Updated: March 7, 2024

What is an Income Annuity and How Do They Work?

An income annuity is an insurance product that you can buy to turn a chunk of retirement savings into a guaranteed income stream. The income can last you for the rest of your life.

Income annuities are designed to solve the big question for most retirees: How do I ensure I have enough money in retirement?

Rather than simply hoping your retirement savings will last you, income annuities create peace of mind by converting your savings into a dependable income check. That way, you’ll know that you’ll have some money coming in.

How exactly do they work? What are the pros and cons? Read on to learn everything you need to know about income annuities.

Is an Income Annuity the Same as an Immediate Annuity?

Yes, income annuities are immediate annuities because they begin to pay you back soon after you fund them — often within a year. Some people also refer to them as immediate payment annuities, or single-premium immediate annuities (SPIAs), when they’re bought with a single lump-sum premium payment.

Income annuities are often contrasted with deferred annuities.

One difference between them is that income annuities annuitize right away. In other words, not only must you convert your annuity account into a stream of income, you have to do it immediately. That means your money doesn’t have time to earn interest and grow before it starts to come back to you as income.

In contrast, deferred annuities give you the option of annuitizing, but you do not have to annuitize. Indeed, many people never do. They simply use the deferred annuities as a safe way to earn a significant interest crediting rate and grow retirement savings over the long term.

Note that with both income and deferred annuities you can usually choose to add a joint life option or death benefits.

With a joint life payout option, you add a spouse or other beneficiary as an additional annuitant. Your payments will be lower, but they will continue as long as either you or that named beneficiary are still alive.

Death benefits help guarantee that named beneficiaries receive any remaining annuity account balance should you die before your premiums are paid back to you. That way, you can ensure that you don’t lose your premium — it gets passed on to your family or friends.

Depending on your annuity company, these add-on options may cost you extra or reduce the value of your annuity income payments.

When Do You Get Benefits from an Income Annuity?

Once you buy an income annuity, it annuitizes right away. Your stream of cash may begin as soon as one month after you pay your premium.

You also have the option to delay your annuity payments until a later date. With this option, you still must annuitize the annuity immediately, but your life insurance company will not process your payments until the date you specify.

You also typically get to select your payout schedule when you sign your contract, choosing between monthly, quarterly, semi-annual, and annual payments. These options allow you to customize your payouts so that they are most convenient for your lifestyle.

What are the Pros and Cons of an Income Annuity?

Income annuities — like all financial products — have advantages and disadvantages. Whether they’re right for you depends on your circumstances and needs.

Pros

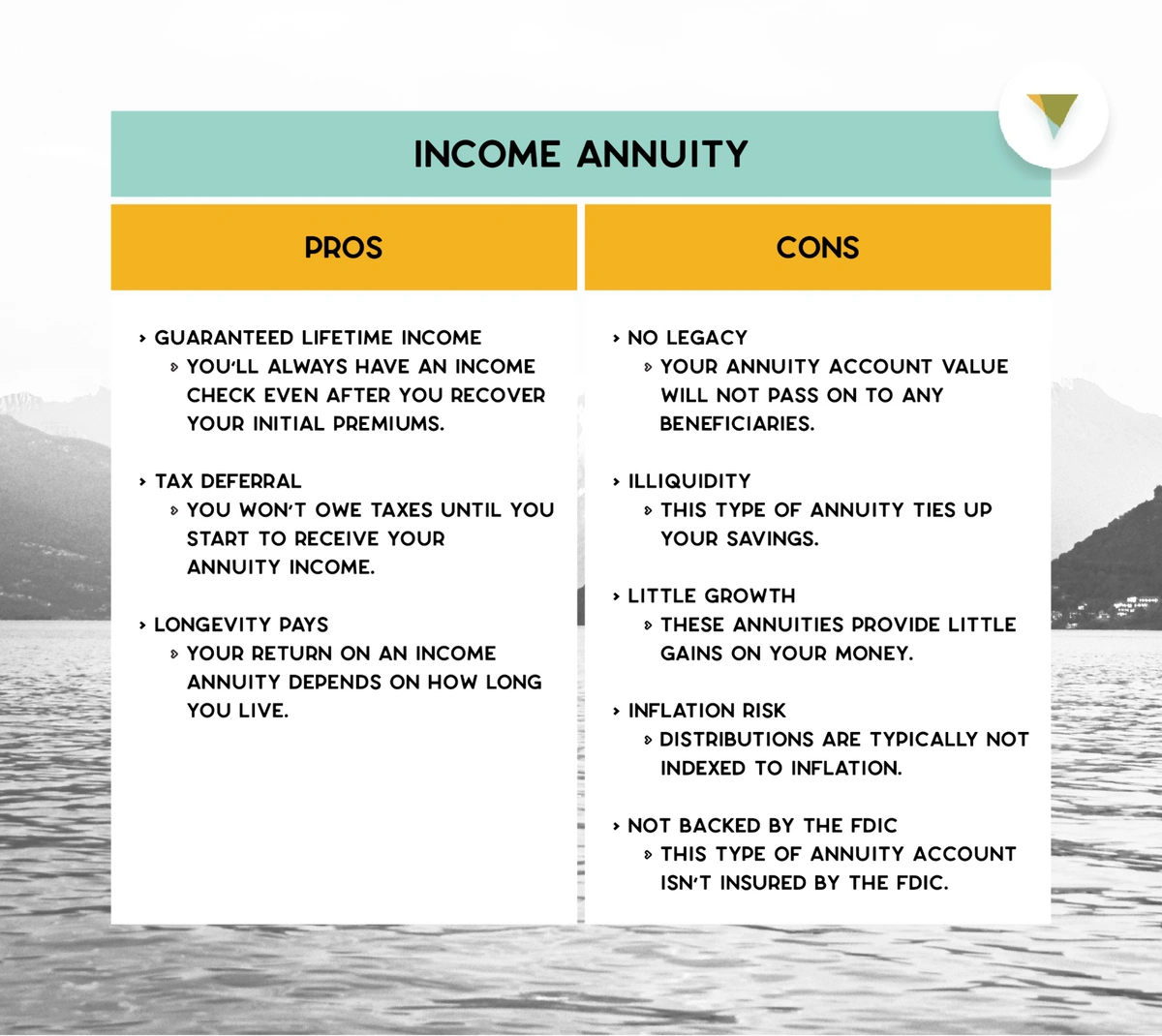

Some of the benefits of buying an income annuity include the following.

- Guaranteed lifetime income. The biggest benefit is the certainty that you won’t outlive your retirement savings. Annuities provide peace of mind because you can be confident that you’ll always have an income check even after you recover your initial premiums.

- Tax deferral. You won’t owe taxes until you start to receive your annuity income. Note that when you do start to receive your payments, they will be taxed as ordinary income.

- Longevity pays. Your return on an income annuity depends on how long you live. If you are healthy and live a very long time, you get more payments and a better return.

Cons

While income annuities can be advantageous, they also have some drawbacks. Some of the cons of income annuity contracts include the following.

- No legacy. In the most basic version of the income annuity contract, your annuity account value will not pass on to any beneficiaries. The money in your annuity account would go to the life insurance company. However, note that some annuity companies may offer death benefits as an optional add-on, which would ensure your beneficiaries receive back at least your initial premiums less any distributions.

- Illiquidity. Income annuities tie up your savings. Once you’ve paid your premiums, it can be costly to take the money back. Early withdrawals may come at the expense of surrender charges and tax penalties.

- Little growth. Another downside is that income annuities provide little gains on your money. Your cash will not earn any significant rate of return while it’s waiting in your annuity account to be paid back to you.

- Inflation risk. Distributions from income annuities are typically not indexed to inflation. That means that, during periods of inflation, the purchasing power of the annuity payments would decrease over time. If you’re worried about inflation, consider inflation-protected annuities.

- Not backed by the FDIC. Your income from an annuity is guaranteed only as long as the issuing insurance company is in business. If the financial strength of that company fails, your annuity account isn’t insured by the FDIC the same way a savings account would be.

Who is an Income Annuity Right For?

Income annuities are built for individuals in a certain set of circumstances. Here’s who they are best suited for.

Savers. Income annuities protect you from outliving your retirement savings. They’re ideal for individuals who have accumulated a significant retirement nest egg already and can use some of it to pay the annuity premiums. They may not be as appropriate for individuals who are still building up their retirement accounts.

Those who need income. Income annuities are ideal for individuals who have a concern that their retirement savings will not last the rest of their life. This type of annuity probably isn’t as useful for very wealthy individuals who are unlikely to outlive their savings, or for individuals with significant other sources of retirement income, like social security and pension income.

Older individuals. Because income annuities pay you back soon after you buy them, they’re best for individuals who are closer to retirement or already in it. They aren’t ideal for people further away from retirement or for young adult annuity buyers.

Safety seekers. Income annuities provide a guaranteed source of income, and that appeals to people who are less risk averse. Those who want potentially higher earnings — or who are comfortable with more risk — may be better off considering alternative investment options like mutual funds or stocks.

If you’re not sure, consider consulting a credible financial advisor for guidance on developing a retirement plan.

Are There Better Options?

There are many other annuity options that may be better suited to your circumstances and needs.

One alternative to an income annuity is a deferred annuity. Deferred annuities provide much more flexibility. For one thing, you can choose between funding your annuity with a single premium or with a flexible premium schedule, where you pay in a number of smaller payments over time.

Then, you can choose whether to annuitize when you’re ready, or not annuitize at all. Instead, at the end of the term, you can simply opt to receive your annuity account value back to you. This gives you more flexibility.

If you do choose to annuitize, most deferred annuities also offer a number of payout options that you can choose between. For example, you can choose the life annuity payout schedule, where you’re paid out for the rest of your life. Or, you can choose a period-certain payout option, where your monthly income payouts are higher, but only last for a specified period of time.

While your deferred annuity is accumulating, you also earn interest. Depending on the type of deferred annuity that you choose, you can earn more or less interest.

For example, you could choose a fixed annuity, which is the safest option. With a fixed you earn a fixed minimum interest rate, so you can be sure that your money will grow. Other options for deferred annuities include fixed-indexed annuities and variable annuities. These both introduce some stock market risk into the annuity, which increases your potential gains, but also increases your risk.

All of these options with deferred annuities make them potentially better suited to your needs and circumstances than income annuities.

Annuities Can Power-Up Your Retirement Plan

Income annuities are one of many annuity products that are designed to help you feel less stress around retirement. Their particular features — including immediate annuitization and lifetime payout — make them ideal for someone with a big chunk of cash that wants to generate income right away.

Anyone who’s not close to retirement, who doesn’t have a significant stash of retirement cash, or who wants their money to grow more before they turn it into income may be better off considering other options.

A fixed deferred annuity is more flexible because it allows you the opportunity to annuitize when you want, without requiring you to annuitize. It also offers better growth potential than income annuities because your money has time to earn interest.

Canvas Annuity offers extremely safe fixed annuity products that earn a guaranteed minimum interest crediting rate. These products are designed to help you save now so you can convert your cash to a lifetime income later.

Check out Canvas’ annuity products and have a look. If you think they’re right for you, apply today.

Resource Hub