecticut can offer deferred and immediate annuities (for both the accumulation and distribution phase) as well as three general varieties based on your risk appetite:

Fixed annuities: Fixed annuities offer a fixed rate of return guaranteed by the insurance company for specific periods of time. People sometimes buy a fixed annuity to provide a solid foundation for their retirement plan since rates are locked in for the period of time you choose, usually 3, 5, or 7 years.

Fixed-indexed annuities: These products share features of fixed and variable annuities. Fixed-indexed annuities offer a guaranteed floor rate (usually 0% so you won’t lose money) and a rate "ceiling" as well. They offer more accumulation potential versus fixed annuities. You choose an investment “index” (like the S&P 500) which drives your returns.

Variable annuities: This is the most volatile type of annuity but also offers the largest accumulation "upside" because returns are linked to stock market funds that you choose. Unfortunately, they can be difficult to understand, have no "floor" (you can lose money), and usually have lots of management and other fees that the insurance company charges.

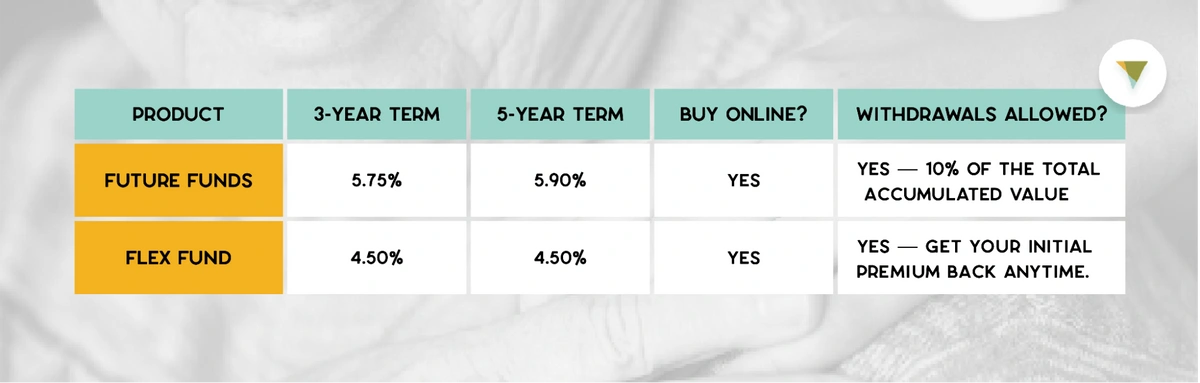

Connecticut Fixed Annuity Rates

One of the most important factors when choosing an annuity is the interest rate. Higher interest rates mean your annuity account grows faster.

Here are the three-year and five-year rates for fixed annuity products offered by Canvas Annuity.

Final Thoughts

When buying an annuity in Connecticut, you have a lot of choices. The best product to buy depends on what your goals are (accumulating money or creating a stream of income that you can't outlive) as well as your risk tolerance.

Fortunately for Connecticut residents, fixed annuities from Canvas Annuity are now available for sale. Canvas offers some of the most competitive fixed annuity rates in the country, and you can buy right over the phone or on your own from the company's website.

Resource Hub