Updated: March 7, 2024

Can Annuities be Transferred without Penalties?

Yes, deferred annuities that have not been annuitized can be transferred using the IRS 1035 rule without penalty. Immediate annuities cannot be transferred. Neither can deferred annuities that have been annuitized.

Annuities are a powerful way to prepare yourself for retirement. They offer a way to secure yourself a guaranteed retirement income in addition to social security and pensions. But there are many different types of annuity products, and new ones are popping up every day. What if you become dissatisfied with yours and want to switch?

You might consider an annuity transfer.

An annuity transfer happens when you take one annuity contract and exchange it for one with another company. That new policy might be a better fit for your goals or may be appealing because it provides better interest crediting rates.

Read on to learn everything you need to know about annuity transfers and potential penalties.

What Types of Annuities Can You Transfer?

First, be aware that not every annuity can be transferred.

Deferred annuities can be exchanged, as long as they haven’t been annuitized. In other words, if you have not yet elected to receive a stream of income payment for life, it can be exchanged. If you’ve begun the payout phase and are receiving distributions, it can’t be.

Deferred annuities can be exchanged, regardless of whether they’re fixed annuities, fixed-indexed annuities, or variable annuities.

Immediate annuities can’t be exchanged. Neither can deferred annuities if you have already annuitized them.

Other specific types of annuities that cannot be exchanged include:

- Single premium immediate annuities (SPIAs)

- Longevity annuities

- Qualified longevity annuity contracts (QLACs)

When is Transferring an Annuity a Good Idea?

Transferring an annuity may or may not be a good idea — it depends.

When it’s a Good Idea to Transfer

Fundamentally, transferring is a good idea if the new annuity offers advantages over your older annuity. Here are some examples of when you might want to transfer an annuity.

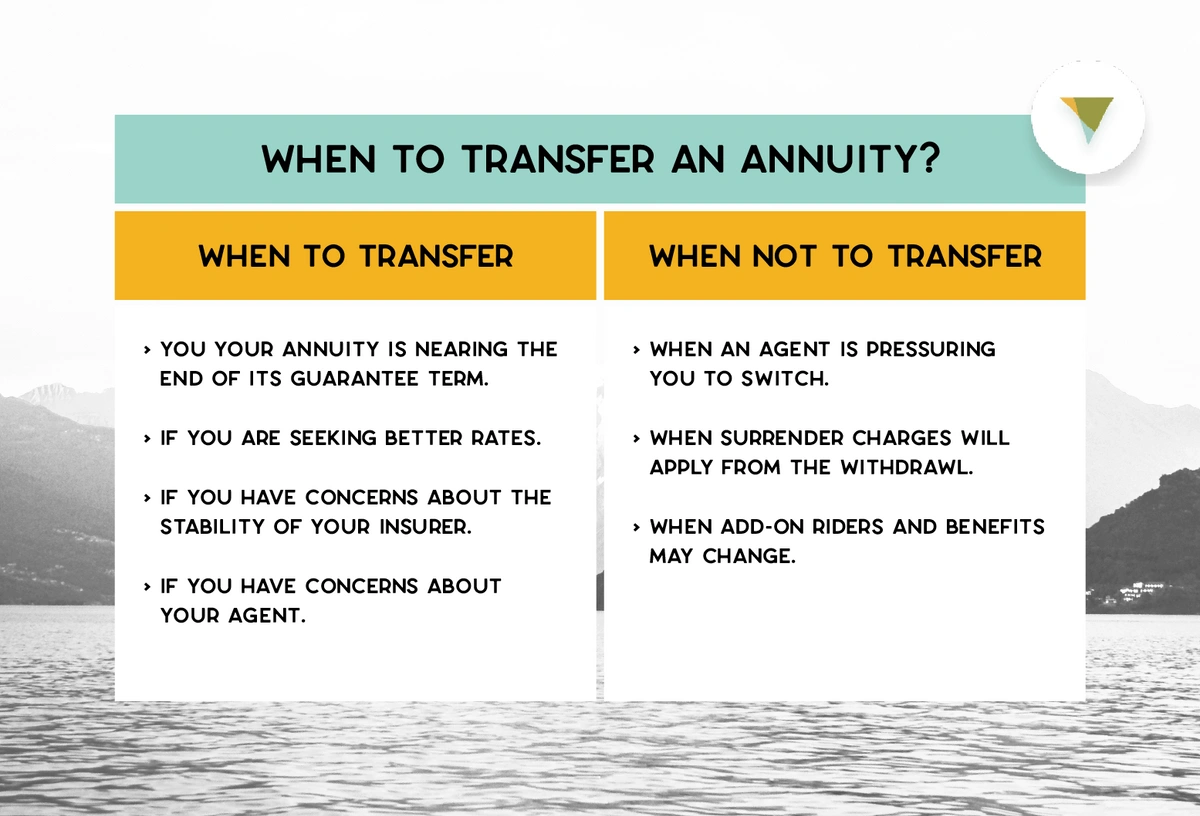

- You have an annuity that’s nearing the end of its guarantee term. You might want to transfer it to a new annuity with a different annuity company that charges lower fees.

- If you are seeking better rates. Annuity companies differ with respect to the interest crediting rates and the types of annuities they offer. If you find an annuity product with better features or better rates than your old one, it might be worth the switch.

- If you have concerns about the financial solvency of your insurer. Annuities provide guaranteed income in retirement, but that guarantee rests on the financial stability of the insurance company. If you begin to have doubts about the financial strength of your annuity provider, it might be a good idea to swap out.

- If you have concerns with your agent. You might also be dissatisfied with the agent that sold you the original policy. In that case, transferring to a new policy may help you feel more comfortable.

When it’s not a Good Idea to Transfer

On the other hand, there are some instances when it may not be ideal to transfer your policy. In some cases, the new company may apply extra fees or first-year expenses to the new policy. So, it’s not always in your favor to switch.

Here are some examples of circumstances in which you may prefer to hold on to your existing policy.

- An agent pressures you to switch. Many annuity agents make hefty commissions on annuity sales. An agent may try to convince you to make a transfer just so they get the commission. Make sure the new policy is good for you and not just the sales agent.

- Surrender charges will apply. If you withdraw money from an annuity early (before the surrender charge period is up) you may have to pay the insurance company surrender charges. Make sure you understand these potential costs before making a switch.

- Riders and benefits may change. You can often customize your annuity contract with various add-on riders and options. When you transfer an annuity, you won’t necessarily have access to all the same options and add-ons. Make sure to understand any differences between your new policy and the old one.

What are the Tax Implications of an Annuity Transfer?

Annuities are tax-deferred products. That means that you don’t owe taxes on annuity earnings in the year that you earn them. Instead, you owe ordinary income taxes on annuity distributions in the year that you receive the distributions.

Because there are tax advantages to your annuity income, there can also be tax implications to making a transfer. For example, if you simply took your money out of the annuity and then put it in another one, you would likely owe taxes.

Fortunately, the Internal Revenue Service (IRS) created the 1035 transfer rule, which allows you to transfer one annuity to another without having to pay tax or any penalties. The reason you don’t have to pay tax is that you do not receive any money. Instead, your money is simply moved from one tax-advantaged annuity product to another.

Can You Transfer an Annuity to an Heir?

In short, yes, you can usually transfer annuities to another person, including a beneficiary. But this kind of transfer is not covered in a 1035 exchange and there are potential tax implications. If you’d like guidance with this kind of transfer, consider consulting with a financial advisor or tax professional for advice.

Transferring a non-qualified annuity is usually fairly simple. You just fill out the insurance company’s paperwork. There may be taxes due at the time of the transfer, and the transfer may affect your estate and gift taxes

Transferring a qualified annuity is a little more complicated because qualified annuities have been funded with pre-tax dollars. It’s a good idea to consult with a tax advisor here to ensure your transfer is conducted as tax-efficiently as possible.

Transferring an annuity to an heir or beneficiary can also be done through death benefits. Note that there are a number of different potential death benefit options, and they have implications for how much money your beneficiary would inherit. Inherited annuities also have a number of specific tax implications to keep in mind.

Final Thoughts

Before making an annuity transfer, really consider whether it’s going to be better for you than keeping the older annuity. Here’s a quick set of guidelines to follow to help you make the call:

- Make sure it’s a good deal. The new annuity should be better than the old one in some way — maybe it has a better interest rate or lower fees.

- Understand the new contract. Every annuity has unique features, like the term, the surrender schedule, etc. Make sure you understand the new contract and how it’s different from the old one.

- Understand any penalties. Double-check that you will not have to pay any surrender charges or tax penalties.

- Keep your original policy details. If you do a 1035 exchange, your new life insurance company will need the details of your old annuity contract. Make sure you hold onto them.

If you currently have an annuity contract and you think there are better options for you, consider a fixed annuity from Canvas Annuity. We offer safe, no-nonsense annuities with great rates.

If you have any questions about how to transfer your annuity to a Canvas annuity, just reach out to a licensed representative.

Resource Hub