Updated: March 7, 2024

What is an Annuity Statement? How Do You Read One?

Annuities are great products for accumulating money prior to retirement, then creating a guaranteed stream of income once you retire. The insurance company that issues your annuity provides you with an annuity policy statement that tracks the performance of your annuity and provides other valuable information.

Reading your annuity statement isn’t hard, but it can be confusing if you’ve never seen one before.

Here’s how you can make sense of each statement your annuity company sends you.

What is an Annuity Statement?

Let's face it, many of us receive statements from our financial accounts and just file them without reviewing the details.

But if you own an annuity, you will want to spend a little time reviewing the specific components of the statement since annuities can make up a substantial piece of your retirement nest egg.

These documents provide you with details such as money balances, growth or loss of your principal, cash values, and penalty-free withdrawal options. In variable and fixed-indexed, they also show investment details.

Your statement will also detail any activity that has occurred within your annuity account, like interest rate changes and rate cap details (for fixed-indexed annuities).

When you purchase an annuity, you receive these statements either annually (if you own a fixed annuity) or quarterly (if you own a variable or fixed-indexed annuity). These quarterly statements show the growth or loss of your annuity value based on the investment subaccounts that are the basis for growth or loss.

Important Parts of an Annuity Statement

Most annuity statements feature components such as:

- Identification information

- Contract details

- Interest rate credited

- Transactions

- Tax qualification

- Surrender value

- Death benefit value

- Lifetime income value

Let's take a look at some of the most important sections of an annuity statement in detail.

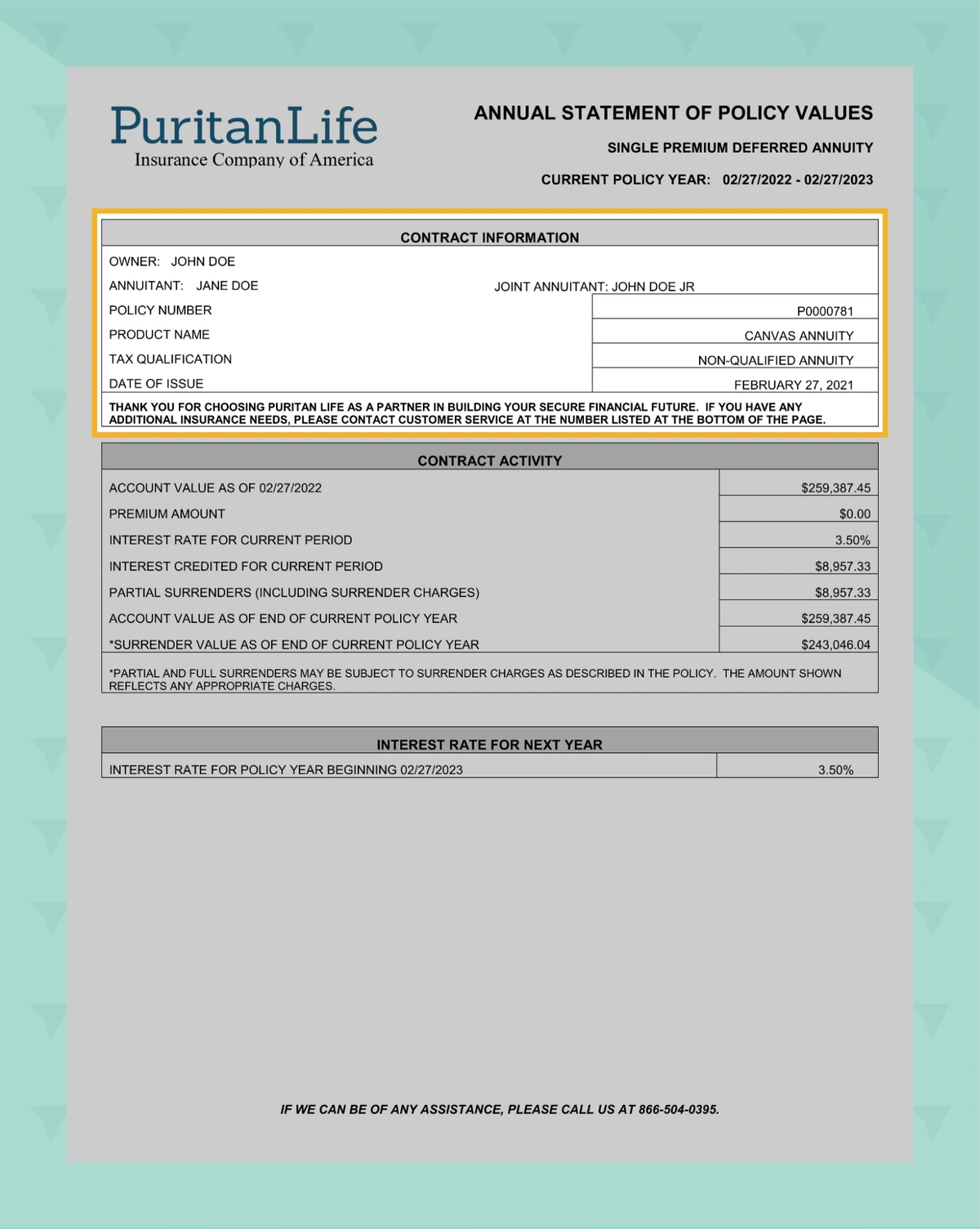

Contract Information and Overview

This section usually appears at the top of your statement and includes information such as your name and address, as well as specific contract information, which typically includes policy number, type of annuity, product name, and the date your annuity was issued.

The statement period (dates reflected in the statement) is also listed here. This section may also include the tax status of the annuity, reflected as "qualified" or "non-qualified."

This information is important to know, especially if you are contacting the company with questions.

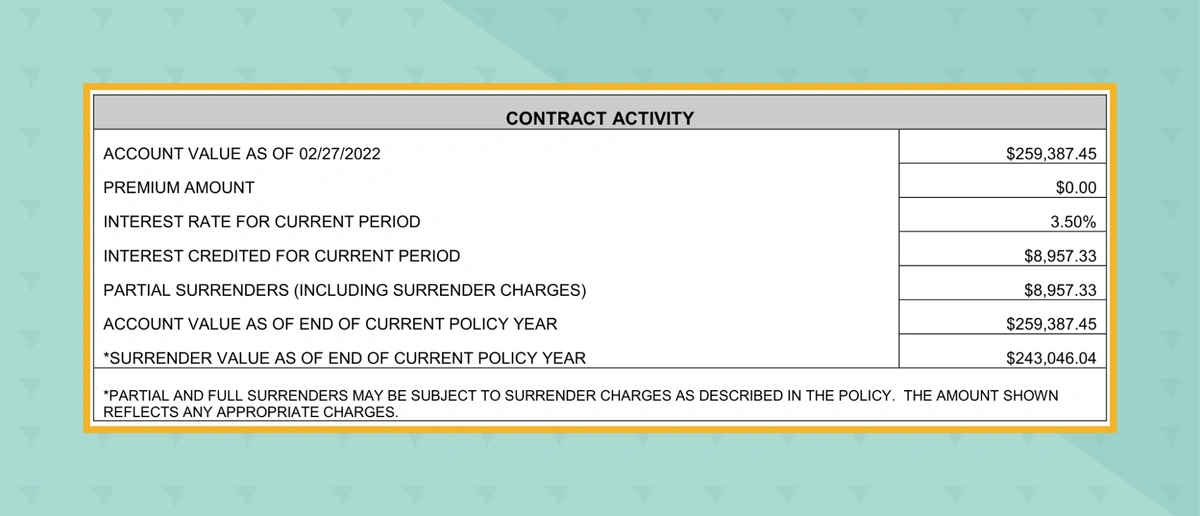

Contract Balances and Activity

One of the most important areas of your statement, the Contract Activity section, should show your initial annuity deposit amount, as well as the current interest rate for the term selected (for fixed annuities) or the interest rate credited for a specific time period (for fixed-indexed and variable annuities).

It will also show the amount of the gain or loss for a specific period, the current balance (account value), and what the balance would be if you surrendered the policy (the net amount after any surrender charges).

It may also include details such as contributions or premiums paid, withdrawals or distributions taken, any fees or charges incurred, and adjustments made to the account. Death benefit values, if applicable, will also appear in this section.

If it is an annual statement (usually for fixed annuities), it will also show the guaranteed rate for the upcoming year.

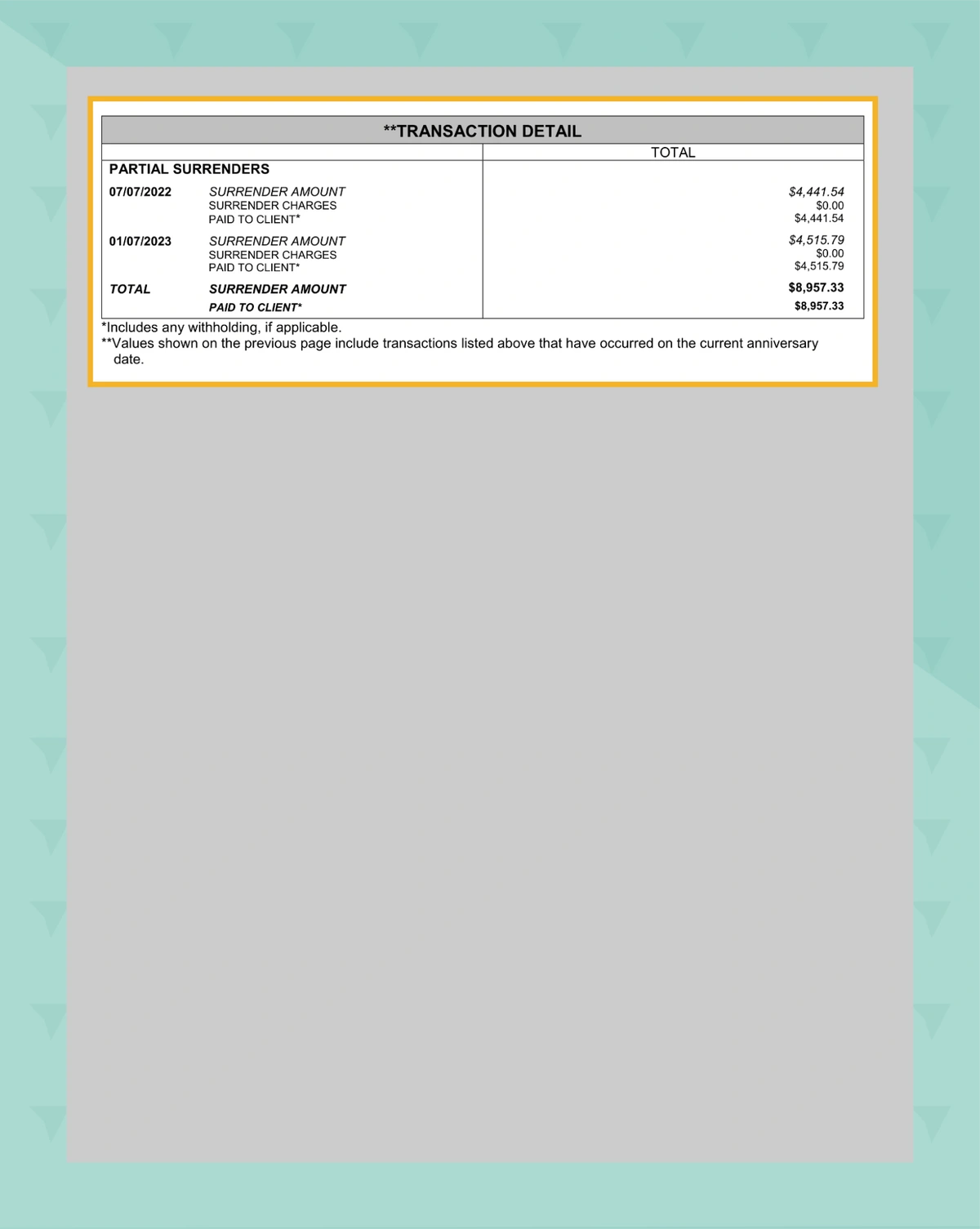

Transaction Detail

If you have had any deposit or withdrawal activity during the statement period, it will be reflected in the Transactions section.

Specific activity includes surrender activity (annuity withdrawals) and any penalties if warranted.

Privacy Notice

An annuity statement should include the company's privacy statement, which outlines the policies that guide the use of your personal information.

Read this section carefully and make sure you are comfortable with who and when your information is shared.

How to Read and Understand an Annuity Statement

There are a few critical areas of your statement that provide information regarding your money, including gains or losses and current balances.

Reading and understanding this statement is one of the most important actions you can take to truly understand your annuity.

Investment Performance — "Performance" shows how your annuity balance either has grown or declined during the statement period. For annuities linked to investment options (fixed-indexed or variable annuities), this section provides a breakdown of the performance of each investment option within your annuity. It typically includes information such as the investment account name, stock ticker symbol (if applicable), the current unit or share value, the number of units or shares owned, and the total value of the investment. With fixed annuities, this section will be very simple, reflecting the guaranteed interest rate credited for the period.

Fees and Charges — This section outlines the fees and charges associated with your annuity contract. It may include information about annual contract fees, mortality and expense charges, administrative fees, investment management fees, and any other applicable charges. This section helps you better understand the costs associated with your contract. Fees are usually associated with fixed-indexed and variable annuities. These charges can take a real bite out of your contract values. Be sure to ask your advisor if you have any questions regarding fees.

Once you have a better understanding of the components of your annuity statement, especially performance, returns, and balances, it is easier to make a decision on whether to continue holding the annuity or consider switching to another product.

Remember that annuities are long-term financial products and come with fees for surrendering all or part of your annuity prior to the end of the surrender period.

Also, know that one of the primary reasons to own an annuity is to eventually use the product to create guaranteed income in retirement. It is the only financial product available that fits this role in your post-retirement planning.

Final Thoughts

Any financial account statement you receive, either on paper or electronically, is worth reviewing and understanding.

Annuity statements are no exception.

You've worked hard to allocate your money to financial vehicles that hopefully will help you live a comfortable retirement. Having a full understanding of how your product is performing and its ultimate contribution to your retirement plan is important. It's always a good idea to consult with a financial advisor if you have any questions regarding your annuity statement and/or your annuity's performance.

If you are looking for a product that provides guaranteed returns (with a simple, straightforward annuity statement), a fixed annuity from Canvas Annuity is a great choice. Canvas offers very competitive returns, and you can make a purchase online or over the phone in minutes.

Resource Hub