Updated: March 7, 2024

Are Annuities A Good Investment? (When Are Annuities A Good Idea?)

Many people are confused about annuities. In fact, according to a recent Secure Retirement Institute (SRI) study, only 25% of consumers scored a passing grade (70%) on an annuity knowledge questionnaire.

With all of this confusion surrounding annuities, it can be hard to determine if they are a good investment and deserve a place in your retirement account. But we’re here to make it simple.

An annuity contract provides long-term guaranteed retirement income. Its main goal is to help you address the risk of outliving your savings.

Most people don't understand this key feature: They can provide you with the funds to retire comfortably. Because of the guaranteed income feature, these products can be an integral part of your retirement planning. So, what do you need to know about annuities to decide if these personal financial products are a good investment for your retirement?

And how do they compare to other investment options, like the stock market, bonds, CDs, and mutual funds? We’ve got your answers.

We’re covering what annuities are, their pros and cons, and alternatives. Once you have a solid understanding of what annuities are—and what they are not—you’ll be able to determine if they deserve a place in your retirement planning journey.

What Are Annuities?

Annuities are personal finance products issued by insurance companies. You provide the funds to the insurer now (either in a lump sum or through monthly payments), the money gains interest, and you receive payouts as dictated by your contract.

Unlike 401(k)s or non-annuity IRAs, annuities can give you a fixed stream of income that can last the rest of your life.

This is why annuities can be a good choice for retirement.

Annuity Pros and Cons

Annuities offer a unique way to grow your retirement savings and provide retirement income.

They are becoming more and more popular because of this fact.

But as you evaluate whether or not an annuity is a good investment option for you, you must also be aware of its disadvantages.

The Pros of an Annuity

- Multiple interest rate options depending on your risk tolerance (fixed, fixed indexed, and variable annuities)

- Generally less volatile than stocks

- Available to help retirees accumulate money or distribute money in retirement

- Some companies, like Canvas Annuity, offer a simple annuity product with an easy, online application process.

- They allow you to conduct the entire transaction online without going through an insurance agent

- Can provide guaranteed income for life

The Cons of an Annuity

- Most annuity products must be purchased from insurance agents or financial advisors

- Can have surrender charges, management fees, or commissions that reduce your returns

- They are generally long-term products, meaning you know you won’t need the money for a while (vs CDs or savings accounts)

Types of Annuities

Now that you understand the pros and cons of annuities, it’s time to evaluate the different types. There are several types of annuities, depending on when and how you want to use them.

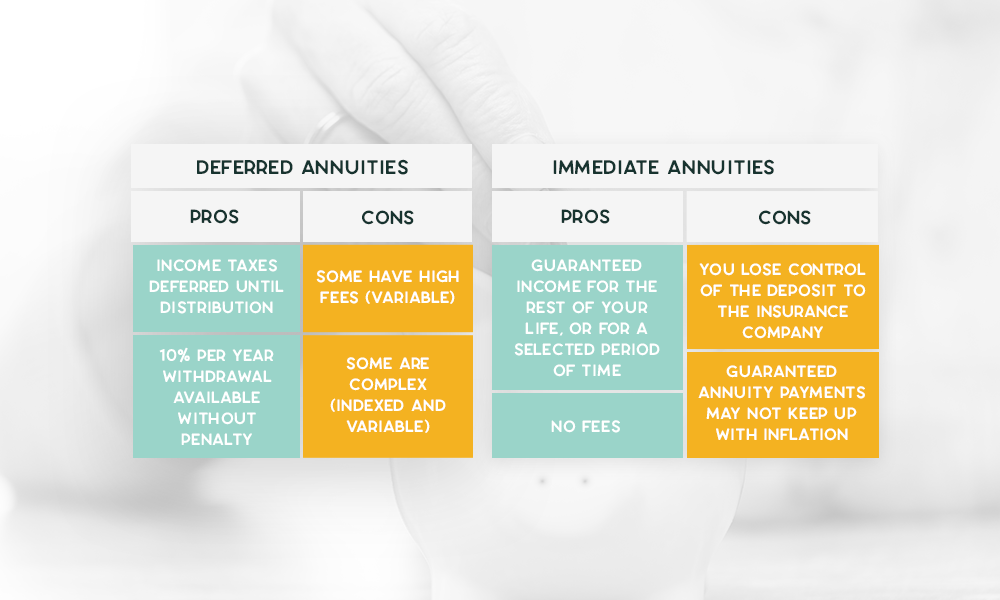

Deferred Annuities vs Immediate Annuities

For those who do not currently need income, there are deferred annuities. A deferred annuity just means that you are biding your time, taking advantage of competitive interest rates, and letting your money grow tax-deferred until you need payouts.

This is known as the accumulation phase. When it's time to receive your payouts (usually in retirement), it's known as the annuitization phase.

For those who need a guaranteed source of retirement income right now, there are immediate annuities.

Immediate annuities give you a choice of payout options and can provide significant peace of mind.

They’re best for people who need monthly income to supplement social security. They also benefit those who need additional retirement income to cover healthcare, utilities, and other retirement expenses. With immediate annuities, there is no accumulation phase. You pay a lump sum and almost immediately enter the annuitization phase.

Fixed Annuities vs Fixed-Indexed vs Variable Annuities

Within deferred and immediate annuities, there are fixed, fixed indexed, and variable options.

Each name simply indicates the product’s investment style (i.e. how your money will grow).

Fixed annuities provide conservative, guaranteed returns (with low risk), variable annuities provide the most potential for growth (with high risk), and fixed indexed annuities lie somewhere in the middle.

Let's take a closer look at the different types of plans to determine if these investment vehicles might be a good choice as part of your overall retirement plan.

With a fixed annuity, your plan has a fixed interest rate for a specific period of time (typically three, five, or seven years).

This means your annuity will grow at a steady rate, ensuring a guaranteed rate of return. This can be especially helpful for financial planning because you can predict how much money it will earn.

A fixed indexed annuity lets you determine your annuity’s interest rate by choosing specific markets its gains will be linked to.

Better market performance means more earnings. But low market performance means fewer earnings or no earnings.

These products typically have a guaranteed minimum rate of return.

With a variable annuity, you invest your annuity into certain investment options (typically stock mutual funds). The performance of these investment options determines your earnings.

It is advisable to work with a financial planner when buying variable annuities, as they tend to be complex insurance products and if the performance of the investment option chosen is poor, you can lose the money you invested.

Alternatives to Annuities

When planning for retirement, there are a lot of roads you can take. An annuity is a great path that has specific attributes (like tax-deferred growth and guaranteed lifetime income) that can help you secure a comfortable retirement.

But, like a great orchestra, a well-diversified retirement portfolio should consist of many financial instruments. Let’s take a look at some of the most common investment options. (Or you can read our full guide on Annuitiy Alternatives here)

Certificates of Deposit (CDs)

Certificates of Deposit (CDs) are similar to annuities in that they are very low-risk. Most CDs provide a guaranteed minimum interest rate.

One difference between CDs and fixed annuities is how they’re taxed. The IRS typically taxes earnings from CDs as capital gains. In contrast, you pay ordinary income tax on annuity payments. Also, CD income is taxed in the year it is earned, even if the money remains in the CD. Alternatively, annuities have the benefit of tax deferral so you won’t pay taxes on your earnings until you make a withdrawal.

Compared to CDs, annuities tend to hold the advantage. However, the upside to CDs is that they are available for short- and medium-length terms. That makes them a potentially better choice for investors looking to grow their money over a shorter time frame.

401(k)s

A 401(k) is a retirement plan sponsored by your employer. They deduct a portion of your paycheck every month and put it towards your chosen investments. They may even contribute to your fund themselves.

401(k)s are different from annuities. They're tied to your employer, so if your employer doesn't offer a 401(k), you may be out of luck. They also have limits on how much you can contribute. That's not great if you want to build up significant retirement savings. Also, your earnings are tied to the performance of your chosen assets. Depending on your portfolio and stock market performance, you could earn very little—or even lose money.

In contrast, annuities are not tied to an employer—they're available to everyone. Also, there are no contribution limits. And if you buy a fixed annuity, you'll receive steady earnings with a guaranteed minimum crediting rate.

IRAs

Individual retirement accounts (IRAs) are sometimes confused with annuities, but they’re not the same thing.

IRAs are not actually a financial or investment product. They're just an account that holds retirement savings and investments. They can hold stocks, bonds, mutual funds, and even annuities.

Because these accounts are for retirement savings, the IRS gives them several tax advantages. However, there are also rules. The IRS dictates what you can invest your money in, how much you can contribute, and when you must withdraw your money by.

One downside of IRAs is the contribution limits. Annuities do not have this same restriction.

IRAs also do not provide a guaranteed minimum interest rate like fixed annuities can. And they can't provide a guaranteed income in retirement.

IRAs are great for investors who want a tax-advantaged place to hold their retirement savings and investments. Annuities are better for people who want to ensure their retirement savings grow or for those who want a steady retirement income.

Stock Mutual Funds

Stock mutual funds allow you to invest in stocks without the risk of choosing individual stock holdings.

Professional money managers take care of choosing the stocks in each mutual fund and generally choose a diverse group of holdings to maximize the interest rate return. Mutual funds can lose money, and unlike annuities, do not have a minimum guaranteed rate of return.

They also charge annual fees called “loads,” which most annuities do not.

Stocks

Stocks can be a valuable part of a well-balanced retirement strategy due to the high potential for growth (the stock market has averaged a 10% return since 1976). You research and choose your own stocks and can invest directly through public platforms like TD Ameritrade and Schwab. When you buy a stock, you are actually becoming a part owner of the company.

But buying stocks can be time consuming and risky. There are no provisions for safety like minimum returns and the safety of state guarantee associations.

Social Security

Social security is a government program that provides supplemental income to some retirees. It’s a useful assistance program, but the keyword is “assistance.” Most people do not plan to rely only on social security in retirement

First of all, not everyone is eligible for social security. Also, most people receive only about 40% of their pre-retirement income. That amount may not be enough to support you through retirement.

Many retirees have additional savings to maintain their quality of life through retirement. An annuity can provide supplemental income over and above your social security check.

Is an Annuity a Good Retirement Investment Option?

Annuities can be a powerful addition to your portfolio because they provide a guaranteed income stream in retirement. This is something no other retirement product can offer. In the case of a low-risk fixed annuity, they can help balance out the riskier investments you may hold.

Most people don’t just have one retirement product; they diversify their retirement savings. They may have a pension, an IRA, and a 401(k) in addition to their savings. They may also have a separate portfolio of investments.

When Are They a Good Idea for Retirement?

An annuity could be the right product for you is:

- You're planning for retirement and you want a very low-risk way to steadily grow your savings.

- You're in retirement and you want to safely earn interest on your nest egg.

- You want to supplement your other income sources with additional retirement income.

- You want to invest over the long term.

Hopefully, now you’re better armed to decide if an annuity would be a good investment as part of your overall investment portfolio.

Most financial advisors suggest that people near or in retirement build an investment portfolio that is well-diversified. And annuities certainly can play a role as part of this diversification.

When traditional savings vehicles offer very low rates, buying a fixed deferred annuity can be a solid alternative. Canvas Annuity, for instance, is currently offering rates around 3% per year, guaranteed for 5 or 7 years! Further, if you are making a retirement plan and are interested in a guaranteed income stream, then an annuity could be a good investment option for you.

An immediate annuity is the only personal finance product that guarantees lifetime income via a series of payments directly to you!

At Canvas, our annuities are designed to be simple, straightforward, and people-first. We offer fixed annuities with a guaranteed rate of return that you fund with a single premium through qualified or non-qualified funds.

Canvas annuities are backed by the Puritan Life Insurance Company of America, a company rated B++ by A.M. Best. With penalty-free withdrawals for qualifying medical emergencies and partial withdrawals up to 10% of your account value, our annuities are flexible, helping you deal with life when it happens. And the best part?

You can buy our annuities directly online, meaning you don't have to work with an agent. Taking out the middleman gives our annuity products highly competitive interest rates—not to mention no commission, account, or annual fees. Ready to get started?

See which Canvas annuity is right for you, and we can help you get it up and running today.

Citations

1. Deloitte, “Voice of the Annuities Customer,” Freeman, Canaan, Gokhale, 2015. Voice of the Annuities Consumer

2. LIMRA, “Knowledge Matters -- The Impact of Financial Knowledge on the Annuity Perceptions of Consumers,” Morales, Shiner, 2020. Secure Retirement Institute Study: Most Consumers Baffled By Annuities

3. The Nest, “Which is Better, CD or Annuity,” Joseph, 2020. Which is Better, CD or Annuity?

4. Bankrate, “The pros and cons of CD investing,” Dixon, 2021. The pros and cons of CD investing

5. The Balance, “The Pros and Cons of Stock Mutual Funds,” Thune 2021. Here Is a Look at the Pros and Cons of Investing in Stock Mutual Funds

6. Zacks, “The Advantages and Disadvantages of Investing in the Stock Market With Personal Finances,” (Johnson 2019). The Advantages and Disadvantages of Investing in the Stock Market With Personal Finances

Resource Hub